33:390:400 Lecture Notes - Lecture 4: Net Present Value, Capital Structure, Earnings Before Interest And Taxes

11 May 2018

School

Department

Course

Professor

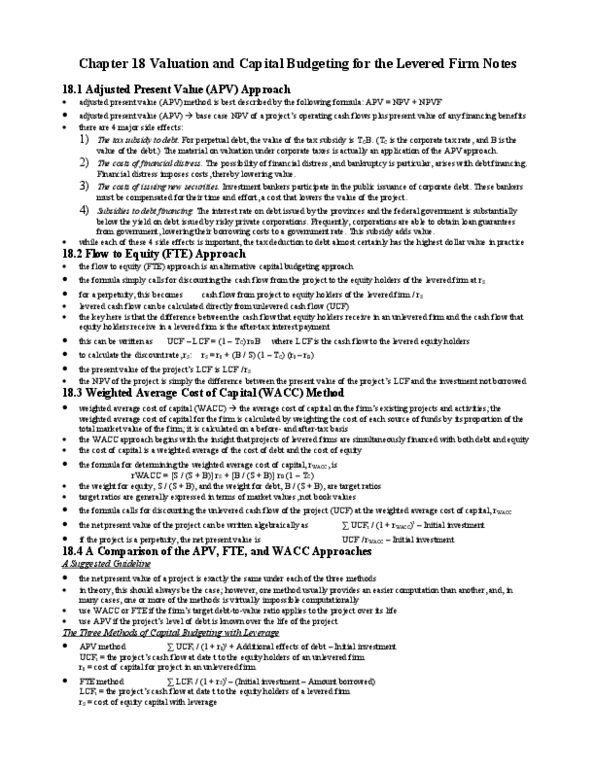

Chapter 18: Valuation and Capital Budgeting for the Levered Firm

Numerators:

Let UCF = Unlevered CF = CF that would accrue to shareholders if firm only uses equity

Let LCF = Levered CF = CF that would accrue to shareholders under current capital structure

Denominators:

R0 = Cost of capital if a firm only uses equity financing

RE = Cost of capital under current capital structure (w/ some debt)

RWACC = Weighted average cost of capital

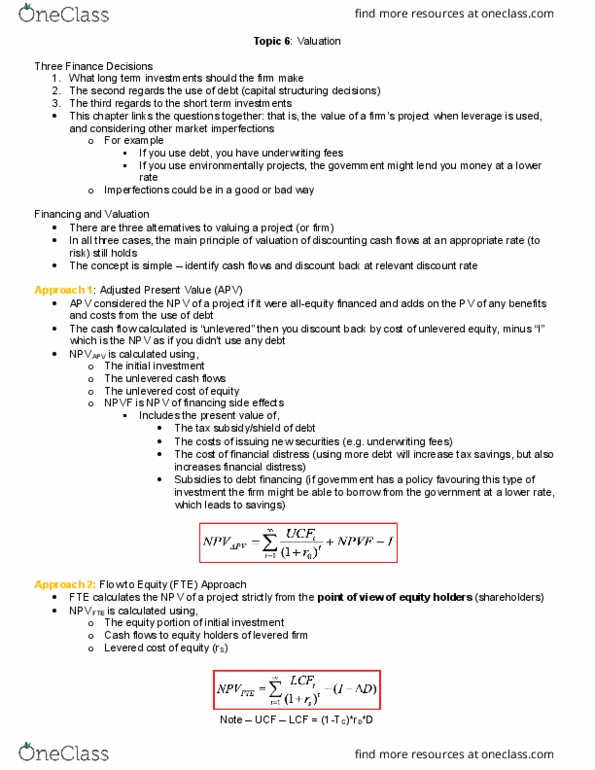

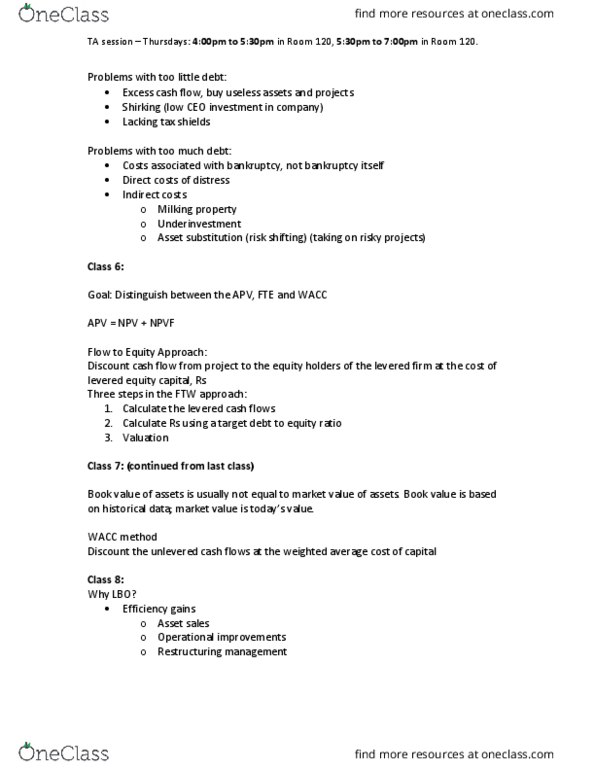

18.1 Adjusted Present Value Approach

Adjusted Present Value (APV): APV = NPV + NPVF

NPV = Value of a project to an unlevered firm

NPVF = NPV of the financing effects

There are four main side effects (NPVF)

1. Tax benefit from debt financing. This benefit is :(TC)x(RD)x(Debt). Most important

2. The costs of issuing new securities (IB costs, legal fees, etc.)

3. Expected financial distress costs from taking on a project

4. Subsidies to debt financing: Muni bonds are tax exempt will have a lower yield than

taxable bonds. No tax financing adds value

Example: Calculating APV w/ tax benefits to debt

Project:

Cash inflows of $500,000 per year Cash Costs = 72% of sales

Initial Investment = $475,000 TC = 34%, r0 = 20%

Step 1: Calculate UCF (unlevered cash flows)

Cash inflows (annual sales): $500,000

Cash costs (annual costs): (-$360,000)

Operating Income $140,000

Corporate Tax (34%) (-$47,600)

Unlevered Cash Flow (UCF) $92,400

Step 2: Calculate the PV of the Project:

CF/r0 = PV of CF

92,400/ 0.20 = $462,000

Step 3: Calculate the NPV (assuming no leverage)

(-Initial Cost) + (PV of CF) = (-$475,000) + $462,000 = (-$13,000)

- Since the NPV is negative, this project would be rejected by an all-equity firm

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Npv = value of a project to an unlevered firm. Chapter 18: valuation and capital budgeting for the levered firm. Let ucf = unlevered cf = cf that would accrue to shareholders if firm only uses equity. Let lcf = levered cf = cf that would accrue to shareholders under current capital structure. R0 = cost of capital if a firm only uses equity financing. Re = cost of capital under current capital structure (w/ some debt) Adjusted present value (apv): apv = npv + npvf. Example: calculating apv w/ tax benefits to debt. Step 2: calculate the pv of the project: tax benefit from debt financing. Most important: the costs of issuing new securities (ib costs, legal fees, etc. , expected financial distress costs from taking on a project, subsidies to debt financing: muni bonds are tax exempt will have a lower yield than. Tc = 34%, r0 = 20% taxable bonds.