ACCT 201 Lecture Notes - Lecture 11: Income Statement, Balance Sheet

ACCT 201 – Lecture 11 – Chapter 7

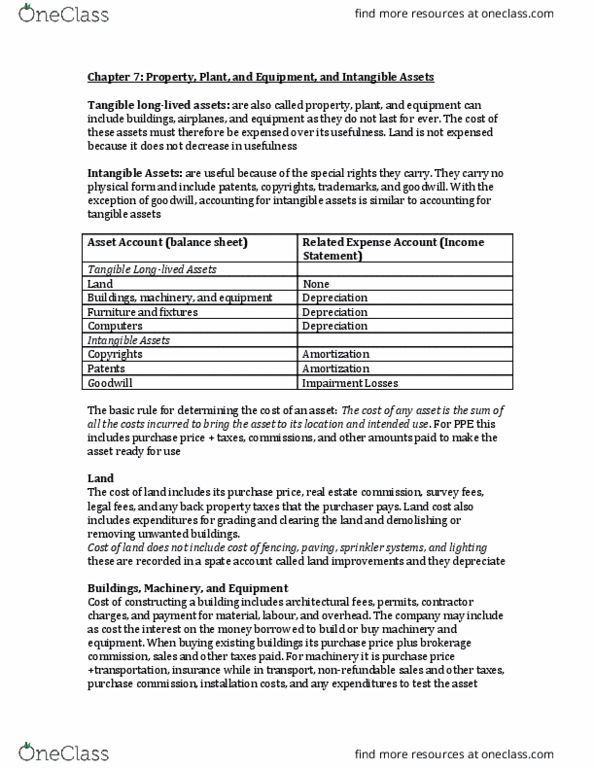

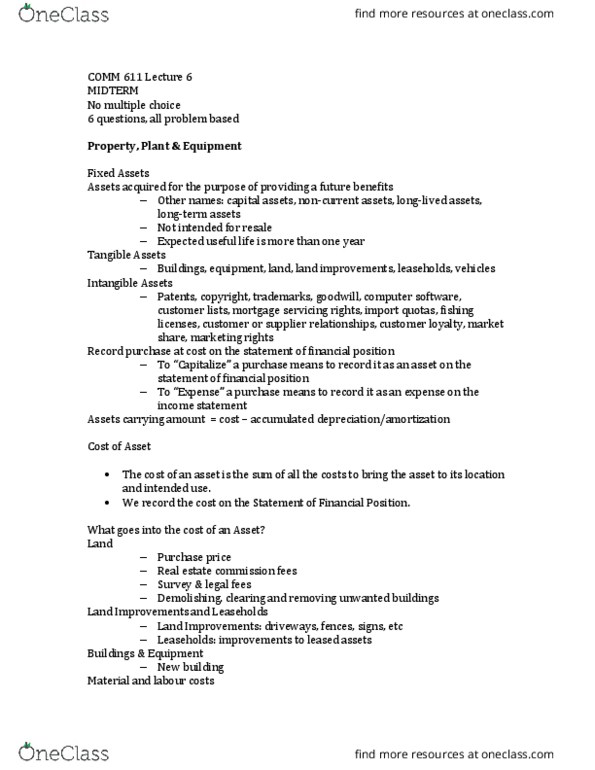

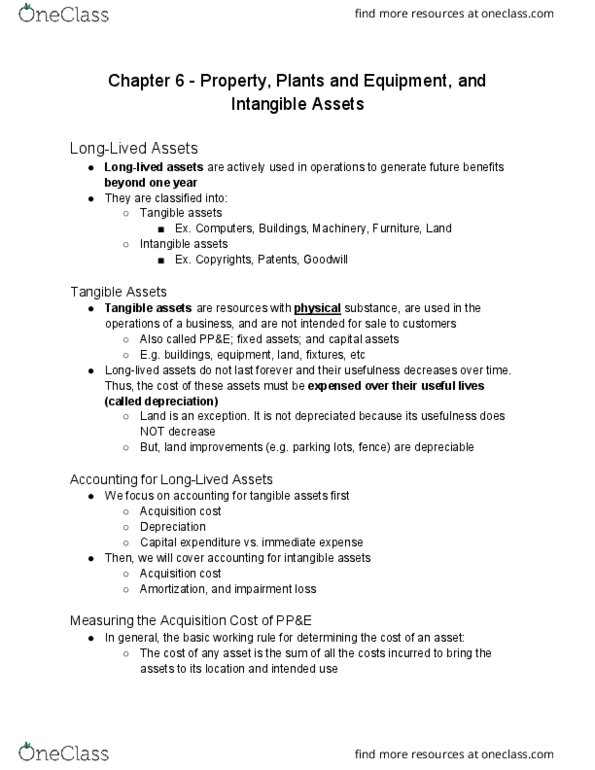

Chapter 7 – Long Term Assets

• Cost Allocation

o The building in this can be interchangeable with any Long Term Asset, except for

Land which does not get used up. LAND DOES NOT DEPRECIATE

• Acquisitions

o Types

▪ Tangible

• Includes Buildings, land, furniture, any physical thing

• Also includes Land improvements (fenses, parking lots, etc) –

these DO depreciate

• Also, Natural Resources (Mines, timerland, etc) – These do what is

called “amortize” which basically is just another term for

depreciation

▪ Intangible

• Includes Copyrights, Patents, etc. – These also are “amoritized”

• Also includes what is called “Good Will”, which is the difference

between amount paid and fair value

• Example:

Building

Asset

Building

Expense

Depreciation Expense

Question/Graph Taken From

“Financial Accounting”, Fourth

Edition, J. David Spiceland, Wayne

Thomas, Don Herrmann. (Page 363)

o In order to find goodwill must find the amount paid and

fair value

▪ Amount paid = 12,000,000

▪ Total Fair value = 10,500,000

▪ Goodwill = 12,000,000 – 10,500,000 = 1,500,000

o Costs

▪ All amounts necessary to obtain and get READY for its intended use

• Example: We paint the name of the company on the company

truck

• Costs After Acquisition

o Debit to Asset (Capitalization) = “Faster, Stronger, Bigger, Better”

o Debit to Expense = None of the above improvements

• Usage

o Accounts

▪ Depreciation Expense: How much is used up this period – goes on income

statement

▪ Accumulated Depreciation: Total used up – Goes on Balance sheet

▪ ***Depreciation: Allocation of cost, not a reflection of market value

o Methods

▪ Know

• Depreciable Cost = Cost – Residual Value (Salvage Value – what its

worth at the end of its life)

• Estimated Life – Don’t have to figure this out, it will be given

Truck

Cash

100

100

Depreciation Expense

Accumulated Depreciation

X

X

Document Summary

Acct 201 lecture 11 chapter 7. Chapter 7 long term assets: cost allocation. Depreciation expense: the building in this can be interchangeable with any long term asset, except for. Land does not depreciate: acquisitions, types, tangible. These also are (cid:862)a(cid:373)oritized(cid:863: also i(cid:374)(cid:272)ludes (cid:449)hat is (cid:272)alled (cid:862)good will(cid:863), (cid:449)hi(cid:272)h is the difference between amount paid and fair value, example: 100: costs after acquisition, de(cid:271)it to asset (cid:894)capitalizatio(cid:374)(cid:895) = (cid:862)faster, tro(cid:374)ger, bigger, better(cid:863, debit to expense = none of the above improvements, usage, accounts. Estimated life in years: example: solve the question using straight line method. Thomas, don herrmann. (page 363: cost = 270,000; rv = 24,000; time = 6 years (hours used later) This rate will be used consistently for all of the rates in declining balance method: example, using the same table as the last example, cost = 270,000; rv = 24,000; time = 6 years. Rv since we know it will be worth that much in the end.