ACCT 23020 Lecture Notes - Lecture 10: Deferral, Regional Policy Of The European Union, Accounts Receivable

6 Jul 2019

School

Department

Course

Professor

Document Summary

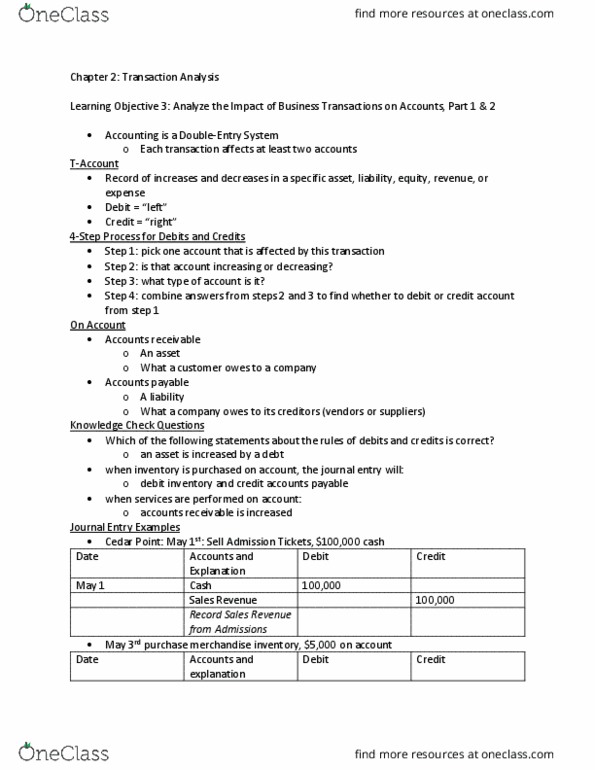

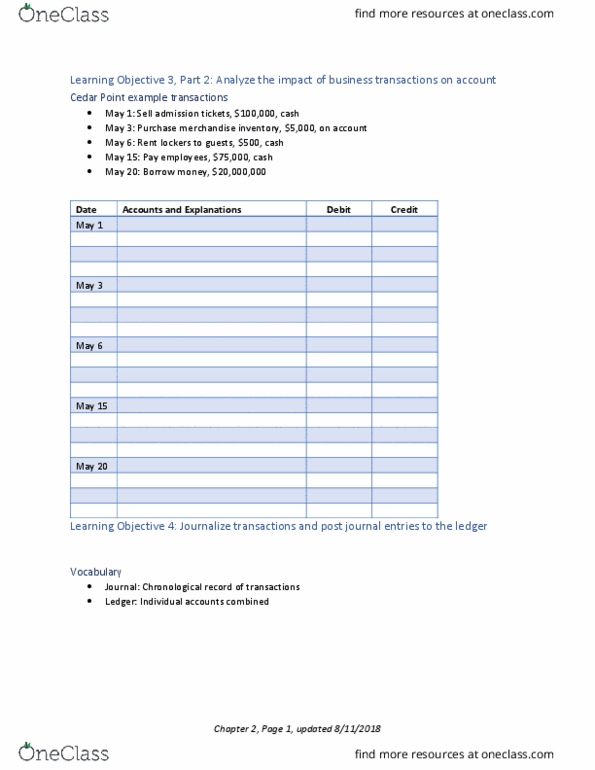

Learning objective 1: recognize a business transaction and the various types of accounts in which it can be recorded. Transaction: any event that has a financial impact on the business, can be measured reliably, provides information about an exchange, something given, something received, accounting records both sides of a transaction. Cedar point example transactions: sell admission to park, collect money for parking, purchase merchandise inventory for gift shops, rent lockers to guests, pay employees, borrow money (i. e. , to finance new roller coaster construction) Transactions: two sides, giving, receiving, record both sides. Account: record of all changes in a particular asset, liability, or stockholders" equity during a period, basic summary device. Inventory: products for sale to customers. (also known as merchandise and merchandise inventory: prepaid expenses: an asset that provides a future benefit for the business. Prepaid rent, prepaid insurance, and supplies are prepaid expenses.