AC 210 Lecture Notes - Lecture 23: Accounts Payable, Purchase Order, Operating Expense

5 Jun 2018

School

Department

Course

Professor

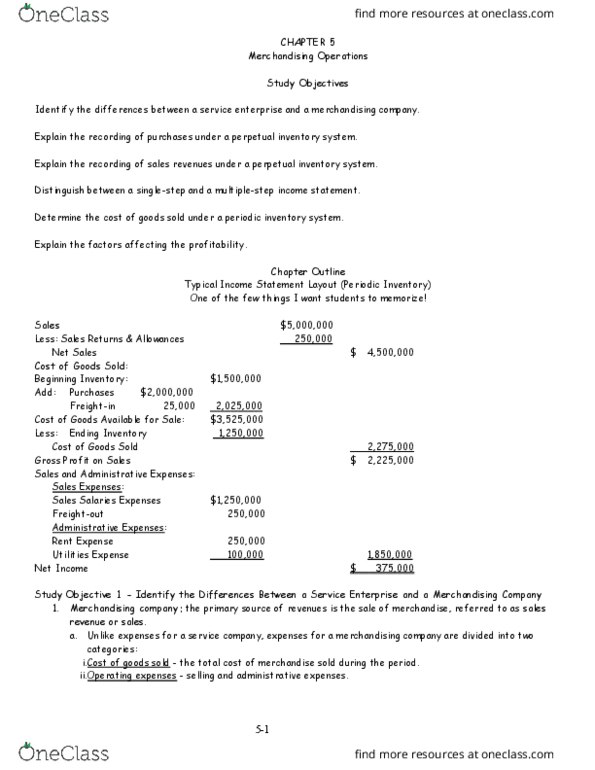

Inventory Systems

There are two systems to account for inventory: the perpetual system and the periodic

system. With the perpetual system, the inventory account is updated after every

inventory purchase or sale. Before computers became widely available, only companies

that sold a relatively small number of high‐priced items used this system. Under

the periodic system, a careful evaluation of inventory occurs only at the end of each

accounting period. At that time, each product available for sale is counted and multiplied

by its per unit cost, and the total of all such calculations equals the value of inventory.

Recording Purchases

Under the periodic system, a temporary expense account named merchandise

purchases, or simply purchases, is used to record the purchase of goods intended for

resale. The source documents used to journalize merchandise purchases include the

seller's invoice, the company's purchase order, and a receiving report that verifies the

accuracy of the inventory quantities. When Music World receives a shipment of

merchandise worth $1,000 on account from Music Suppliers, Inc., Music World

increases (debits) the purchases account for $1,000 and increases (credits) accounts

payable for $1,000.

For reference purposes, the journal entry's description usually includes the invoice

number.

When a seller pays to ship merchandise to a purchaser, the seller records the cost as a

delivery expense, which is considered an operating expense and, more specifically, a

selling expense. When a purchaser pays the shipping fees, the purchaser considers the

fees to be part of the cost of the merchandise. Instead of recording such fees directly in

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

There are two systems to account for inventory: the perpetual system and the periodic system. With the perpetual system, the inventory account is updated after every inventory purchase or sale. Before computers became widely available, only companies that sold a relatively small number of high priced items used this system. Under the periodic system, a careful evaluation of inventory occurs only at the end of each accounting period. At that time, each product available for sale is counted and multiplied by its per unit cost, and the total of all such calculations equals the value of inventory. Under the periodic system, a temporary expense account named merchandise purchases, or simply purchases, is used to record the purchase of goods intended for resale. The source documents used to journalize merchandise purchases include the seller"s invoice, the company"s purchase order, and a receiving report that verifies the accuracy of the inventory quantities.