ECON 10010 Lecture Notes - Lecture 11: Average Cost, Marginal Product, Marginal Cost

Document Summary

Get access

Related Documents

Related Questions

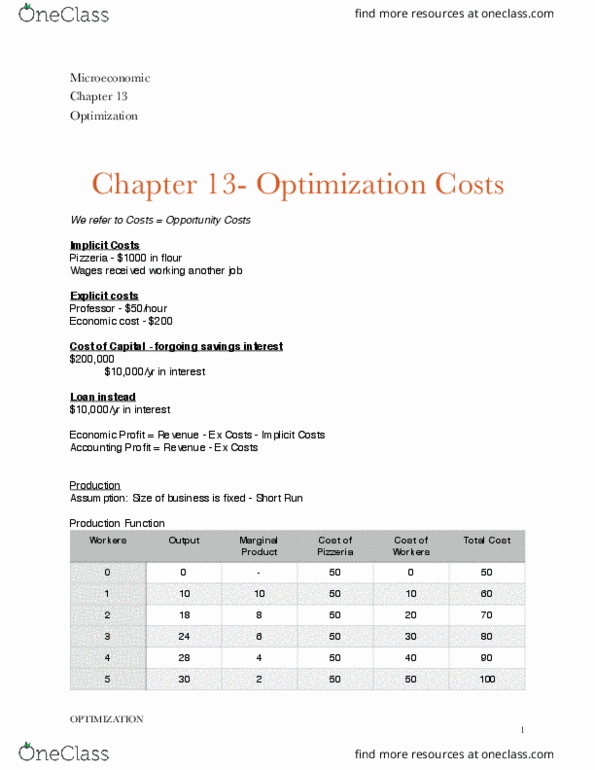

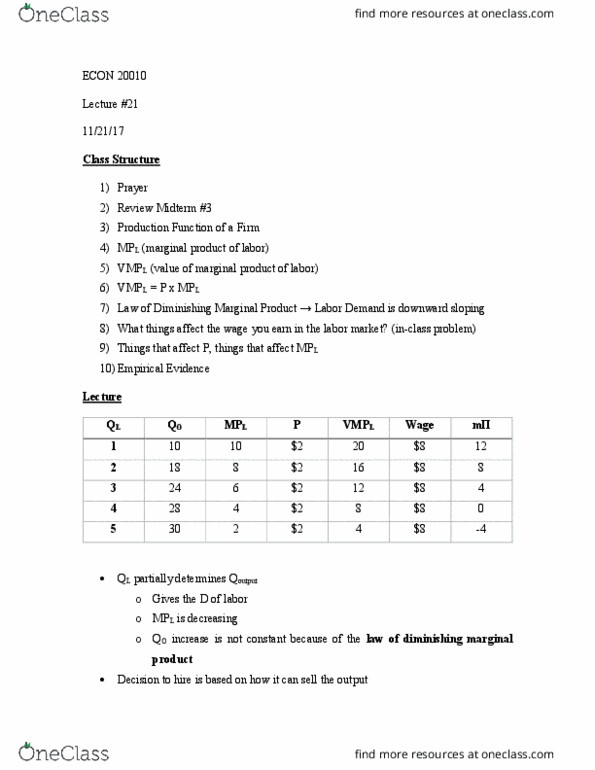

Redstone Clayworks Inc. is located in Sedona, Arizona, and manufactures clay fire pits for patios. They are one of about two dozen firms around the world that manufacture and sell clay fire pits for retailers such as Home Depot, Lowe's, Front Gate, and other upscale home product chains. There is virtually no product differentiation. A clay fire pit is a clay fire pit.

The spreadsheet below gives some of Redstone's production cost data.

Assume that the world market demand and supply curves for clay fire pots intersect at $190 per unit.

|

Q |

TC |

TFC |

TVC |

AFC |

AVC |

ATC |

SMC |

TR |

MR |

Profit |

Average |

Profit |

|

Profit |

Margin |

|||||||||||

|

0 |

7000 |

7000 |

NIL |

NIL |

NIL |

NIL |

NIL |

0 |

NIL |

-7000 |

NIL |

nil |

|

100 |

14000 |

7000 |

7000 |

70 |

70 |

140 |

70 |

19000 |

190 |

5000 |

50 |

26% |

|

200 |

23000 |

7000 |

16000 |

35 |

80 |

115 |

90 |

38000 |

190 |

15000 |

75 |

39% |

|

300 |

32000 |

7000 |

25000 |

23.33 |

83.33 |

106.67 |

90 |

57000 |

190 |

25000 |

83.33 |

44% |

|

400 |

43000 |

7000 |

36000 |

17.5 |

90 |

107.5 |

110 |

76000 |

190 |

33000 |

82.5 |

43% |

|

500 |

52000 |

7000 |

45000 |

14 |

90 |

104 |

90 |

95000 |

190 |

43000 |

86 |

45% |

|

600 |

74000 |

7000 |

67000 |

11.67 |

111.67 |

123.33 |

220 |

114000 |

190 |

40000 |

66.67 |

35% |

|

700 |

97000 |

7000 |

90000 |

10 |

128.57 |

138.57 |

230 |

133000 |

190 |

36000 |

51.43 |

27% |

|

800 |

111000 |

7000 |

104000 |

8.75 |

130 |

138.75 |

140 |

152000 |

190 |

41000 |

51.25 |

27% |

|

900 |

132000 |

7000 |

125000 |

7.78 |

138.89 |

146.67 |

210 |

171000 |

190 |

39000 |

43.33 |

23% |

|

1000 |

152000 |

7000 |

145000 |

7 |

145 |

152 |

200 |

190000 |

190 |

38000 |

38 |

20% |

AFC = total fixed cost/total output.

AVC = total variable cost/total output.

ATC = total cost/total output.

MC = change in total cost/change in output.

Total revenue = price * quantity. And given that the demand and supply intersect at $190, which implies that the equilibrium price is $190 because the point where the demand equals the supply determines the price.

MR = change in total revenue/change in output.

Profit = total revenue - total cost.

Average profit = total profit/total output.

Profit margin = total profit/total revenue*100 or (revenue - cost)/revenue*100.

Question:

What level of output should the manager of Redstone choose to produce? Explain your choice in 50-100 words.

Redstone Clayworks Inc. is located in Sedona, Arizona, and manufactures clay fire pits for patios. They are one of about two dozen firms around the world that manufacture and sell clay fire pits for retailers such as Home Depot, Lowe's, Front Gate, and other upscale home product chains. There is virtually no product differentiation. A clay fire pit is a clay fire pit.

The spreadsheet below gives some of Redstone's production cost data.

Assume that the world market demand and supply curves for clay fire pots intersect at $190 per unit.

|

Q |

TC |

TFC |

TVC |

AFC |

AVC |

ATC |

SMC |

TR |

MR |

Profit |

Average |

Profit |

|

|

|

|

|

|

|

|

|

|

|

|

Profit |

Margin |

|

0 |

7000 |

7000 |

NIL |

NIL |

NIL |

NIL |

NIL |

0 |

NIL |

-7000 |

NIL |

nil |

|

100 |

14000 |

7000 |

7000 |

70 |

70 |

140 |

70 |

19000 |

190 |

5000 |

50 |

26% |

|

200 |

23000 |

7000 |

16000 |

35 |

80 |

115 |

90 |

38000 |

190 |

15000 |

75 |

39% |

|

300 |

32000 |

7000 |

25000 |

23.33 |

83.33 |

106.67 |

90 |

57000 |

190 |

25000 |

83.33 |

44% |

|

400 |

43000 |

7000 |

36000 |

17.5 |

90 |

107.5 |

110 |

76000 |

190 |

33000 |

82.5 |

43% |

|

500 |

52000 |

7000 |

45000 |

14 |

90 |

104 |

90 |

95000 |

190 |

43000 |

86 |

45% |

|

600 |

74000 |

7000 |

67000 |

11.67 |

111.67 |

123.33 |

220 |

114000 |

190 |

40000 |

66.67 |

35% |

|

700 |

97000 |

7000 |

90000 |

10 |

128.57 |

138.57 |

230 |

133000 |

190 |

36000 |

51.43 |

27% |

|

800 |

111000 |

7000 |

104000 |

8.75 |

130 |

138.75 |

140 |

152000 |

190 |

41000 |

51.25 |

27% |

|

900 |

132000 |

7000 |

125000 |

7.78 |

138.89 |

146.67 |

210 |

171000 |

190 |

39000 |

43.33 |

23% |

|

1000 |

152000 |

7000 |

145000 |

7 |

145 |

152 |

200 |

190000 |

190 |

38000 |

38 |

20% |

AFC = total fixed cost/total output.

AVC = total variable cost/total output.

ATC = total cost/total output.

MC = change in total cost/change in output.

Total revenue = price * quantity. And given that the demand and supply intersect at $190, which implies that the equilibrium price is $190 because the point where the demand equals the supply determines the price.

MR = change in total revenue/change in output.

Profit = total revenue - total cost.

Average profit = total profit/total output.

Profit margin = total profit/total revenue*100 or (revenue - cost)/revenue*100.

Question:

a. What level of output should the manager of Redstone choose to produce? Explain your choice in 50-100 words.

b. Make a copy of your spreadsheet and triple the fixed costs to 21,000. How does this change your answer to question a? Explain your result in 50-100 words.