ECON 1201 Lecture Notes - Lecture 10: Perfect Competition, Takers, Taipei Metro

7 Nov 2016

School

Department

Course

Professor

74

ECON 1201 Full Course Notes

Verified Note

74 documents

Document Summary

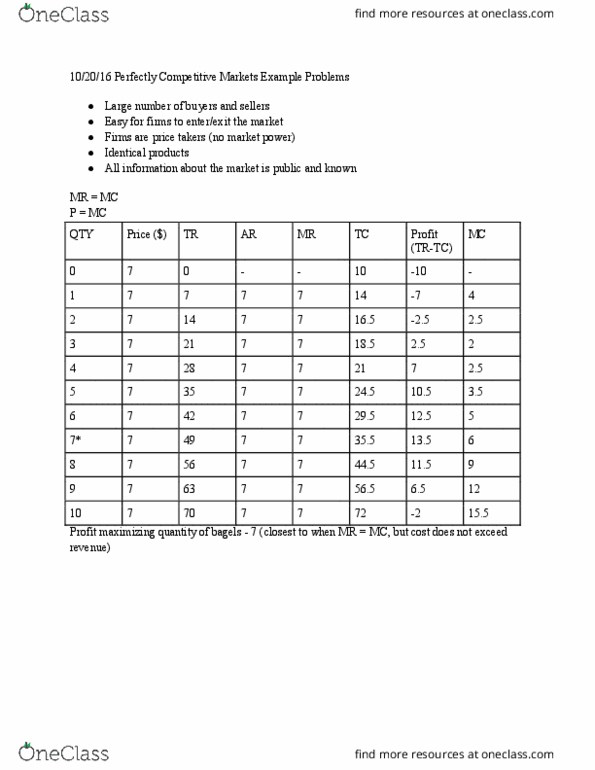

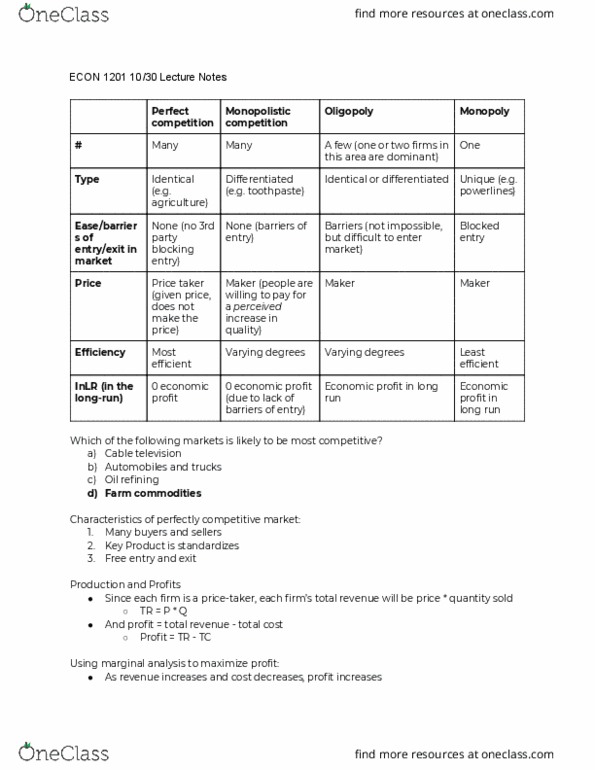

Consumer"s" objective is to maximize utility subject to budget. They decide how much to consume given the price of the product and their income. Producer/firm"s objective is to minimize costs (maximize profit) Decisions that firms make and influence cost of production. What the price the product should be. Do not influence market price of a product. Assumes a large number of sellers and buyers. Can influence market price of a product. Assumes only one seller with no close substitute. Occurs before entry or exit of firms takes place. Occurs after all entry or exit of firms takes place. Fixed cost - independent of output (or level of production) Fixed cost + variable cost = total cost (we won"t discuss the cost associated with economic profit because we won"t discuss economic profit) Average fixed cost = fixed cost / quantity. Average variable cost = variable cost / quantity. Average fixed cost + average variable cost = average cost.