ACTG 2300 Lecture 20: Day 20 Notes

7 Feb 2017

School

Department

Course

Professor

Document Summary

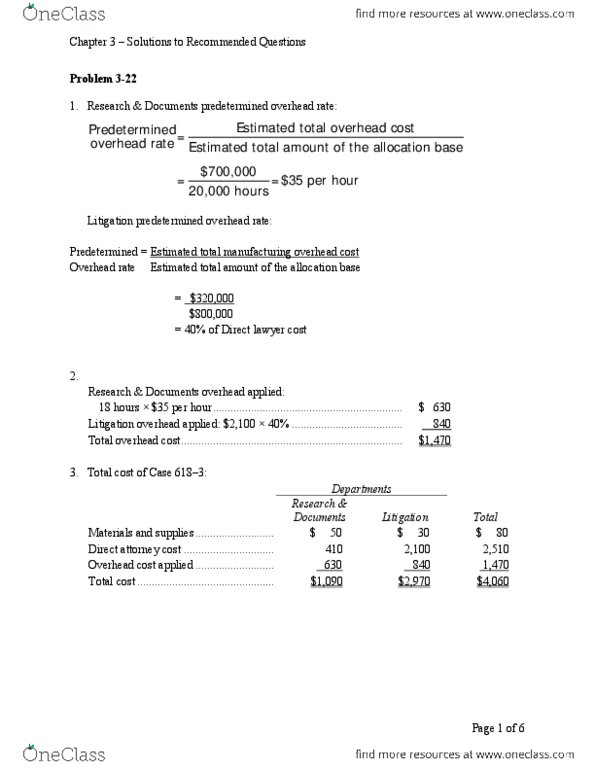

Variable = . 00 / hour * 20,000 hours = ,000 / hour. ---- #1 / #2 = . 70 per direct labor hour. ---- #1 / #2 = . 40 per direct labor hour. Actual allocation base incurred by each cost object. Difference between the manufacturing overhead cost applied (moca) and the actual manufacturing overhead cost (amoc) Manufacturing overhead applied > actual manufacturing overhead. Manufacturing overhead applied < actual manufacturing overhead. If not a large difference between applied and actual: overallocation = decrease cogs, underallocation = increase cogs. Overallocation - decrease: cogs, finished goods (fg) inventory, work in progress (wip) inventory. Underallocation - increase: cogs, finished goods (fg) inventory, work in progress (wip) inventory. 80,000 20,000 y = a + bx. 180 = a + . 00(20,000) a = ,000: y = 140,000 + 2. 00x y = 140,000 + 2. 0(60,000) y = ,000 = man. = ,000 = total manufacturing costs (4th quarter)