FINC314 Lecture Notes - Lecture 14: Dimensional Fund Advisors, Efficient Frontier, Downside Risk

10 Feb 2020

School

Department

Course

Professor

Document Summary

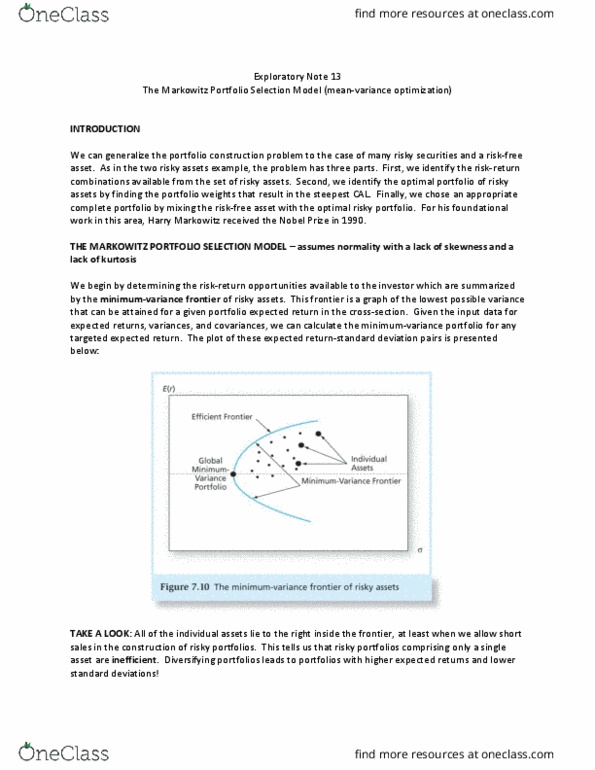

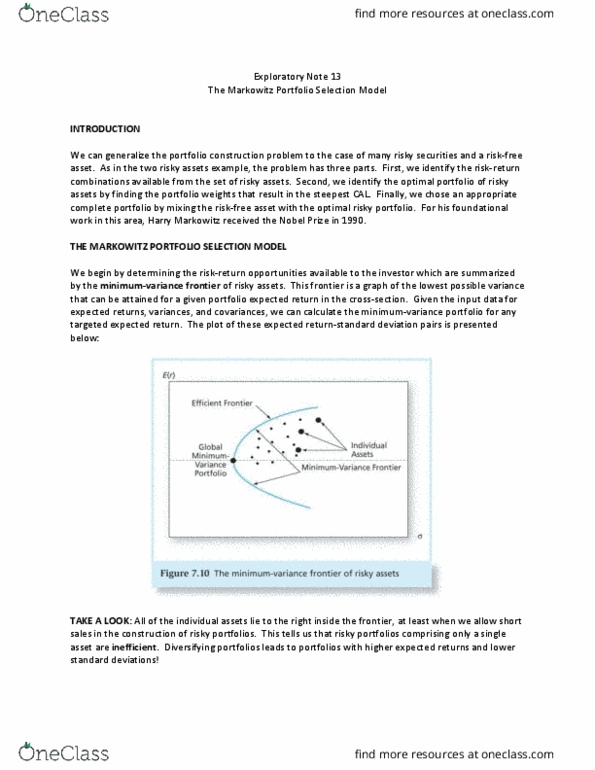

This exploratory note explores james davis" whitepaper, efficient frontiers constructed with historical. Data can be misleading, and also presents a couple of alternatives to the mean-variance formulation of. Dimensional fund advisors are a fund company that run over sh. 5 trillion. Mean-variance efficiency, of course, assumes that investors would like to achieve a given expected return with as little uncertainty about the outcome as possible. Viewed another way, investors would like the highest possible expected return for a given level of return variation. Portfolios that achieve this objective are said to be mean-variance efficient. Consider the following figure (ex ante = from the beginning): Since investors prefer high expected returns and low standard deviations (or variances), they like to go as far northwest as possible in two-dimensional space. The available investments, of course, constrain how far investors can go. An important note: the hypothetical frontier shown above utilizes ex ante expected returns (generated via an asset pricing model).