HIST 1402 Lecture Notes - Lecture 12: United States Treasury Security, Yield Curve

Document Summary

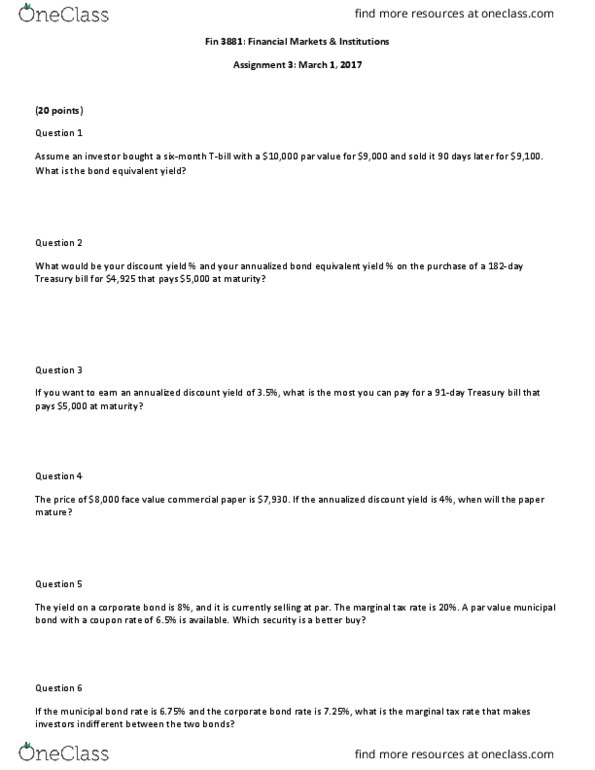

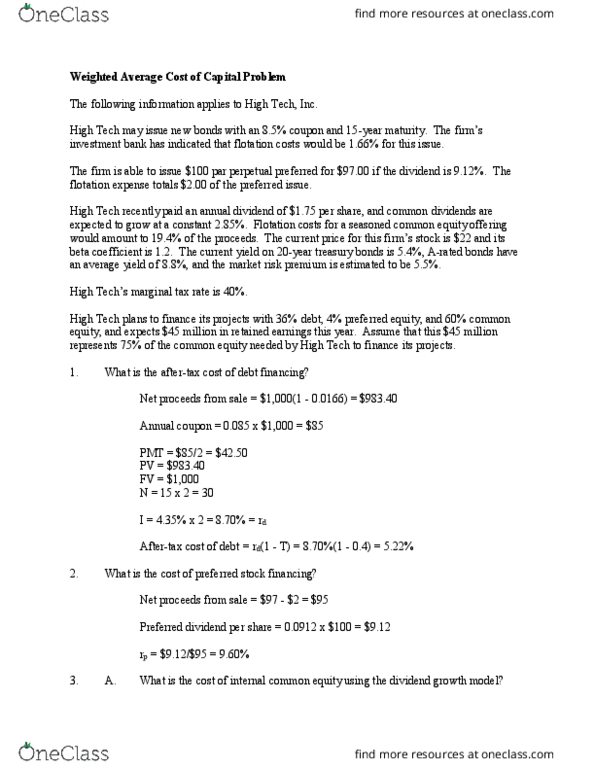

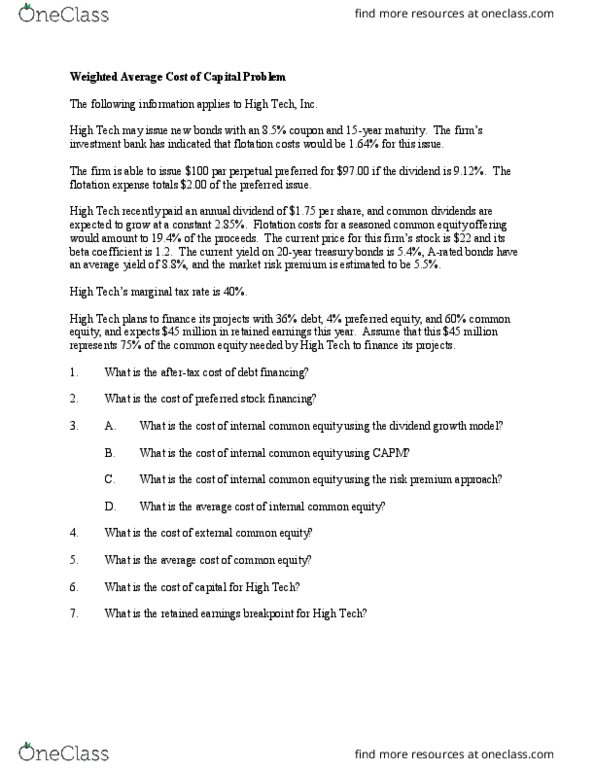

Due february 6, 2017 (20 points) (2 points) question 1. The current one-year treasury-bill is 6. 7% and the expected one-year rate 12 months from now is 8. 8%. According to the unbiased expectation theory, what should be the current rate for a two- year treasury security? (4 points) question 2. Assume that the current one-year rate and expected one-year t-bill rates over the following three years are as follows: 1r1 = 6% , e(2r1)=8%, e(3r1)= 8. 5%, e(4r1)=9. 1% , e(5r1)= 10. 3: calculate the long-term rates for 1, 2, 3, 4, and 5 year maturity treasury securities, plot the yield curve (4 points) question 3. Use the following spot rates 1r1= 6%; 1r2= 8%; 1r3= 11% to find. What is the duration of a bond with a 3 year remaining if the bond has a coupon rate of 6. 4 % paid semiannually, and the market interest rate is 4. 9%? (6 points) question 5. You are given information about the following two bonds: