ACC 311 Lecture Notes - Lecture 8: Historical Cost

31 Mar 2018

School

Department

Course

Professor

Document Summary

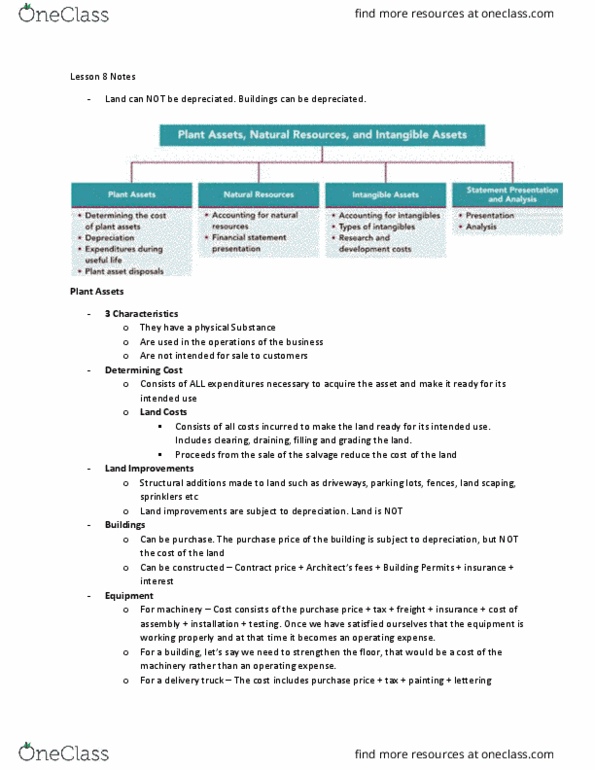

Property plant & equipment: acquired for use in operations and not for resale, long-term in nature and usually depreciated, they possess physical substance. Most companies use historical cost to value it. Purchase price, freight costs, sales taxes and installation costs, depreciation, replacement/improvement costs. Purchase price, closing costs, costs to get land ready for intended use (grading, filling, draining, clearing), assumption of liens or mortgages, etc. , and any additional land improvements that have indefinite life. Improvements with limited lives are recorded separately (driveways, fence, parking lots) Materials, labor and overhead costs incurred during construction; professional fees and building permits. Purchase price, freight and handling charges, insurance while in transit, special foundation costs if required, assembling and installation, and cost of conducting trial runs. Can deal with indirect costs by either assigning no fixed overhead to the cost of the constructed asset or assigning a portion of all overhead to the construction process (full-costing approach)