MGMT 4A Lecture Notes - Lecture 4: Rent Regulation, Price Floor, Price Ceiling

Document Summary

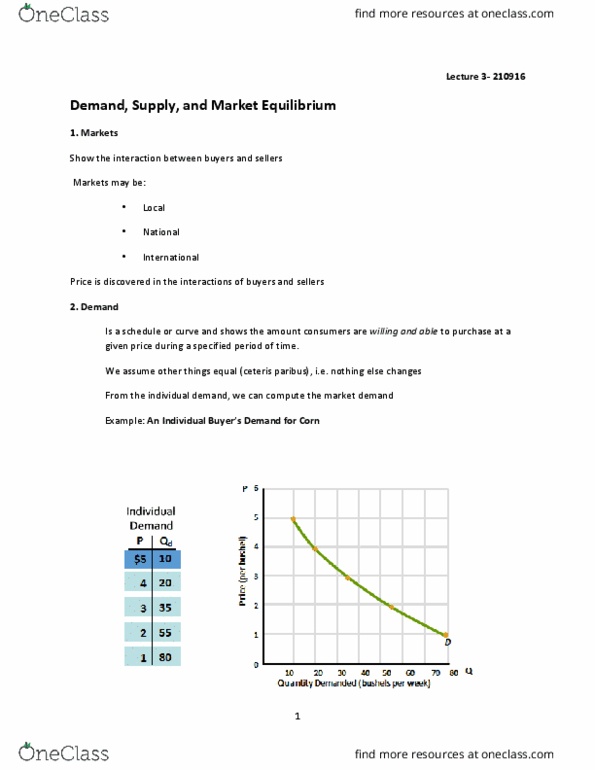

Oil prices rise=oil production rises; food prices fall=resources driven out of agriculture. Those w/ higher incomes as a group will end up w/ larger houses, more clothing, etc. They move the demand curve inward or outward. Beef price rises, consumers substitute other meals. Distinguishing shifts vs. movements helps pinpoint source price change. Market demand curve: horizontal sum of individual demand curves. Shift out- indicates more supply at any given price. Shift in- indicates less supply at any given price. Factors of production: land & labor, capital, and energy & natural resources. Flat slope: small change in price = large change in quantity demanded (elastic demand) Steep slope: large change in price = small change in quantity demanded (inelastic demand) Surplus: an excess of the quantity supplied over the quantity demanded. Shortage: an excess of the quantity demanded in the market over the quantity supplied.