33:390:310 Lecture Notes - Lecture 13: Standard Deviation, Weighted Arithmetic Mean, Covariance

Document Summary

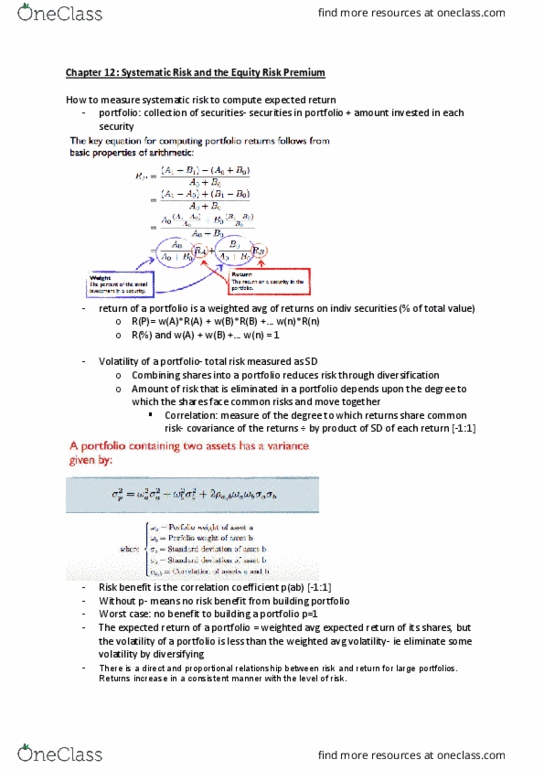

Suppose that an investor has estimates of the expected returns on individual securities and the correlations between securities. Obviously, the investor would like a portfolio with a high expected return and a low standard deviation of returns. The expected return of a portfolio is the weighted average of the expected returns on the individual securities: , or, the expected return of a portfolio = w1r1 + w2r2 + + wnrn. For two securities, a and b, the expected return = wara + wbrb. The formula for the variance of a portfolio comprised of two securities, a and b, is: (1) variance(portfolio) = Note that there are three terms on the right-hand side of equation (1). A , the second term involves the variance of stock b the variance of stock a third term involves the covariance between the two stocks.