MGT 135 Lecture Notes - Lecture 13: S Corporation, Payroll Tax, Preferred Stock

27 Mar 2020

School

Department

Course

Professor

Document Summary

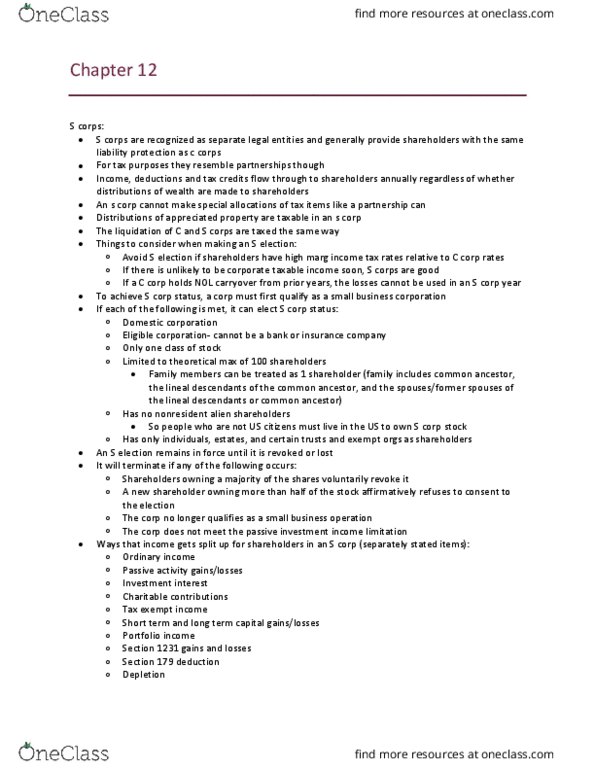

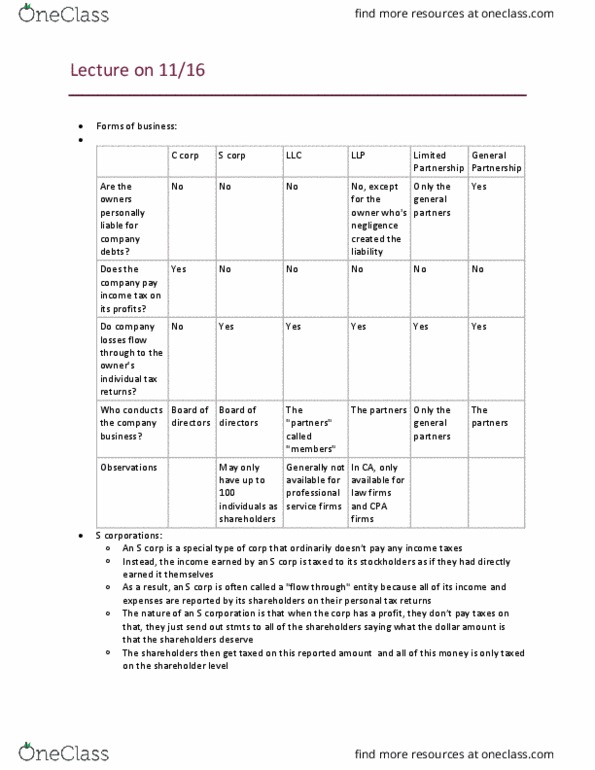

Subchapter s corporation. : advatanges, (1) limited liability, (2) pass through entity (meaning that s corps are not taxed, there are 3 statutory requirements, 1. Shareholders can only be individuals, estates, trusts, tax exempt organizations. (does not include partnerships, other companies and c corps: 2. Number of shareholders is limited to 100: 3. Subchapter s corp (i. e s corp) can only have one single class of outstanding stock. (no preferred stock) very simple. Just one class of stocks: salary payments, owner can be an employee, can be paid a salary. Payroll tax is withheld consequently: important difference between an s corp and a partnership. 3: basis limitation on loss deductions and computing the adjusted basis of s corp stock: both of these concepts are the same as for a partnership. Chapter 11: corporate taxpayer: legal characteristics of a corporation, 4 primary legal characteristics.