ECON 0100 Lecture 2: Lecture 2

Chapter 3

Supply & Demand

Competitive Markets

There are many buyers and sellers of the same good or service

§

No one buyer or seller's actions are able to influence the market price

§

○

Supply & Demand Model

You can identify what factors determine and affect the price and quantity of goods

being traded in a competitive market

§

○

•

Demand

QUESTION

How many cups of coffee would people buy if the price were $5? $4? $1?

§

Price

Quantity

Demanded

$5

1

$4

7

$3

15

$2

20

$1

25

○

Demand Schedule

Shows amount consumers are willing to buy at every price

§

○

Quantity Demanded

Amount consumers want to buy at a specific price

§

○

Demand Curve

Graphical representation of a demand schedule

§

○

Demand

The amount consumers want to purchase at EACH different price

§

This is the ENTIRE demand curve

§

○

Quantity Demanded

Amount consumers want to purchase for a specific curve

§

Graphically, this is ONE POINT on the demand curve

§

○

As the price of coffee decreases, the quantity demanded ____________.

Called the Law of Demand

All else equal, there is an INVERSE relationship between price and quantity

demanded.

As the price of a good ____, the quantity demanded ____.

®

As the price of a good ____, the quantity demanded ____.

®

□

§

○

•

Changes in Demand

All else equal means we are holding all other factors such as consumer income, tastes and

preferences, and the price of related goods constant.

○

What happens when one of these factors changes?

○

What happens to the demand for coffee during finals.

○

Price

Quantity

Demanded

(OLD)

Quantity

Demanded

(NEW)

$5

1

3

$4

7

12

$3

15

20

$2

20

24

$1

25

25

○

•

Factors that Demand Shift Demand

FACTOR 1: Change in Price of Related Goods

Two types of related goods

Compliments

□

Substitutes

□

§

Two goods are Compliments if:

INCREASE in the price of one good --> DECREASES the demand of the other good

□

These are goods that are typically consumed together

□

Example

You buy a coffee and bagel every morning. Bagel price goes up. You don't

want to drink coffee without eating your bagel. So you buy neither.

®

□

§

Two goods are Substitutes if:

INCREASE in the price of one good --> INCREASES the demand for the other good

□

These are goods that typically serve similar functions or are interchangeable

□

Example

Price of Coke increases, the demand for Pepsi increases

®

Price of coffee increases, the demand for tea goes up.

®

□

§

○

FACTOR 2: Change in Consumer Income

Normal Goods

Goods that when consumer income increases, the demand for them INCREASES

□

Example

Cars

®

House

®

□

§

Inferior Goods

Goods that when consumer income increases, the demand for them DECREASES

□

Example

Bus fair

®

Off-brand goods

®

□

§

○

FACTOR 3: Change in Tastes & Preferences

Examples

What is in in fashion

□

Change in food

□

Change in seasons

□

§

○

FACTOR 4: Change in Future Expectations

Examples

Extreme weather conditions

□

Investing in stock in a company that is starting to be good

□

Buying before Black Friday

□

§

○

FACTOR 5: Change in Number of Consumers

When we draw a Market Demand Curve, it is actually composed of several Individual

Demand Curves

§

○

•

The Market Demand Curve shows the quantity demanded for a good by all consumers

in the market at every given price.

§

It is the horizontal sum of all the individual demand curves.

§

As we add MORE consumers, the quantity demanded at every given price INCREASES

& the demand INCREASES.

§

CAREFUL!

Change in Demand

Caused by a change in one of the 5 factors listed.

□

Graphically, it is represented by a shift in the ENTIRE demand curve.

□

INCREASE in demand = shift the curve to the RIGHT

□

DECREASE in demand = shift the curve to the LEFT

□

§

Change in Quantity Demanded

Caused when the good's OWN price changes.

□

Graphically, represented by movement ALONG the demand curve.

Going from one point to another

®

□

§

○

PRACTICE PROBLEMS

Consider the market for popcorn. Illustrate what would happen if the price of DVDs

increased.

○

•

Once again, consider the market for popcorn. Illustrate what would happen if the price of

popcorn increased.

○

Assume popcorn is a normal good. Illustrate what would happen if consumer income

increased.

○

Which of the following would cause a DECREASE in demand for cars?

A decrease in the price of gasoline

A.

An increase in the price of cars

B.

An increase in the popularity of road trips

C.

An improvement in public transportation.

D.

○

Supply

Economists are also interested in modelling the behavior of sellers.

Much of this will look similar to what you saw when we were looking at consumers and

demanded.

§

○

Consider the following:

○

Price

Quantity

Supplied

$5

10

$4

8

$3

6

$2

4

$1

2

If the price is more, you will want to sell more

§

○

Supply Schedule

Graph that shows the amount of a good or service that will be supplied by sellers at

every given price

§

○

Quantity Supplied

Amount supplied at a SPECIFIC price

§

○

Supply Curve

Supply schedule represented graphically

§

○

Law of Supply

All else equal, there is a positive relationship between price and quantity supplied.

§

As the price of a good ____, the quantity supply____.

§

As the price of a good ____, the quantity supply ____.

§

○

•

Factors that Shift Supply

FACTOR 1: An input is any good or service used in production.

As input prices for a good INCREASE, supply _________ because ___________.

§

As input prices for a good DECREASE, supply _____________.

§

Example

Illustrate what happens to the supply of t-shirts if the price of cotton increases.

□

§

○

•

FACTOR 2: Change in Price of Related Goods

Two goods are Substitutes in Production if:

INCREASE in price of one good --> DECREASE the supply of the other good

□

These are goods that typically use the same resources

□

Producing one good prevents sellers from using resources to produce another.

□

Example:

Price for sandwiches goes up, you eat more bagels instead

®

□

§

Two goods are Compliments in Production if:

INCREASE in price of one good --> INCREASE the supply of the other good

□

Occurs if one good uses the product of the other

□

Example:

The price of beef increases, the price of leather increases

®

□

§

○

FACTOR 3: Technology

Improvements in technology should shift to the ________.

§

More efficient way to produce a good means that more of the good is being made,

supply goes ___.

§

Example:

Illustrate what effect the introduction of the assembly line had on the supply of

cars.

□

§

○

FACTOR 4: Expectations

If producers expect the price of a good to DROP in the future, supply will ____ in the

short run.

§

If producers expect the price of a good to INCREASE in the future, supply will ____ in

the short run.

§

○

FACTOR 5: Change in the Number of Producers

Similar to demand, the market supply curve is made up of several individual supply

curves

§

○

The market supply curve shows the quantity supplied or a good by all producers in the

market at every given price.

§

It is the horizontal sum of all the individual supply curves.

§

As we add more producers, the quantity supplied at every given price ___, and the

supply ____. Graphically, it becomes ___________.

§

CAREFUL!

Change in Supply

Caused by a change in one of the five factors.

§

Graphically, this is represented by a shift in the ENTIRE supply curve.

§

○

Change in Quantity Supplied

Occurs when the good's own price changes.

§

Graphically, this is represented by movement ALONG the supply curve.

§

○

We model an INCREASE in supply by shifting the supply curve to the _______.

○

We model an DECREASE in supply by shifting the supply curve to the _______.

○

•

Market Equilibrium

Equilibrium means that no one individual has the ability to make themselves better off by

doing something else.

○

•

Markets Move Towards Equilibrium

What happens when market price is above the equilibrium price? Below equilibrium price?

○

•

Changes in Market Equilibrium

What happens to market equilibrium when the demand curve shifts?

○

•

The INCREASE in demand causes prices to __________ and quantity to ____________.

§

What happens to market equilibrium when the demand curve shifts?

○

What happens to market equilibrium if both curves shifted simultaneously?

When both curves shift simultaneously, we can only determine the effect on P or Q,

NEVER both.

§

USEFUL TRICK:

Determine what the effect of each shift is separately, then combine to determine

the total effect.

□

§

Example:

Increase in Supply & Increase in Demand

□

§

○

Chapter 4

Consumer Surplus

The table below shoes the WTP for a Kennywood tickets.

○

Potential

Buyer

Willingness

to Pay

CS if

P=$45

Alice

$100

Bob

$85

Caroline

$60

David

$45

Evan

$40

Individual Consumer Surplus

Gain a single buyer gets from purchase

§

○

Total Consumer Surplus

Sum of all of the individual consumer surpluses

§

○

We can use the information on willingness to pay to construct a demand schedule and

graphically illustrate consumer to surplus.

On a graph, consumer surplus is everything BELOW THE DEMAND CURVE & ABOVE

THE PRICE.

§

○

•

Area of a Triangle

(Base*Height)/2

§

○

Consumer Surplus After a Price Change

•

What would happen if the price would have increased?

○

Producer Surplus

Potential

Seller

Cost

PS if

P=$40

Frank

$10

Gregory

$25

Hanna

$35

Ingrid

$45

Jacqueline

$55

○

Individual Producer Surplus

Gain a single seller gets from selling something

§

○

Total Producer Surplus

Sum of all of the individual producer surpluses

§

○

We can use the information on seller cost to construct a supply schedule and graphically

illustrate producer surplus.

On a graph, producer surplus is everything ABOVE THE SUPPLY CURVE & BELOW

THE PRICE.

§

○

•

Producer Surplus After a Price Change

What would happen to producer surplus after a price decrease?

○

•

All Together - Total Surplus

Total Surplus

Producer Surplus + Consumer Surplus

§

Illustrates one of the key economic principles: INCENTIVES

§

○

Markets are usually efficient.

This is when, in equilibrium, the Total Surplus is at a max.

§

○

EXAMPLE

Identify and calculate consumer surplus, producer surplus, and total surplus in the

following market.

§

○

•

Chapter 5

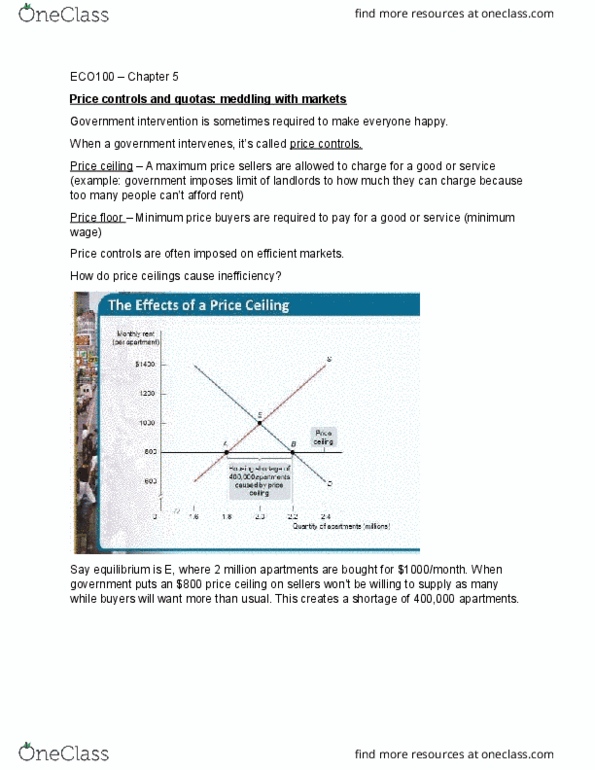

Price Controls

Policies that restrict how high or low a price can be

○

Price Ceiling

Dictates the MAX price sellers are allowed to charge for a good or service.

§

A common example is apartment rent laws in NYC.

§

○

Price Floor

Dictates the MIN price sellers are allowed to charge for a good or service.

§

A common example is minimum wage.

§

○

•

Modeling a Binding Price Ceiling

•

Deadweight Loss (DWL)

The loss in the total surplus whenever a policy or action distorts the quantity being

traded in a market away from the efficient Q.

§

○

Area of a Trapezoid

(Side1+ Side2)*Height / 2

§

○

Modeling a Binding Price Floor

•

What happens if a price floor is set above equilibrium price?

○

What happens if a price floor is set below equilibrium price?

○

Is the shift in demand or quantity

demanded? _________________

•

The two goods are ________________.

•

Is the shift in demand or quantity

demanded? _________________

•

Is the shift in demand or quantity

demanded? _________________

•

A market is in equilibrium when the

price in the market is such that

_________________ = ________________.

○

What would happen if a seller tried

to charge prices above what other

sellers were charging?

○

_________________________

What would happen if a buyer tried

to negotiate a price well below what

other buyers were paying?

○

_________________________

Consider the market for tennis shoes and

assume it is initially in equilibrium. An

increase in the popularity in running causes

the demand for tennis shoes to _____. As a

result, the _______ curve shifts to the______.

Initially, there is a ________ of tennis shoes.

This causes _____________________________.

○

Consider the market for chairs and

assume it is initially in equilibrium

○

Illustrate what would happen if the price

of wood INCREASED.

○

Total Effect:

Price ________

Quantity _____

Price ____, Quantity ___

Price ____, Quantity ____

Area ___ represents the original CS

before the price decrease.

○

Area ___ represents the increase in

CS to original buyers after the price

decreases.

○

Area ___ represents the increase in

CS gained by new buyers.

○

Area ___ represents the original PS

before the price increase.

○

Area ___ represents the increase in

PS to original sellers after the price

increase.

○

Area ___ represents the increase in

PS gained by new sellers entering.

○

Side effect of introducing a

binding price ceiling into an

efficient market:

Shortage

○

Inefficient Allocation

○

Wasted Resources (Time)

○

Low Quality

○

Black Markets

○

•

Side effect of introducing a binding

price floor into an efficient market:

Surplus

○

Inefficient Allocation of Products

○

Wasted Resources

○

Inefficiency of High Quality

○

Black Markets

○

•

Lecture 2

Sunday,*May*20,*2018

3:41*PM

Chapter 3

Supply & Demand

Competitive Markets

There are many buyers and sellers of the same good or service

§

No one buyer or seller's actions are able to influence the market price

§

○

Supply & Demand Model

You can identify what factors determine and affect the price and quantity of goods

being traded in a competitive market

§

○

•

Demand

QUESTION

How many cups of coffee would people buy if the price were $5? $4? $1?

§

Price

Quantity

Demanded

$5

1

$4

7

$3

15

$2

20

$1

25

○

Demand Schedule

Shows amount consumers are willing to buy at every price

§

○

Quantity Demanded

Amount consumers want to buy at a specific price

§

○

Demand Curve

Graphical representation of a demand schedule

§

○

Demand

The amount consumers want to purchase at EACH different price

§

This is the ENTIRE demand curve

§

○

Quantity Demanded

Amount consumers want to purchase for a specific curve

§

Graphically, this is ONE POINT on the demand curve

§

○

As the price of coffee decreases, the quantity demanded ____________.

Called the Law of Demand

All else equal, there is an INVERSE relationship between price and quantity

demanded.

As the price of a good ____, the quantity demanded ____.

®

As the price of a good ____, the quantity demanded ____.

®

□

§

○

•

Changes in Demand

All else equal means we are holding all other factors such as consumer income, tastes and

preferences, and the price of related goods constant.

○

What happens when one of these factors changes?

○

What happens to the demand for coffee during finals.

○

Price

Quantity

Demanded

(OLD)

Quantity

Demanded

(NEW)

$5

1

3

$4

7

12

$3

15

20

$2

20

24

$1

25

25

○

•

Factors that Demand Shift Demand

FACTOR 1: Change in Price of Related Goods

Two types of related goods

Compliments

□

Substitutes

□

§

Two goods are Compliments if:

INCREASE in the price of one good --> DECREASES the demand of the other good

□

These are goods that are typically consumed together

□

Example

You buy a coffee and bagel every morning. Bagel price goes up. You don't

want to drink coffee without eating your bagel. So you buy neither.

®

□

§

Two goods are Substitutes if:

INCREASE in the price of one good --> INCREASES the demand for the other good

□

These are goods that typically serve similar functions or are interchangeable

□

Example

Price of Coke increases, the demand for Pepsi increases

®

Price of coffee increases, the demand for tea goes up.

®

□

§

○

FACTOR 2: Change in Consumer Income

Normal Goods

Goods that when consumer income increases, the demand for them INCREASES

□

Example

Cars

®

House

®

□

§

Inferior Goods

Goods that when consumer income increases, the demand for them DECREASES

□

Example

Bus fair

®

Off-brand goods

®

□

§

○

FACTOR 3: Change in Tastes & Preferences

Examples

What is in in fashion

□

Change in food

□

Change in seasons

□

§

○

FACTOR 4: Change in Future Expectations

Examples

Extreme weather conditions

□

Investing in stock in a company that is starting to be good

□

Buying before Black Friday

□

§

○

FACTOR 5: Change in Number of Consumers

When we draw a Market Demand Curve, it is actually composed of several Individual

Demand Curves

§

○

•

The Market Demand Curve shows the quantity demanded for a good by all consumers

in the market at every given price.

§

It is the horizontal sum of all the individual demand curves.

§

As we add MORE consumers, the quantity demanded at every given price INCREASES

& the demand INCREASES.

§

CAREFUL!

Change in Demand

Caused by a change in one of the 5 factors listed.

□

Graphically, it is represented by a shift in the ENTIRE demand curve.

□

INCREASE in demand = shift the curve to the RIGHT

□

DECREASE in demand = shift the curve to the LEFT

□

§

Change in Quantity Demanded

Caused when the good's OWN price changes.

□

Graphically, represented by movement ALONG the demand curve.

Going from one point to another

®

□

§

○

PRACTICE PROBLEMS

Consider the market for popcorn. Illustrate what would happen if the price of DVDs

increased.

○

•

Once again, consider the market for popcorn. Illustrate what would happen if the price of

popcorn increased.

○

Assume popcorn is a normal good. Illustrate what would happen if consumer income

increased.

○

Which of the following would cause a DECREASE in demand for cars?

A decrease in the price of gasoline

A.

An increase in the price of cars

B.

An increase in the popularity of road trips

C.

An improvement in public transportation.

D.

○

Supply

Economists are also interested in modelling the behavior of sellers.

Much of this will look similar to what you saw when we were looking at consumers and

demanded.

§

○

Consider the following:

○

Price

Quantity

Supplied

$5

10

$4

8

$3

6

$2

4

$1

2

If the price is more, you will want to sell more

§

○

Supply Schedule

Graph that shows the amount of a good or service that will be supplied by sellers at

every given price

§

○

Quantity Supplied

Amount supplied at a SPECIFIC price

§

○

Supply Curve

Supply schedule represented graphically

§

○

Law of Supply

All else equal, there is a positive relationship between price and quantity supplied.

§

As the price of a good ____, the quantity supply____.

§

As the price of a good ____, the quantity supply ____.

§

○

•

Factors that Shift Supply

FACTOR 1: An input is any good or service used in production.

As input prices for a good INCREASE, supply _________ because ___________.

§

As input prices for a good DECREASE, supply _____________.

§

Example

Illustrate what happens to the supply of t-shirts if the price of cotton increases.

□

§

○

•

FACTOR 2: Change in Price of Related Goods

Two goods are Substitutes in Production if:

INCREASE in price of one good --> DECREASE the supply of the other good

□

These are goods that typically use the same resources

□

Producing one good prevents sellers from using resources to produce another.

□

Example:

Price for sandwiches goes up, you eat more bagels instead

®

□

§

Two goods are Compliments in Production if:

INCREASE in price of one good --> INCREASE the supply of the other good

□

Occurs if one good uses the product of the other

□

Example:

The price of beef increases, the price of leather increases

®

□

§

○

FACTOR 3: Technology

Improvements in technology should shift to the ________.

§

More efficient way to produce a good means that more of the good is being made,

supply goes ___.

§

Example:

Illustrate what effect the introduction of the assembly line had on the supply of

cars.

□

§

○

FACTOR 4: Expectations

If producers expect the price of a good to DROP in the future, supply will ____ in the

short run.

§

If producers expect the price of a good to INCREASE in the future, supply will ____ in

the short run.

§

○

FACTOR 5: Change in the Number of Producers

Similar to demand, the market supply curve is made up of several individual supply

curves

§

○

The market supply curve shows the quantity supplied or a good by all producers in the

market at every given price.

§

It is the horizontal sum of all the individual supply curves.

§

As we add more producers, the quantity supplied at every given price ___, and the

supply ____. Graphically, it becomes ___________.

§

CAREFUL!

Change in Supply

Caused by a change in one of the five factors.

§

Graphically, this is represented by a shift in the ENTIRE supply curve.

§

○

Change in Quantity Supplied

Occurs when the good's own price changes.

§

Graphically, this is represented by movement ALONG the supply curve.

§

○

We model an INCREASE in supply by shifting the supply curve to the _______.

○

We model an DECREASE in supply by shifting the supply curve to the _______.

○

•

Market Equilibrium

Equilibrium means that no one individual has the ability to make themselves better off by

doing something else.

○

•

Markets Move Towards Equilibrium

What happens when market price is above the equilibrium price? Below equilibrium price?

○

•

Changes in Market Equilibrium

What happens to market equilibrium when the demand curve shifts?

○

•

The INCREASE in demand causes prices to __________ and quantity to ____________.

§

What happens to market equilibrium when the demand curve shifts?

○

What happens to market equilibrium if both curves shifted simultaneously?

When both curves shift simultaneously, we can only determine the effect on P or Q,

NEVER both.

§

USEFUL TRICK:

Determine what the effect of each shift is separately, then combine to determine

the total effect.

□

§

Example:

Increase in Supply & Increase in Demand

□

§

○

Chapter 4

Consumer Surplus

The table below shoes the WTP for a Kennywood tickets.

○

Potential

Buyer

Willingness

to Pay

CS if

P=$45

Alice

$100

Bob

$85

Caroline

$60

David

$45

Evan

$40

Individual Consumer Surplus

Gain a single buyer gets from purchase

§

○

Total Consumer Surplus

Sum of all of the individual consumer surpluses

§

○

We can use the information on willingness to pay to construct a demand schedule and

graphically illustrate consumer to surplus.

On a graph, consumer surplus is everything BELOW THE DEMAND CURVE & ABOVE

THE PRICE.

§

○

•

Area of a Triangle

(Base*Height)/2

§

○

Consumer Surplus After a Price Change

•

What would happen if the price would have increased?

○

Producer Surplus

Potential

Seller

Cost

PS if

P=$40

Frank

$10

Gregory

$25

Hanna

$35

Ingrid

$45

Jacqueline

$55

○

Individual Producer Surplus

Gain a single seller gets from selling something

§

○

Total Producer Surplus

Sum of all of the individual producer surpluses

§

○

We can use the information on seller cost to construct a supply schedule and graphically

illustrate producer surplus.

On a graph, producer surplus is everything ABOVE THE SUPPLY CURVE & BELOW

THE PRICE.

§

○

•

Producer Surplus After a Price Change

What would happen to producer surplus after a price decrease?

○

•

All Together - Total Surplus

Total Surplus

Producer Surplus + Consumer Surplus

§

Illustrates one of the key economic principles: INCENTIVES

§

○

Markets are usually efficient.

This is when, in equilibrium, the Total Surplus is at a max.

§

○

EXAMPLE

Identify and calculate consumer surplus, producer surplus, and total surplus in the

following market.

§

○

•

Chapter 5

Price Controls

Policies that restrict how high or low a price can be

○

Price Ceiling

Dictates the MAX price sellers are allowed to charge for a good or service.

§

A common example is apartment rent laws in NYC.

§

○

Price Floor

Dictates the MIN price sellers are allowed to charge for a good or service.

§

A common example is minimum wage.

§

○

•

Modeling a Binding Price Ceiling

•

Deadweight Loss (DWL)

The loss in the total surplus whenever a policy or action distorts the quantity being

traded in a market away from the efficient Q.

§

○

Area of a Trapezoid

(Side1+ Side2)*Height / 2

§

○

Modeling a Binding Price Floor

•

What happens if a price floor is set above equilibrium price?

○

What happens if a price floor is set below equilibrium price?

○

Is the shift in demand or quantity

demanded? _________________

•

The two goods are ________________.

•

Is the shift in demand or quantity

demanded? _________________

•

Is the shift in demand or quantity

demanded? _________________

•

A market is in equilibrium when the

price in the market is such that

_________________ = ________________.

○

What would happen if a seller tried

to charge prices above what other

sellers were charging?

○

_________________________

What would happen if a buyer tried

to negotiate a price well below what

other buyers were paying?

○

_________________________

Consider the market for tennis shoes and

assume it is initially in equilibrium. An

increase in the popularity in running causes

the demand for tennis shoes to _____. As a

result, the _______ curve shifts to the______.

Initially, there is a ________ of tennis shoes.

This causes _____________________________.

○

Consider the market for chairs and

assume it is initially in equilibrium

○

Illustrate what would happen if the price

of wood INCREASED.

○

Total Effect:

Price ________

Quantity _____

Price ____, Quantity ___

Price ____, Quantity ____

Area ___ represents the original CS

before the price decrease.

○

Area ___ represents the increase in

CS to original buyers after the price

decreases.

○

Area ___ represents the increase in

CS gained by new buyers.

○

Area ___ represents the original PS

before the price increase.

○

Area ___ represents the increase in

PS to original sellers after the price

increase.

○

Area ___ represents the increase in

PS gained by new sellers entering.

○

Side effect of introducing a

binding price ceiling into an

efficient market:

Shortage

○

Inefficient Allocation

○

Wasted Resources (Time)

○

Low Quality

○

Black Markets

○

•

Side effect of introducing a binding

price floor into an efficient market:

Surplus

○

Inefficient Allocation of Products

○

Wasted Resources

○

Inefficiency of High Quality

○

Black Markets

○

•

Lecture 2

Sunday,*May*20,*2018

3:41*PM

Chapter 3

Supply & Demand

Competitive Markets

There are many buyers and sellers of the same good or service

§

No one buyer or seller's actions are able to influence the market price

§

○

Supply & Demand Model

You can identify what factors determine and affect the price and quantity of goods

being traded in a competitive market

§

○

•

Demand

QUESTION

How many cups of coffee would people buy if the price were $5? $4? $1?

§

Price

Quantity

Demanded

$5

1

$4

7

$3

15

$2

20

$1

25

○

Demand Schedule

Shows amount consumers are willing to buy at every price

§

○

Quantity Demanded

Amount consumers want to buy at a specific price

§

○

Demand Curve

Graphical representation of a demand schedule

§

○

Demand

The amount consumers want to purchase at EACH different price

§

This is the ENTIRE demand curve

§

○

Quantity Demanded

Amount consumers want to purchase for a specific curve

§

Graphically, this is ONE POINT on the demand curve

§

○

As the price of coffee decreases, the quantity demanded ____________.

Called the Law of Demand

All else equal, there is an INVERSE relationship between price and quantity

demanded.

As the price of a good ____, the quantity demanded ____.

®

As the price of a good ____, the quantity demanded ____.

®

□

§

○

•

Changes in Demand

All else equal means we are holding all other factors such as consumer income, tastes and

preferences, and the price of related goods constant.

○

What happens when one of these factors changes?

○

What happens to the demand for coffee during finals.

○

Price

Quantity

Demanded

(OLD)

Quantity

Demanded

(NEW)

$5

1

3

$4

7

12

$3

15

20

$2

20

24

$1

25

25

○

•

Factors that Demand Shift Demand

FACTOR 1: Change in Price of Related Goods

Two types of related goods

Compliments

□

Substitutes

□

§

Two goods are Compliments if:

INCREASE in the price of one good --> DECREASES the demand of the other good

□

These are goods that are typically consumed together

□

Example

You buy a coffee and bagel every morning. Bagel price goes up. You don't

want to drink coffee without eating your bagel. So you buy neither.

®

□

§

Two goods are Substitutes if:

INCREASE in the price of one good --> INCREASES the demand for the other good

□

These are goods that typically serve similar functions or are interchangeable

□

Example

Price of Coke increases, the demand for Pepsi increases

®

Price of coffee increases, the demand for tea goes up.

®

□

§

○

FACTOR 2: Change in Consumer Income

Normal Goods

Goods that when consumer income increases, the demand for them INCREASES

□

Example

Cars

®

House

®

□

§

Inferior Goods

Goods that when consumer income increases, the demand for them DECREASES

□

Example

Bus fair

®

Off-brand goods

®

□

§

○

FACTOR 3: Change in Tastes & Preferences

Examples

What is in in fashion

□

Change in food

□

Change in seasons

□

§

○

FACTOR 4: Change in Future Expectations

Examples

Extreme weather conditions

□

Investing in stock in a company that is starting to be good

□

Buying before Black Friday

□

§

○

FACTOR 5: Change in Number of Consumers

When we draw a Market Demand Curve, it is actually composed of several Individual

Demand Curves

§

○

•

The Market Demand Curve shows the quantity demanded for a good by all consumers

in the market at every given price.

§

It is the horizontal sum of all the individual demand curves.

§

As we add MORE consumers, the quantity demanded at every given price INCREASES

& the demand INCREASES.

§

CAREFUL!

Change in Demand

Caused by a change in one of the 5 factors listed.

□

Graphically, it is represented by a shift in the ENTIRE demand curve.

□

INCREASE in demand = shift the curve to the RIGHT

□

DECREASE in demand = shift the curve to the LEFT

□

§

Change in Quantity Demanded

Caused when the good's OWN price changes.

□

Graphically, represented by movement ALONG the demand curve.

Going from one point to another

®

□

§

○

PRACTICE PROBLEMS

Consider the market for popcorn. Illustrate what would happen if the price of DVDs

increased.

○

•

Once again, consider the market for popcorn. Illustrate what would happen if the price of

popcorn increased.

○

Assume popcorn is a normal good. Illustrate what would happen if consumer income

increased.

○

Which of the following would cause a DECREASE in demand for cars?

A decrease in the price of gasoline

A.

An increase in the price of cars

B.

An increase in the popularity of road trips

C.

An improvement in public transportation.

D.

○

Supply

Economists are also interested in modelling the behavior of sellers.

Much of this will look similar to what you saw when we were looking at consumers and

demanded.

§

○

Consider the following:

○

Price

Quantity

Supplied

$5

10

$4

8

$3

6

$2

4

$1

2

If the price is more, you will want to sell more

§

○

Supply Schedule

Graph that shows the amount of a good or service that will be supplied by sellers at

every given price

§

○

Quantity Supplied

Amount supplied at a SPECIFIC price

§

○

Supply Curve

Supply schedule represented graphically

§

○

Law of Supply

All else equal, there is a positive relationship between price and quantity supplied.

§

As the price of a good ____, the quantity supply____.

§

As the price of a good ____, the quantity supply ____.

§

○

•

Factors that Shift Supply

FACTOR 1: An input is any good or service used in production.

As input prices for a good INCREASE, supply _________ because ___________.

§

As input prices for a good DECREASE, supply _____________.

§

Example

Illustrate what happens to the supply of t-shirts if the price of cotton increases.

□

§

○

•

FACTOR 2: Change in Price of Related Goods

Two goods are Substitutes in Production if:

INCREASE in price of one good --> DECREASE the supply of the other good

□

These are goods that typically use the same resources

□

Producing one good prevents sellers from using resources to produce another.

□

Example:

Price for sandwiches goes up, you eat more bagels instead

®

□

§

Two goods are Compliments in Production if:

INCREASE in price of one good --> INCREASE the supply of the other good

□

Occurs if one good uses the product of the other

□

Example:

The price of beef increases, the price of leather increases

®

□

§

○

FACTOR 3: Technology

Improvements in technology should shift to the ________.

§

More efficient way to produce a good means that more of the good is being made,

supply goes ___.

§

Example:

Illustrate what effect the introduction of the assembly line had on the supply of

cars.

□

§

○

FACTOR 4: Expectations

If producers expect the price of a good to DROP in the future, supply will ____ in the

short run.

§

If producers expect the price of a good to INCREASE in the future, supply will ____ in

the short run.

§

○

FACTOR 5: Change in the Number of Producers

Similar to demand, the market supply curve is made up of several individual supply

curves

§

○

The market supply curve shows the quantity supplied or a good by all producers in the

market at every given price.

§

It is the horizontal sum of all the individual supply curves.

§

As we add more producers, the quantity supplied at every given price ___, and the

supply ____. Graphically, it becomes ___________.

§

CAREFUL!

Change in Supply

Caused by a change in one of the five factors.

§

Graphically, this is represented by a shift in the ENTIRE supply curve.

§

○

Change in Quantity Supplied

Occurs when the good's own price changes.

§

Graphically, this is represented by movement ALONG the supply curve.

§

○

We model an INCREASE in supply by shifting the supply curve to the _______.

○

We model an DECREASE in supply by shifting the supply curve to the _______.

○

•

Market Equilibrium

Equilibrium means that no one individual has the ability to make themselves better off by

doing something else.

○

•

Markets Move Towards Equilibrium

What happens when market price is above the equilibrium price? Below equilibrium price?

○

•

Changes in Market Equilibrium

What happens to market equilibrium when the demand curve shifts?

○

•

The INCREASE in demand causes prices to __________ and quantity to ____________.

§

What happens to market equilibrium when the demand curve shifts?

○

What happens to market equilibrium if both curves shifted simultaneously?

When both curves shift simultaneously, we can only determine the effect on P or Q,

NEVER both.

§

USEFUL TRICK:

Determine what the effect of each shift is separately, then combine to determine

the total effect.

□

§

Example:

Increase in Supply & Increase in Demand

□

§

○

Chapter 4

Consumer Surplus

The table below shoes the WTP for a Kennywood tickets.

○

Potential

Buyer

Willingness

to Pay

CS if

P=$45

Alice

$100

Bob

$85

Caroline

$60

David

$45

Evan

$40

Individual Consumer Surplus

Gain a single buyer gets from purchase

§

○

Total Consumer Surplus

Sum of all of the individual consumer surpluses

§

○

We can use the information on willingness to pay to construct a demand schedule and

graphically illustrate consumer to surplus.

On a graph, consumer surplus is everything BELOW THE DEMAND CURVE & ABOVE

THE PRICE.

§

○

•

Area of a Triangle

(Base*Height)/2

§

○

Consumer Surplus After a Price Change

•

What would happen if the price would have increased?

○

Producer Surplus

Potential

Seller

Cost

PS if

P=$40

Frank

$10

Gregory

$25

Hanna

$35

Ingrid

$45

Jacqueline

$55

○

Individual Producer Surplus

Gain a single seller gets from selling something

§

○

Total Producer Surplus

Sum of all of the individual producer surpluses

§

○

We can use the information on seller cost to construct a supply schedule and graphically

illustrate producer surplus.

On a graph, producer surplus is everything ABOVE THE SUPPLY CURVE & BELOW

THE PRICE.

§

○

•

Producer Surplus After a Price Change

What would happen to producer surplus after a price decrease?

○

•

All Together - Total Surplus

Total Surplus

Producer Surplus + Consumer Surplus

§

Illustrates one of the key economic principles: INCENTIVES

§

○

Markets are usually efficient.

This is when, in equilibrium, the Total Surplus is at a max.

§

○

EXAMPLE

Identify and calculate consumer surplus, producer surplus, and total surplus in the

following market.

§

○

•

Chapter 5

Price Controls

Policies that restrict how high or low a price can be

○

Price Ceiling

Dictates the MAX price sellers are allowed to charge for a good or service.

§

A common example is apartment rent laws in NYC.

§

○

Price Floor

Dictates the MIN price sellers are allowed to charge for a good or service.

§

A common example is minimum wage.

§

○

•

Modeling a Binding Price Ceiling

•

Deadweight Loss (DWL)

The loss in the total surplus whenever a policy or action distorts the quantity being

traded in a market away from the efficient Q.

§

○

Area of a Trapezoid

(Side1+ Side2)*Height / 2

§

○

Modeling a Binding Price Floor

•

What happens if a price floor is set above equilibrium price?

○

What happens if a price floor is set below equilibrium price?

○

Is the shift in demand or quantity

demanded? _________________

•

The two goods are ________________.

•

Is the shift in demand or quantity

demanded? _________________

•

Is the shift in demand or quantity

demanded? _________________

•

A market is in equilibrium when the

price in the market is such that

_________________ = ________________.

○

What would happen if a seller tried

to charge prices above what other

sellers were charging?

○

_________________________

What would happen if a buyer tried

to negotiate a price well below what

other buyers were paying?

○

_________________________

Consider the market for tennis shoes and

assume it is initially in equilibrium. An

increase in the popularity in running causes

the demand for tennis shoes to _____. As a

result, the _______ curve shifts to the______.

Initially, there is a ________ of tennis shoes.

This causes _____________________________.

○

Consider the market for chairs and

assume it is initially in equilibrium

○

Illustrate what would happen if the price

of wood INCREASED.

○

Total Effect:

Price ________

Quantity _____

Price ____, Quantity ___

Price ____, Quantity ____

Area ___ represents the original CS

before the price decrease.

○

Area ___ represents the increase in

CS to original buyers after the price

decreases.

○

Area ___ represents the increase in

CS gained by new buyers.

○

Area ___ represents the original PS

before the price increase.

○

Area ___ represents the increase in

PS to original sellers after the price

increase.

○

Area ___ represents the increase in

PS gained by new sellers entering.

○

Side effect of introducing a

binding price ceiling into an

efficient market:

Shortage

○

Inefficient Allocation

○

Wasted Resources (Time)

○

Low Quality

○

Black Markets

○

•

Side effect of introducing a binding

price floor into an efficient market:

Surplus

○

Inefficient Allocation of Products

○

Wasted Resources

○

Inefficiency of High Quality

○

Black Markets

○

•

Lecture 2

Sunday,*May*20,*2018

3:41*PM

Document Summary

There are many buyers and sellers of the same good or service. No one buyer or seller"s actions are able to influence the market price. You can identify what factors determine and affect the price and quantity of goods being traded in a competitive market. Shows amount consumers are willing to buy at every price. Amount consumers want to buy at a specific price. The amount consumers want to purchase at each different price. Amount consumers want to purchase for a specific curve. Graphically, this is one point on the demand curve. As the price of coffee decreases, the quantity demanded ____________. All else equal, there is an inverse relationship between price and quantity demanded. As the price of a good ____, the quantity demanded ____. All else equal means we are holding all other factors such as consumer income, tastes and preferences, and the price of related goods constant. What happens to the demand for coffee during finals.