BMGT 340 Lecture Notes - Lecture 3: Financial Statement, Fokker E.Ii, Accrual

15 Sep 2016

School

Department

Course

Professor

Document Summary

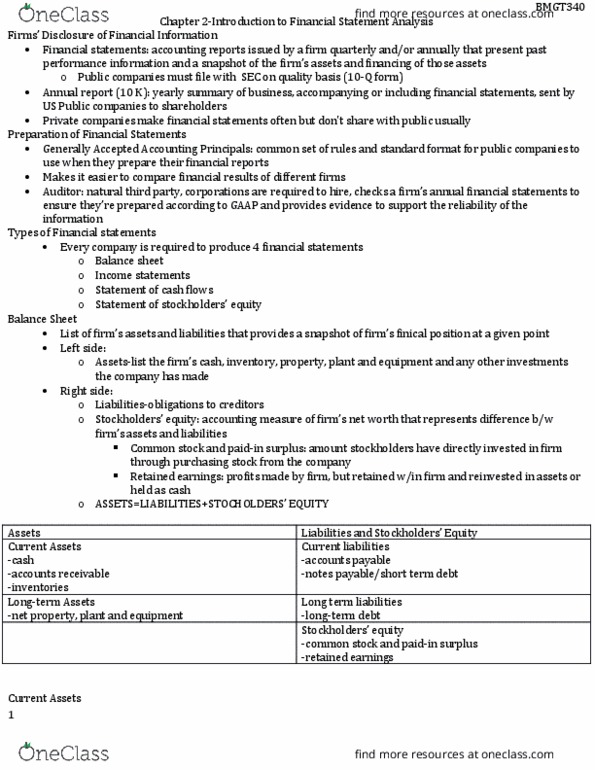

Chapter 2: introduction to financial statement analysis: firm"s disclosure of financial information, four financial statements required by the sec are a. i. The statement of stockholders equity: the accuracy of these are checked by b. i. Public companies that must use a common set of rules and standard format when they prepare their reports b. ii. Corporations are required to hire a neutral party, known as an b. iii. auditor, to check the annual financial statements, ensure that the statements are prepared according to gaap and provide evidence to support the reliability of the information. In addition to the auditor"s role in reviewing the financial statements, the sarbanes-oxley act requires both the ceo and. Cfo to personally attest to the accuracy of the financial statements presented to shareholders and to sign a statement to that effect: balance sheet overview, the balance sheet identity: a. i. ^^^ top 3 current assets in liquidity rankings ^^ d. v. long term assets/ net fixed assets/ net ppe.