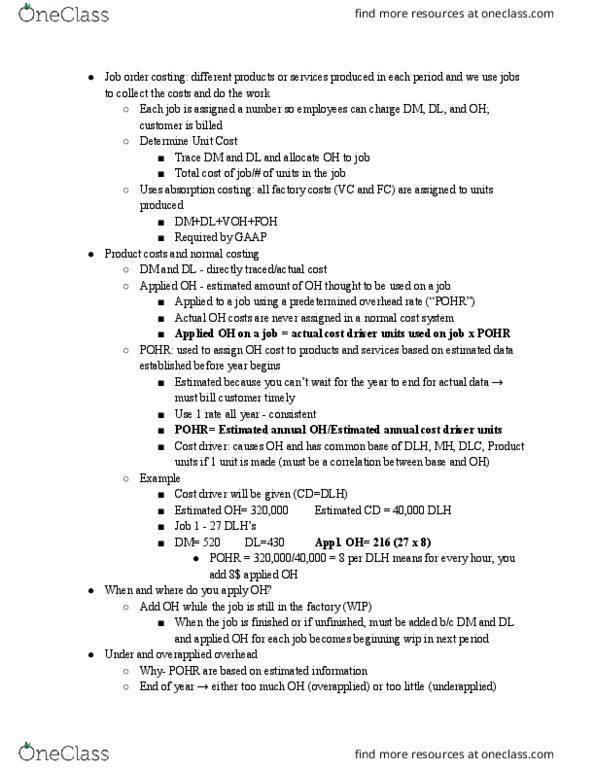

ACCT208 Lecture Notes - Lecture 3: Deutsche Luft Hansa, Direct Labor Cost, Cost Driver

Document Summary

Get access

Related Documents

Related Questions

| Exhibit 1Wilkerson Company: Operating Results (March 2000) | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Sales | $2,152,500 | 100% | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Direct Labor Expense | $271,250 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Direct Materials Expense | 498,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Manufacturing Overhead | ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Machine-relatedexpenses | $313,600 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Setup labor | 32,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Receiving andproduction control | 192,900 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Engineering | 100,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Packaging andshipping | 150,000 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Total Manufacturing Overhead | 788,500 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Total cost of goods sold | 1,557,750 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Gross Margin | $594,750 | 28% | ||||||||||||||||||||||||||||||||||||||||||||||||||

| General, Selling & Admin. Expense | 559,650 | |||||||||||||||||||||||||||||||||||||||||||||||||||

| Operating Income (pre-tax) | $35,100 | 2% | ||||||||||||||||||||||||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||||||||||||||||||||||||||

| Exhibit 3 Product Data | |||

| Valves | Pumps | Flow Controllers | |

| Materials per unit | |||

| # ofcomponents | 4 | 5 | 10 |

| 3 @ $2 = $6 | 4 @ $2 = $8 | 4 @ $1 = $4 | |

| 2 @ $6 = $12 | 2 @ $7 = $14 | 5 @ $2 = $10 | |

| 1 @ $8 = $8 | |||

| Materials cost per unit | $18.00 | $22.00 | $22.00 |

| Direct labor per unit (in DL hrs) | 0.4 | 0.5 | 0.4 |

| Direct labor $/unit @ $25/DL hr | $10.00 | $12.50 | $10.00 |

| including employeebenefits) | |||

| Machine hours per unit | 0.50 | 0.50 | 0.30 |

| Exhibit 4 MonthlyProduction and Operating Statistics (March 2000) | ||||

| Valves | Pumps | Flow Controllers | Total | |

| Production (units) | 7,500 | 12,500 | 4,000 | 24,000 |

| Machine hours | 3,750 | 6,250 | 1,200 | 11,200 |

| Production runs | 10 | 50 | 100 | 160 |

| Number of shipments | 10 | 70 | 220 | 300 |

| Hours of engineering work | 250 | 375 | 625 | 1,250 |

What is the competitive situation faced by Wilkerson?

Given some apparent problems with Wilkersonâs cost system,should executives abandon overhead assignment to products entirelyby adopting a contribution margin approach in which manufacturingoverhead is treated as a period expense? Why or why not?

Prepare the following calculations. Create a table using Excelto show your answers with details support your answer. Be sure touse $ signs where appropriate. Copy and paste as picture into Worddocument.

Calculate the unit product cost for each product using thedirect-labor-based cost allocation system.

Calculate the unit product cost for each product using activitybased costing to allocate the cost of manufacturing overhead, aswell as profitability for each product line. Overhead cost poolsinclude machine, setup, receiving/scheduling, engineering supportand packing/shipping products.

Compare your work in question 3a. and 3b. above. Why have costshifts occurred?