ACCT 1201 Lecture Notes - Electronic Funds Transfer, Skechers, Bank Reconciliation

22 Mar 2013

School

Department

Course

Professor

Document Summary

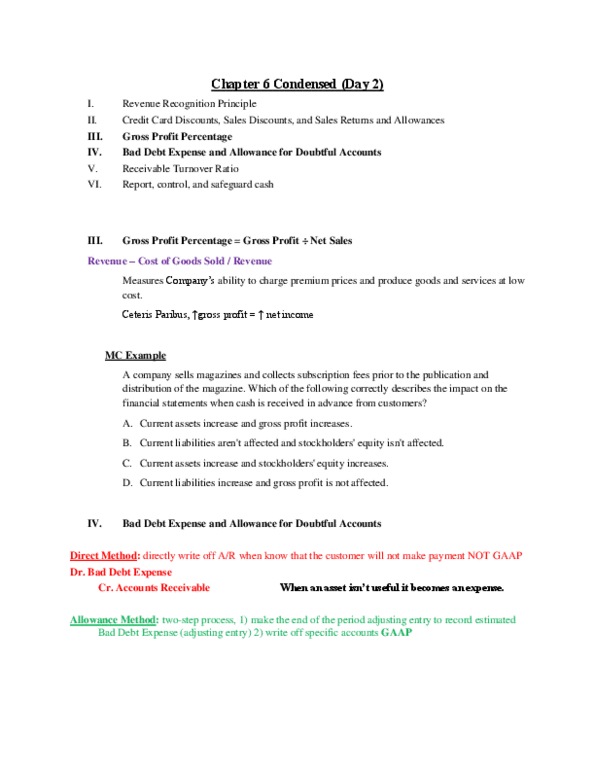

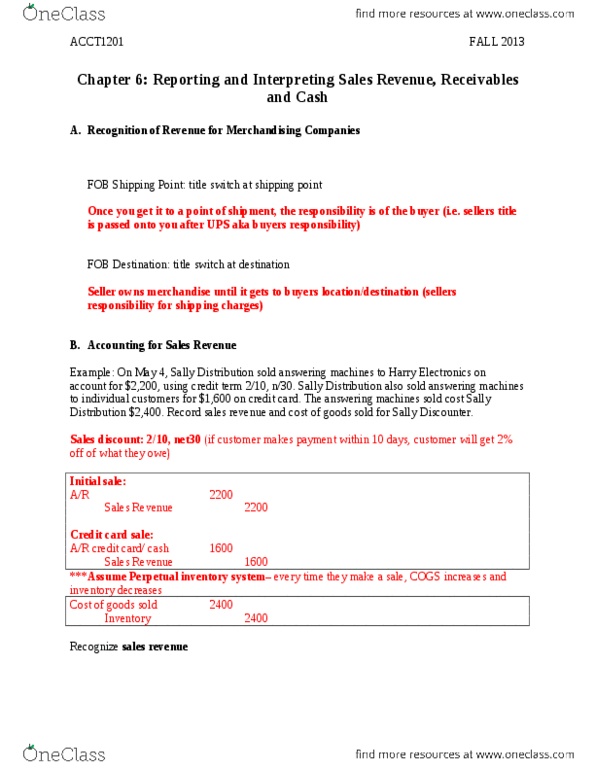

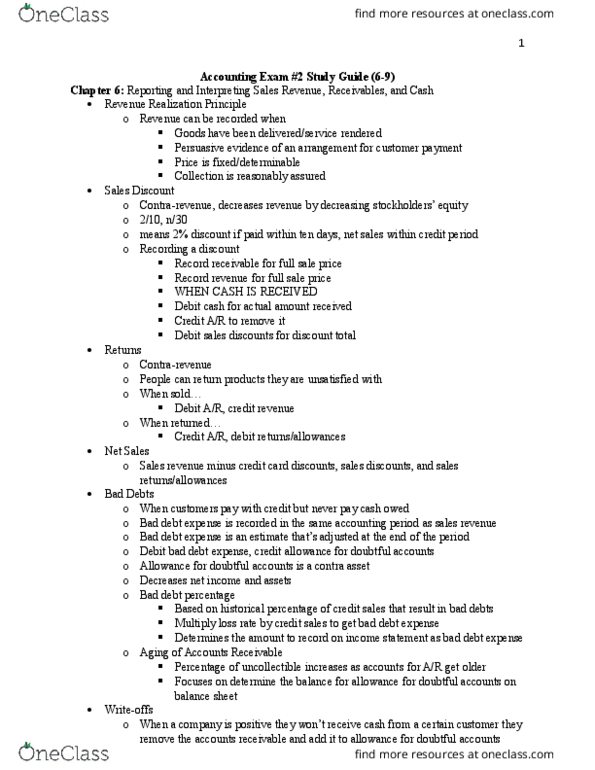

Credit card discounts, sales discounts, and sales returns and allowances. Bad debt expense and allowance for doubtful accounts. Receivables turnover ratio = net sales* average net trade accounts receivable. * ideally the numerator would be net credit sales, but companies often do not separate between cash and credit sales. Credit sales * percentage is bad calculation; general sales * percentage is even worse. Most of the time, the ratio will be greater than one. Average net trade accounts receivable ((beginning a/r + ending a/r) / 2) The receivables turnover ratio reflects how many times average trade receivables are recorded and collected during the period. The higher the ratio, the faster the collection of receivables. Average collection period = 365 receivables turnover ratio. Indicates the average time it takes a customer to pay its accounts. Example from textbook: deckers reported 2008 net sales of ,445,000. December 31, 2007, receivables were ,209,000 and december 31, 2008, receivables were ,129,000.