ECON-UA 2 Lecture Notes - Lecture 8: Opportunity Cost, Monopolistic Competition, Marginal Revenue

12 Sep 2016

School

Department

Course

Professor

Document Summary

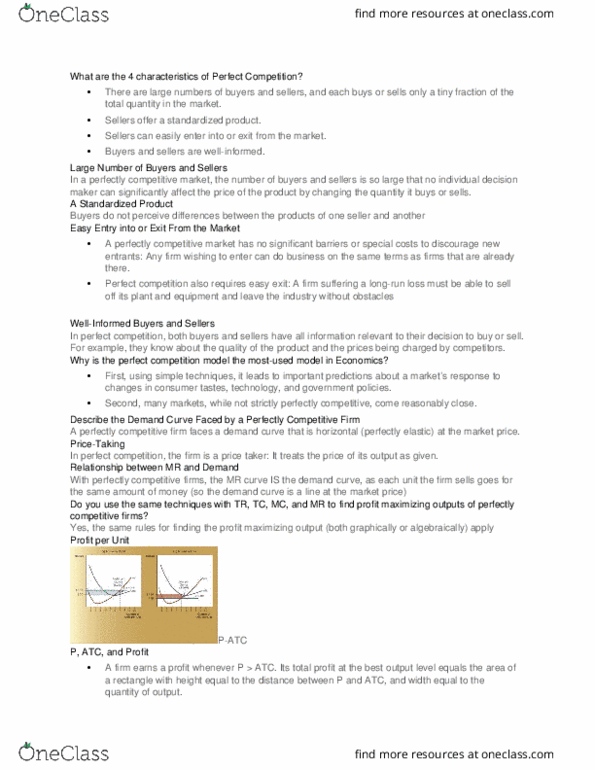

Average revenue = marginal revenue = price slope of total revenue is constant slope of marginal revenue is constant. ***pro t maximising rule: mr = mc (mc cuts mr from below) total loss = (di erence between mr and atc) x q* shut down price | the p at which a rm is indi erent between producing and shutting down. Rm shuts down when rm goes down below the average variable curve. Rm"s short-run supply curve shows the pro t maximising q supplied at each price ( rm takes as given) supply curve: if price is x, i will supply y (this is pro t maximising supply) + stability = economic pro t must be 0 (normal pro t) all inputs can be varied because rms can adjust capital new rms can enter and existing ones can exit deriving the market supply curve *entry and exit also determine the plant size in the long run.