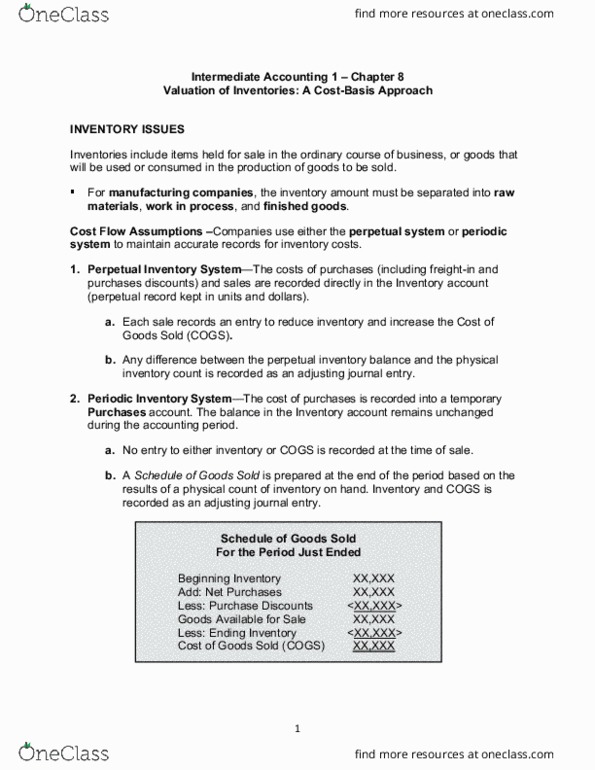

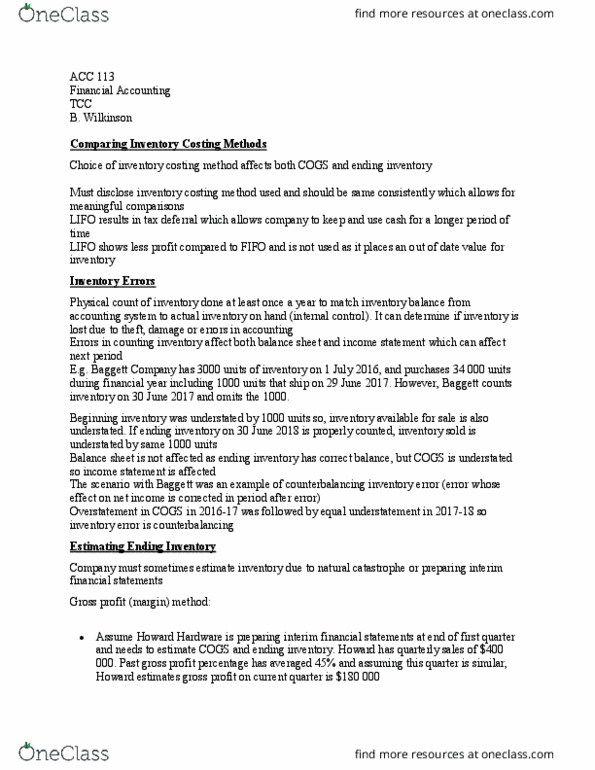

ACC 311 Lecture Notes - Lecture 9: Cost Accounting, European Cooperation In Science And Technology, Matching Principle

Document Summary

Get access

Related Documents

Related Questions

Multiply the LIFO layerby the base year price index and the current year cost-to-retailpercentage. Multiply the LIFO layerby the layer year price index and by the layer year cost-to-retailpercentage. Divide the LIFO layer bythe layer year cost-to-retail percentage and multiply by the layeryear price index. |

Compare beginning andending inventory amounts after adjusting both amounts to theaverage price level for the year. Inflate beginninginventory amount to end of year prices and compare to endinginventory amount. Deflate the endinginventory amount to beginning of year prices and compare to thebeginning inventory amount. |

$360,000. $395,000. $455,000. |

Combines retail LIFOaccounting with dollar-value LIFO accounting Allows companies toreport inventory on the balance sheet at retail prices. All of the above arecorrect. |

Added to netpurchases. Added to interestincome. Deducted frompurchases. |

LIFO. Weighted average. None of the above. |

Beginning inventory +accounts payable - net purchases. Net purchases + endinginventory - beginning inventory. Net Purchases + beginninginventory - ending inventory. |

Reliability. Consistency. Objectivity. |

A deferral of incometax. Simplifiedrecordkeeping. A permanent reduction ofincome taxes. |

Assets intended to besold in the normal course of business. Equipment used in themanufacturing of assets for sale. Assets currently inproduction for normal sales. |

1. Claremont Corp has the following inventory balances for 2009:beginning, $468,000; ending, $444,000. The companyâs cost of goodssold for the year was $4,370,400.

What was Claremont Corp.âs average inventory for 2009?

What is the companyâs inventory turnover ratio?

Calculate the average age of inventory for Claremont Corp.

Assume that Claremont Corp is a retail toy company, and itsfiscal year-end is December 31. Would Claremontâs inventory be atan annual high or low at the end of the year? In this situation,would the inventory turnover ratio provide valid information to adecision maker? Why or why not?

Given the information in Part D, how might you obtain a betterindication of the average amount of inventory that Claremont Corphand on-hand during the year?

2. Itâs Good, YâAll! is a Texas-based company that operates alarge chain of restaurants. The following information is availablefor the company (in thousands):

| Category | 2007 | 2008 | 2009 |

|---|---|---|---|

| Net Sales | $400,577 | $517,616 | $640,898 |

| Cost of Goods Sold | $130,885 | $171,708 | $215,071 |

| Net Income | $33,943 | $46,652 | $57,497 |

| Ending Inventory | $23,192 | $28,426 | $41,989 |

Compute the companyâs inventory turnover ratio and age ofinventory for 2007 through 2009. Beginning inventory for 2007 was$15,746,000.

Comment on the ratios computed in Part A. Are there any definitetrends in theses ratios? If so, are these trends favorable orunfavorable? Explain.

Why do decision makers pay close attention to the age of aninventory statistic for companies in the restaurant industry?

3. Li Enterprises recently purchased new computer equipment forits company headquarters. The following is information regardingthe various cash expenditures related to the acquisition of thisequipment:

The invoice price of the equipment was $300,000, however, Liâsowner negotiated a 15% price reduction.

The equipment was shipped to Liâs headquarters FOB shippingpoint. The delivery cost was $2,750.

Li paid $1,870 to hire a computer consultant to install and testthe new equipment.

Supplies costing $135 were used in installing and testing theequipment.

The day following the installation of the equipment, one of Liâsemployees broke a USB port on the computer equipment. The companypaid $265 to have the port replaced.

Determine the acquisition cost of the computer equipment foraccounting purposes.

A computer purchased for several thousand dollars may havelittle resale value one year later because of technological changesin the computer industry. Given that the resale value of computersand computer equipment can decline rapidly, is historical cost theproper valuation basis to use for such assets? Defend youranswer.