ACC 151 Lecture Notes - Lecture 4: Retained Earnings, Accrual, Accounting Period

19 Jan 2016

School

Department

Course

Professor

Document Summary

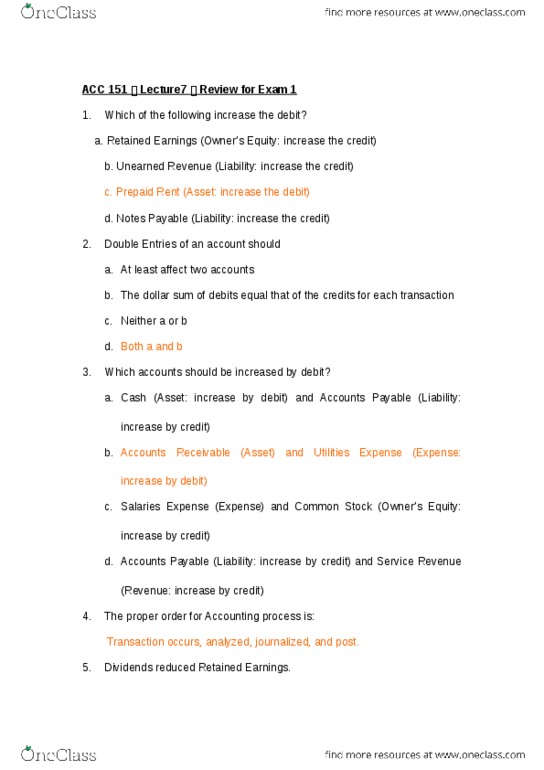

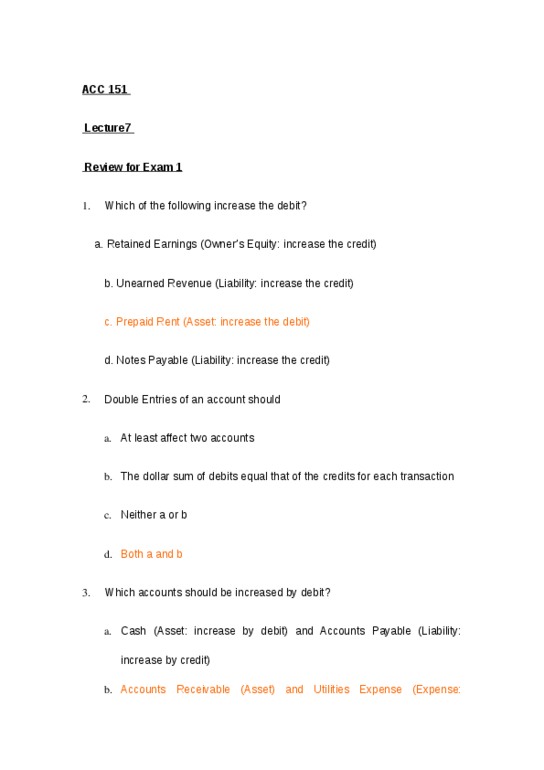

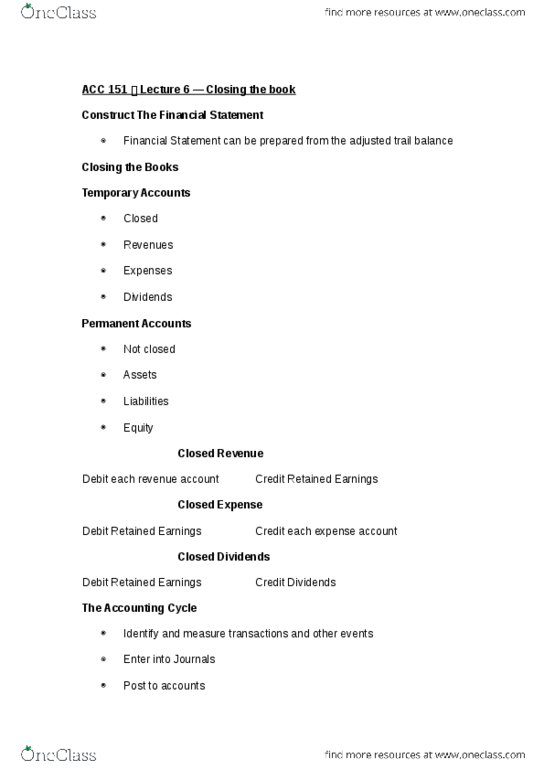

Analyzing the impact of business transactions on accounts. Record of increases and decreases in a specific asset liability, equity, or expense element. Total of all debits = total of all credits. Specify each account affected by the transaction and classify by type: determine if each account is increased or decreased (debit/credit, record in the journal. Copying information (posting) from the journal to the ledger. All the t-accounts combined make up the ledger. Entering a transaction in the journal does not get the data into the ledger. Data must be copied to the ledger a process called posting. Accounts posted to the ledger accounts: construct and use a trail balance. Records only cash transactions cash receipts and cash payments. Accrual accounting records cash and also noncash transactions, such as following. Accrual of expense incurred but not yet paid. Earning of revenue when cash was collected in advance. Ensures that accounting information is reported at regular intervals.