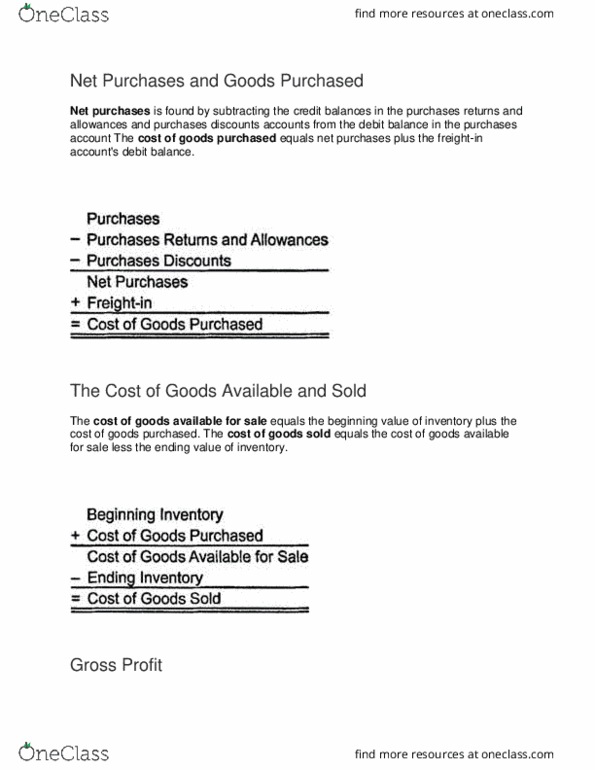

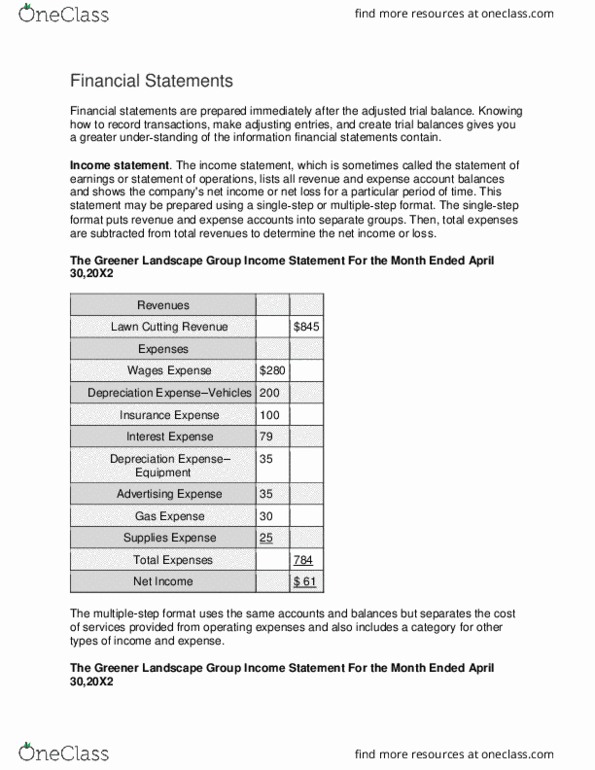

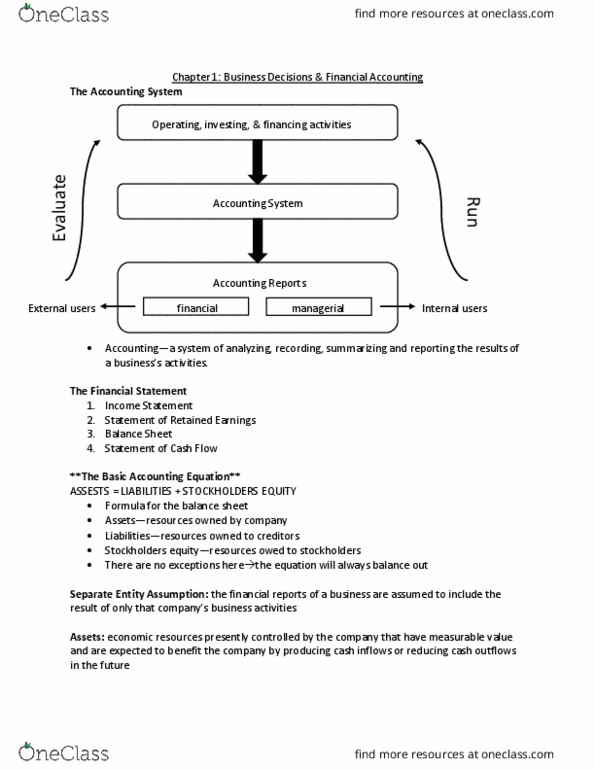

AC 210 Lecture Notes - Lecture 42: Gross Profit, Financial Statement, Balance Sheet

5 Jun 2018

School

Department

Course

Professor

Inventory Errors and Financial Statements

Income statement effects. An incorrect inventory balance causes an error in the

calculation of cost of goods sold and, therefore, an error in the calculation of gross profit

and net income. Left unchanged, the error has the opposite effect on cost of goods sold,

gross profit, and net income in the following accounting period because the first

accounting period's ending inventory is the second period's beginning inventory. The

total cost of goods sold, gross profit, and net income for the two periods will be correct,

but the allocation of these amounts between periods will be incorrect. Since financial

statement users depend upon accurate statements, care must be taken to ensure that

the inventory balance at the end of each accounting period is correct. The chart below

identifies the effect that an incorrect inventory balance has on the income statement.

Impact of Error on

Error in

Inventory

Cost of

Goods

Sold

Gross

Profit

Net Income

Ending

Inventory

Understated

Overstated

Understated

Understated

Overstated

Understated

Overstated

Overstated

Beginning

Inventory

Understated

Understated

Overstated

Overstated

Overstated

Overstated

Understated

Understated

Balance sheet effects. An incorrect inventory balance causes the reported value of

assets and owner's equity on the balance sheet to be wrong. This error does not affect

the balance sheet in the following accounting period, assuming the company accurately

determines the inventory balance for that period.

Impact of Error on

Error in

Inventory

Assets =

Liabilities

+

Owner's

Equity

Understated

Understated

No Effect

Understated

Overstated

Overstated

No Effect

Overstated

find more resources at oneclass.com

find more resources at oneclass.com

Estimating Inventories

Companies sometimes need to determine the value of inventory when a physical count

is impossible or impractical. For example, a company may need to know how much

inventory was destroyed in a fire. Companies using the perpetual system simply report

the inventory account balance in such situations, but companies using the periodic

system must estimate the value of inventory. Two ways of estimating inventory levels

are the gross profit method and the retail inventory method.

Gross profit method. The gross profit method estimates the value of inventory by

applying the company's historical gross profit percentage to current‐period information

about net sales and the cost of goods available for sale. Gross profit equals net sales

minus the cost of goods sold. The gross profit margin equals gross profit divided by

net sales. If a company had net sales of $4,000,000 during the previous year and the

cost of goods sold during that year was $2,600,000, then gross profit was $1,400,000

and the gross profit margin was 35%.

Net Sales

$ 4,000,000

Less: Cost of Goods Sold

(2,600,000)

Gross Profit

$ 1,400,000

If gross profit margin is 35%, then cost of goods sold is 65% of net sales.

Suppose that one month into the current fiscal year, the company decides to use the

gross profit margin from the previous year to estimate inventory. Net sales for the month

were $500,000, beginning inventory was $50,000, and purchases during the month

totaled $300,000. First, the company multiplies net sales for the month by the historical

gross profit margin to estimate gross profit.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

An incorrect inventory balance causes an error in the calculation of cost of goods sold and, therefore, an error in the calculation of gross profit and net income. Left unchanged, the error has the opposite effect on cost of goods sold, gross profit, and net income in the following accounting period because the first accounting period"s ending inventory is the second period"s beginning inventory. The total cost of goods sold, gross profit, and net income for the two periods will be correct, but the allocation of these amounts between periods will be incorrect. Since financial statement users depend upon accurate statements, care must be taken to ensure that the inventory balance at the end of each accounting period is correct. The chart below identifies the effect that an incorrect inventory balance has on the income statement. An incorrect inventory balance causes the reported value of assets and owner"s equity on the balance sheet to be wrong.