ENG ELC 220 Lecture Notes - Lecture 27: Fixed Cost, Management Accounting, Financial Statement

Document Summary

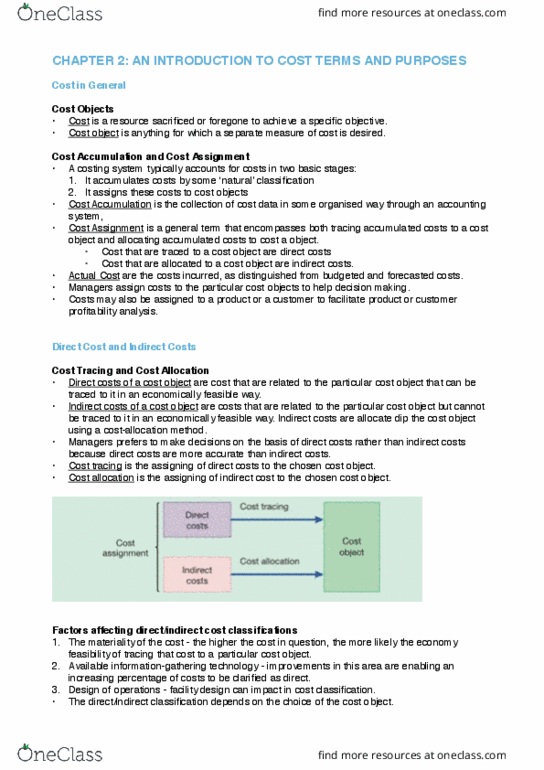

Chapter 2: an introduction to cost terms and purposes. Cost: a resource sacrificed or forgone to achieve a specific objective. Cost object: is anything for which a separate measurement of costs is desired. Examples of cost objects: product, service, project, customer, brand category, activity, department, programme. A costing system typically accounts for costs in two basic stages: it accumulates costs by some natural" classification such as materials, labour, fuel, advertising or shipping, it assigns these costs to cost objects. Cost accumulation: the collection of cost data in some organised way through an accounting system. Cost assignment: tracing accumulated costs to a cost object: allocating accumulated costs to a cost object. Indirect costs: costs that are traced to a cost object are direct costs, and costs that are allocated to a cost object. Actual costs: which are the costs incurred (historical costs), as distinguished from budgeted or forecasted costs.