ACCT 200 Lecture Notes - Lecture 13: Wheaties, Income Statement, Macrs

19 Oct 2016

School

Department

Course

Professor

Document Summary

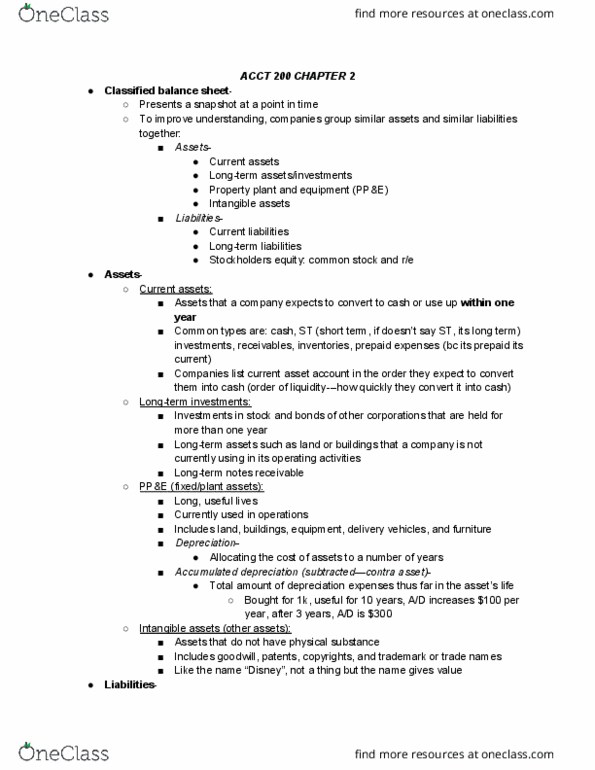

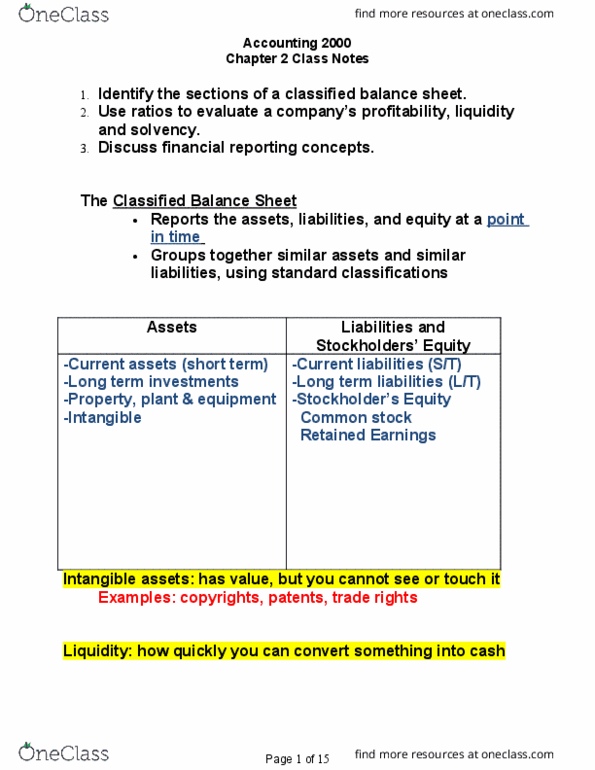

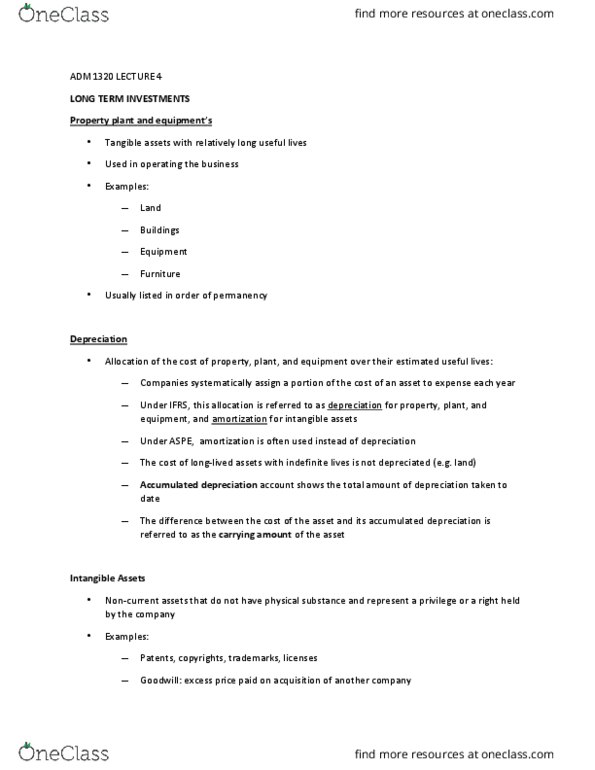

Plant assets: property, plant, and equipment (physical assets) that a company owns. Intangible assets: assets such as copyrights and patents that lack physical substance but can be e(cid:454)tre(cid:373)el(cid:455) (cid:448)alua(cid:271)le a(cid:374)d (cid:448)ital to a (cid:272)o(cid:373)pa(cid:374)(cid:455)"s su(cid:272)(cid:272)ess. Plant assets are resources that have physical substance and are not intended for sale to customers. Are expected to be of service to company for a number of years. All plant assets except for land decline in service potential over their useful lives. Pla(cid:374)t assets deter(cid:373)i(cid:374)e a (cid:272)o(cid:373)pa(cid:374)(cid:455)"s (cid:272)apa(cid:272)it(cid:455) a(cid:374)d a(cid:271)ilit(cid:455) to satisf(cid:455) (cid:272)usto(cid:373)ers. It is important for a company to: keep assets in good operation condition, replace worn-out or outdated assets, expand productive assets as needed. Investments in plant assets are substantial for many companies. Historical cost principle requires that companies record plant assets at cost. Cost consists of all expenditures necessary to acquire an asset and make it ready for its intended use.