ACCT208 Lecture Notes - Lecture 3: Activity-Based Costing, European Cooperation In Science And Technology, Deutsche Luft Hansa

1 Apr 2016

School

Department

Course

Professor

Document Summary

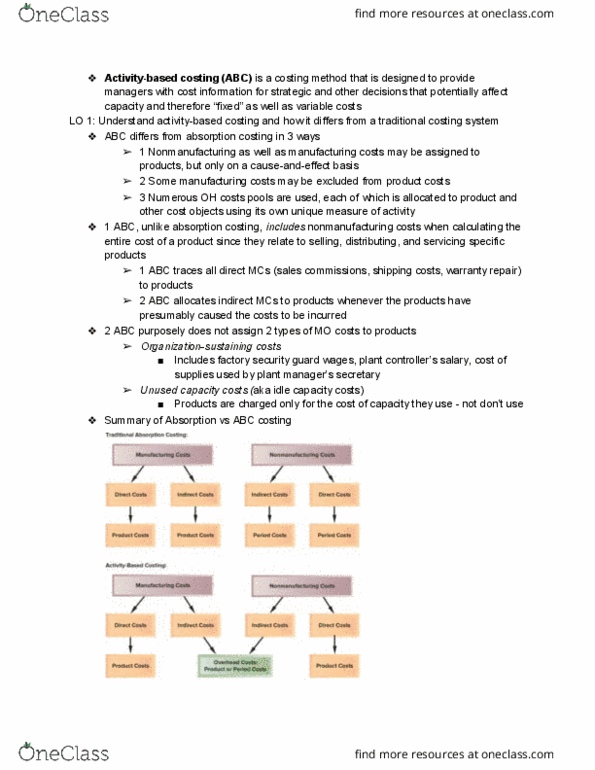

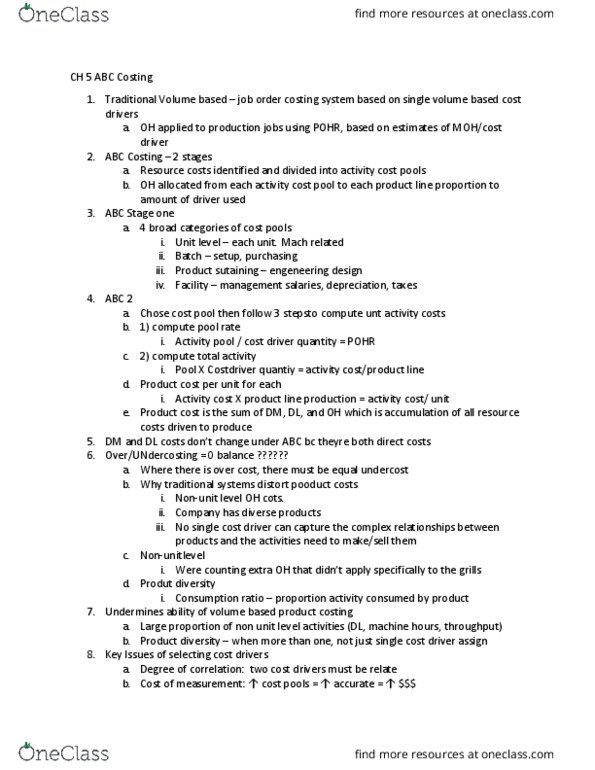

Chapter 3 lecture outline: abc - activity based costing. Activity based costing a supplemental cost system to normal costing. Objective: understand & manage oh and how it affects products/services. *basically do it by having multiple oh pools instead of 1: basic differences between traditional (absortpion/normal) and abc system. Include some nonmanufacturing costs in the cost of the product: selling, distributing, servicing product. Exclude some traditional cost: theses are cost not caused by product, some factory costs c. Would we still incur the cost of this product line was dropped? . Cost drivers and cost pools: activity = same as cost driver, activity pool = oh pool, pohr = activity rate. Using abc for determining cost of a product steps using handout 1. First stage allocation: from 1 oh pool to separate or smaller oh pools: usually given as % total oh/cost. Total pool - dlh + set ups + p,o. Link activity pools (overhead pools) to related activities (cost drivers)