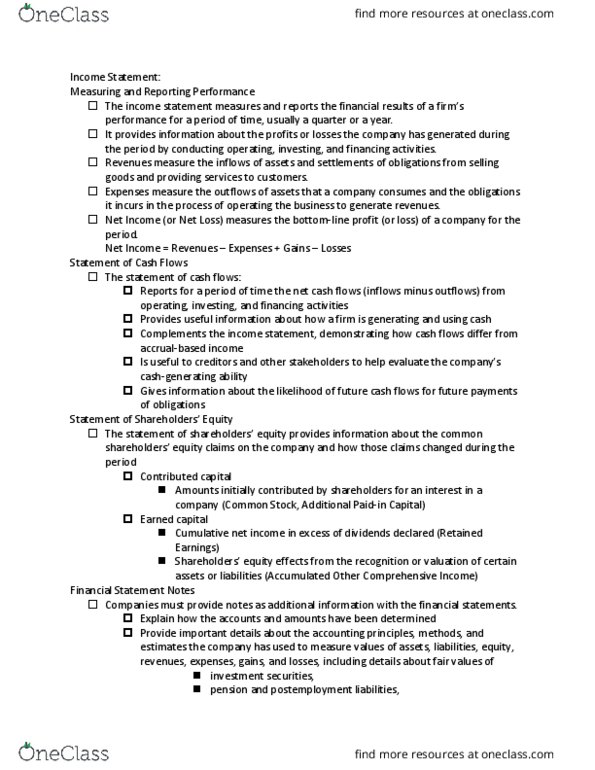

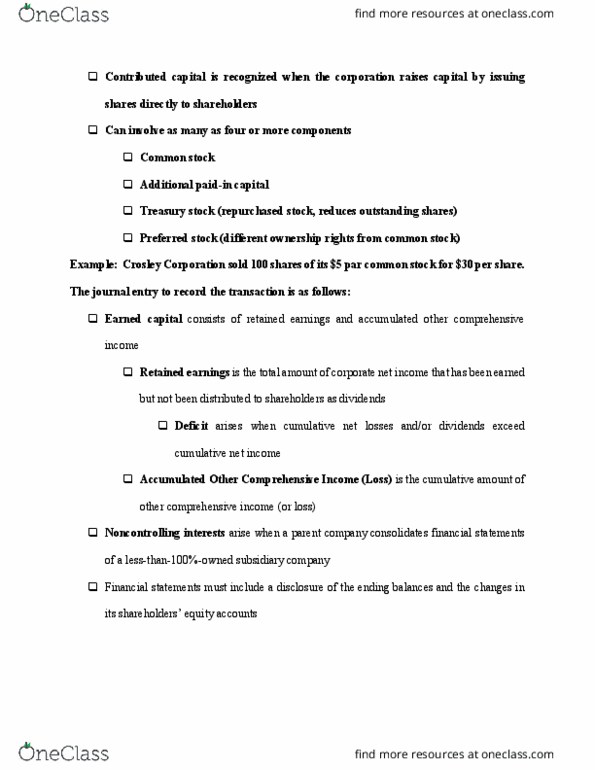

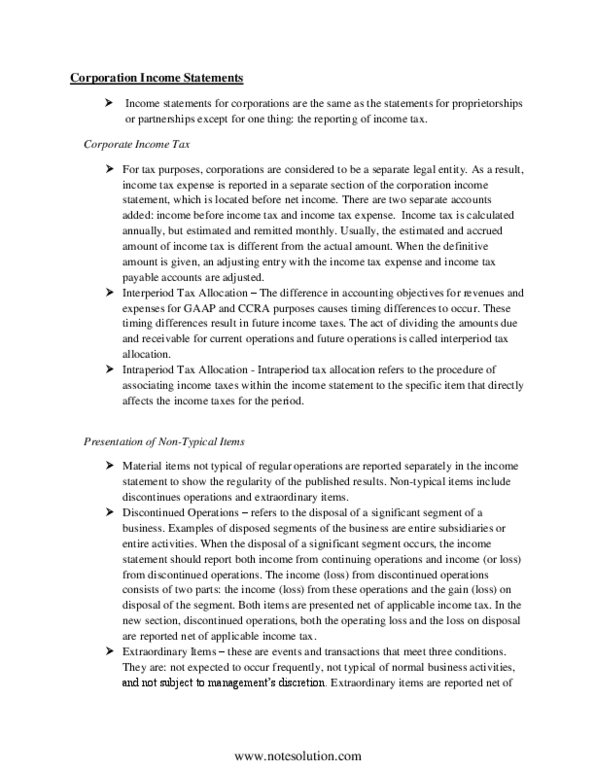

ACC 305 Lecture Notes - Lecture 41: Accrual, Retained Earnings, Income Statement

Get access

Related Documents

Related Questions

Following are selected accounts for Mergaronite Company andHill, Inc., as of December 31, 2018. Several of Mergaroniteâsaccounts have been omitted. Credit balances are indicated byparentheses. Dividends were declared and paid in the sameperiod.

| Mergaronite | Hill | ||||||||

| Revenues | $ | (602,000 | ) | $ | (240,000 | ) | |||

| Cost of goods sold | 260,000 | 114,000 | |||||||

| Depreciation expense | 120,000 | 44,000 | |||||||

| Investment income | NA | NA | |||||||

| Retained earnings, 1/1/18 | (892,000 | ) | (602,000 | ) | |||||

| Dividends declared | 120,000 | 44,000 | |||||||

| Current assets | 200,000 | 662,000 | |||||||

| Land | 318,000 | 94,000 | |||||||

| Buildings (net) | 500,000 | 140,000 | |||||||

| Equipment (net) | 194,000 | 248,000 | |||||||

| Liabilities | (390,000 | ) | (320,000 | ) | |||||

| Common stock | (294,000 | ) | (36,000 | ) | |||||

| Additional paid-in capital | (54,000 | ) | (908,000 | ) | |||||

Assume that Mergaronite took over Hill on January 1, 2014, byissuing 7,600 shares of common stock having a par value of $10 pershare but a fair value of $100 each. On January 1, 2014, Hillâsland was undervalued by $19,800, its buildings were overvalued by$29,200, and equipment was undervalued by $61,800. The buildingshad a 10-year remaining life; the equipment had a 5-year remaininglife. A customer list with an appraised value of $94,000 wasdeveloped internally by Hill and was to be written off over a20-year period.

A.) Determine the December 31, 2018, consolidatedtotals for the following accounts:

|

B.) In requirement (a), can the consolidated totalsbe determined without knowing which method the parent used toaccount for the subsidiary?

|

C.) If the parent uses the equity method, whatconsolidation entries would be used on a 2018worksheet?

Prepare Entry S to eliminate the beginning stockholders' equityof the subsidiary.

|

Prepare Entry A to recognize the unamortized allocation balancesas of the beginning of the current year.

|

Prepare Entry I to remove the equity income recognized duringthe year - equity method.

Prepare Entry D to remove the Intra-entity dividenddeclarations.

Prepare Entry E to recognize the excess acquisition-datefair-value amortizations for the period.

|