FIN 3410 Lecture Notes - Lecture 9: Foreign Exchange Spot, Call Option

7 Feb 2017

School

Department

Course

Professor

Document Summary

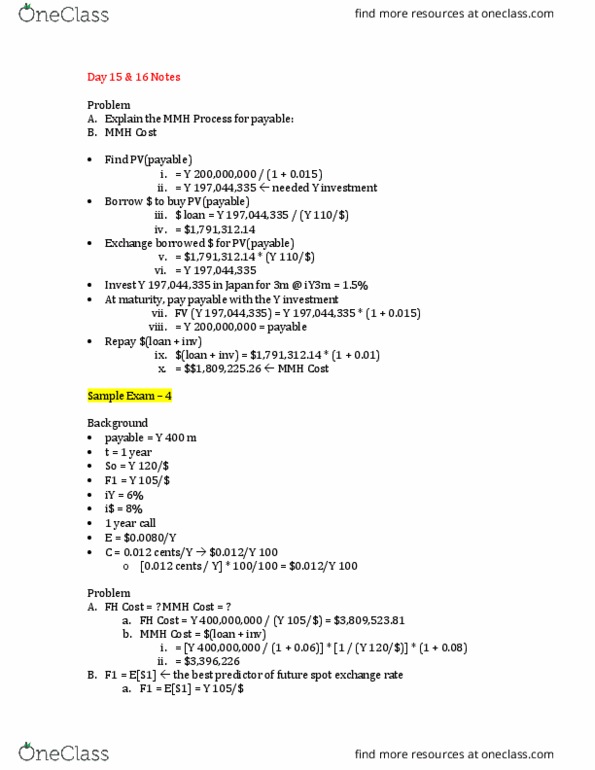

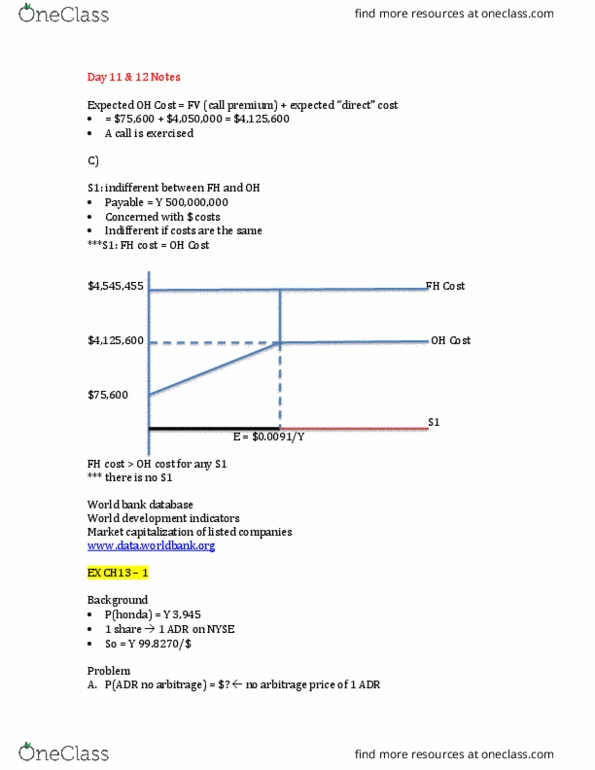

E = sh. 64/sf exercise (strike) price. E[s3] = f3m = sh. 63/sf: e[s3] = expected spot exchange rate in 3 months. I$ = 6% per annum: im = 6%/4 = 1. 5% Isf = 4% per annum: im = 4%/4 = 1% Expected oh cost: payable = sf 5,000, hedge with a long call (b/c payable, purchase the right to buy sf 5,000 in 3m @ e = sh. 64/sf, gives protection against sf appreciation. O( cost @ maturity in 3m = fv (cid:523)call premium(cid:524) + (cid:498)direct(cid:499) cost (cid:498)direct (cid:499) cost of purchasing sf 5,000: s3m > e = sh. 64/sf, then a call is exercised, buy sf 5,000 @ e = sh. 64/sf. Sf 5,000 * sh. 64/sf = ,200: s3m < e = sh. 64/sf, then a call is not exercised, buy sf 5,000 in spot market at s3m. Fv (call premium) = call premium * (1 + im: = sh. 05/sf * sf 5,000 * 1. 015 = . 75.