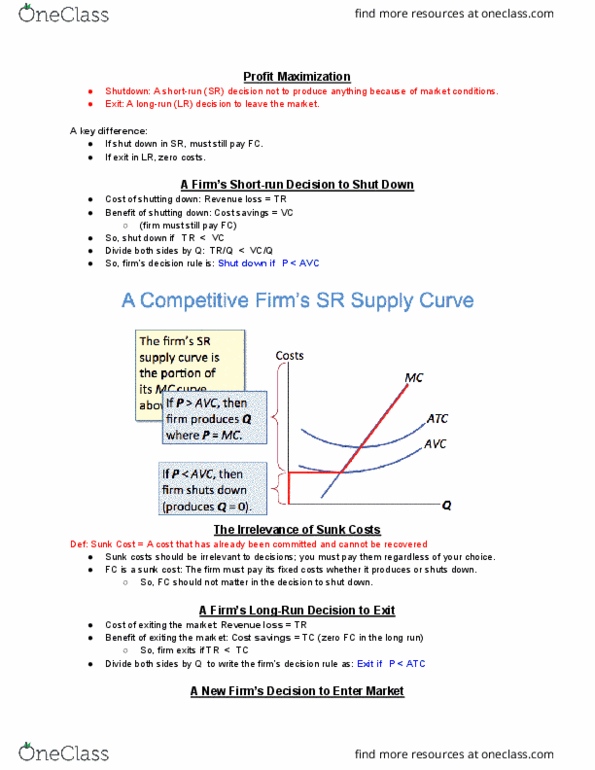

ECON 1 Lecture Notes - Lecture 14: Fixed Cost, Farmer Jack, Marginal Product

Chapters 13 and 14: Costs and Profit Maximization Under Competition

- We assue that the fir’s goals is to aiize profit

o Profit = total revenue – total cost

o Total revenue – the amount a firm receives from the sales of its output

o Total cost – the market value of the inputs a firm uses in production

- Explicit costs – require an outlay of money

o Ex: paying wages to workers

- Implicit costs – do not require a cash outlay

o E: the opportuit ost of the ower’s tie

- Remember one of the Ten Principles: the cost of something is what you give up to get it

- This is true whether the osts are ipliit or epliit. Both atter for firs’ deisios

- Ex: costs – explicit vs implicit

o You need $100,000 to start your business. The interest rate is 5%

o Case 1: borrow $100,000

o Explicit cost = $5000 interest on loan

o Case 2: use $40,000 of your savings, borrow the other $60,000. Assume your savings account pays

5% interest

o Explicit cost = $3000 (5%) interest on the loan

o Implicit cost = $2000 (5%) foregone interest you could have earned on your $40,000

o In both cases, the total (explicit + implicit) costs are $5000

- Accounting profit – total revenue minus total explicit costs

- Economic profit – total revenue minus total costs (including explicit and implicit costs)

- Accounting profit ignores ipliit osts, so it’s higher tha eooi profit

- Ex: economic profit vs accounting profit

o The equilibrium rent on office space has just increased by $500/month

o Determine the effects on accounting profit and economic profit if

▪ A) you rent your office space

• Explicit costs increase $500/month

• Accounting profit and economic profit each fall $500/month

▪ B) you own your office space

• Explicit costs do not change, so accounting profit does not change

• Implicit costs increase $500/month (opportunity cost of using your space instead of

renting it), so economic profit falls by $500/month

- Production function – shows the relationship between the quantity of inputs used to produce a good and

the quantity of output of that good

o Can be represented by a table, equation, or a graph

o Ex: farmer jack grows wheat, has 5 acres of land, he can hire as many workers as he wants

o If jack hires one more worker, his output rises by the

marginal product of labor

o Marginal product of any input – the increase in output

arising from an additional unit of that input, holding all other

inputs constant

▪ Notation: ∆ delta = hage i…

▪ Examples: ∆Q – change in output, ∆L – change in labor

▪ Marginal product of labor (MPL): (∆Q/∆L)

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Chapters 13 and 14: costs and profit maximization under competition. Explicit costs require an outlay of money: ex: paying wages to workers. Implicit costs do not require a cash outlay: e(cid:454): the opportu(cid:374)it(cid:455) (cid:272)ost of the ow(cid:374)er"s ti(cid:373)e. Remember one of the ten principles: the cost of something is what you give up to get it. This is true whether the (cid:272)osts are i(cid:373)pli(cid:272)it or e(cid:454)pli(cid:272)it. Ex: costs explicit vs implicit: you need ,000 to start your business. The interest rate is 5: case 1: borrow ,000, explicit cost = interest on loan, case 2: use ,000 of your savings, borrow the other ,000. 5% interest: explicit cost = (5%) interest on the loan. Implicit cost = (5%) foregone interest you could have earned on your ,000. In both cases, the total (explicit + implicit) costs are . Accounting profit total revenue minus total explicit costs.