ACCT 1209 Lecture Notes - Lecture 27: Amortization Schedule, Interest Expense, Income Statement

1 Apr 2016

School

Department

Course

Professor

Document Summary

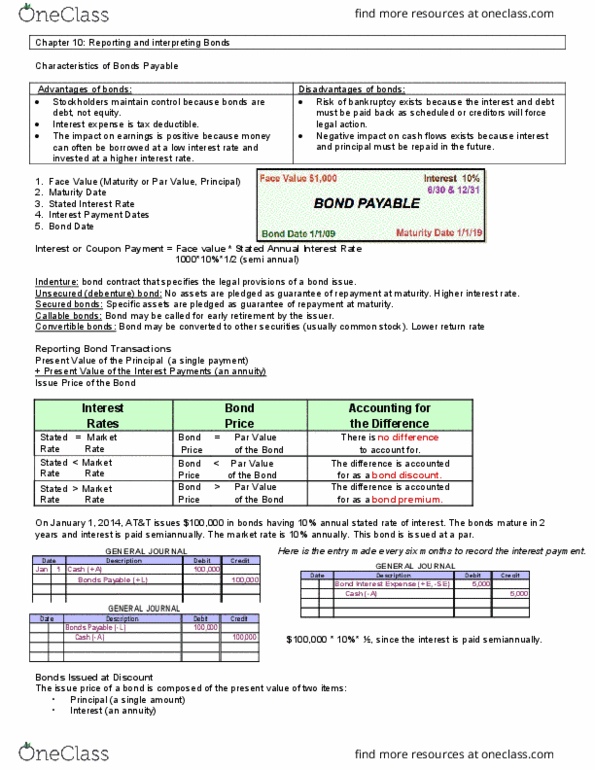

Acct 1209 lecture 27 - bonds issued at a premium, straight line vs. Part a: reporting interest expense on bonds issued at a premium using straight- The recorded premium of ,630 must be apportioned to each interest period. Using the straight-line method, the amortization of premium each annual interest period is (,630 4 periods). This amount is subtracted from the cash interest payment (,000) to calculate interest expense (,092). Thus, amortization of a bond premium decreases interest expense. The payment of interest on the bonds is recorded as follows: The ,000 cash paid each period includes ,092 interest expense and premium amortization. Thus, the cash payment to investors includes the current interest they have earned plus a return of part of the premium they paid when they bought the bonds. The book value of the bonds is the amount in the bonds payable account plus any unamortized premium.