ACG 2071 Lecture 14: Chapter 12 Notes Part 2

19 Oct 2018

School

Department

Course

Professor

Document Summary

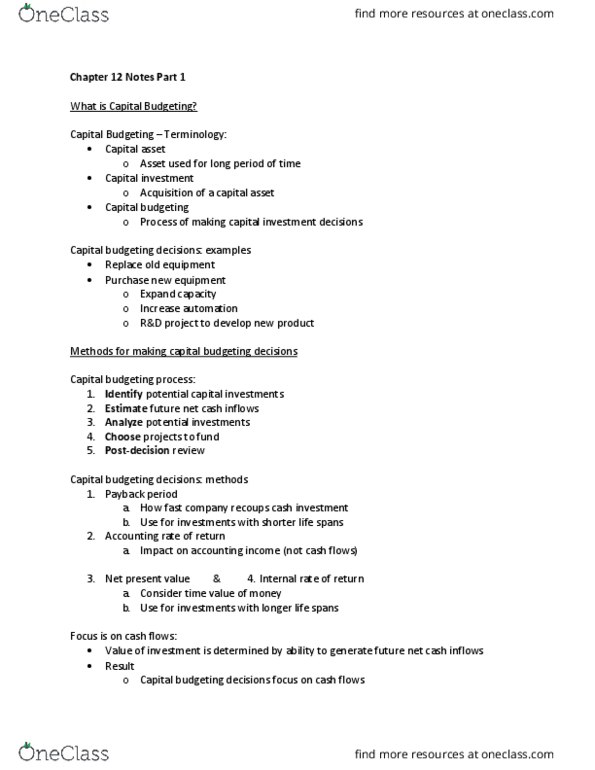

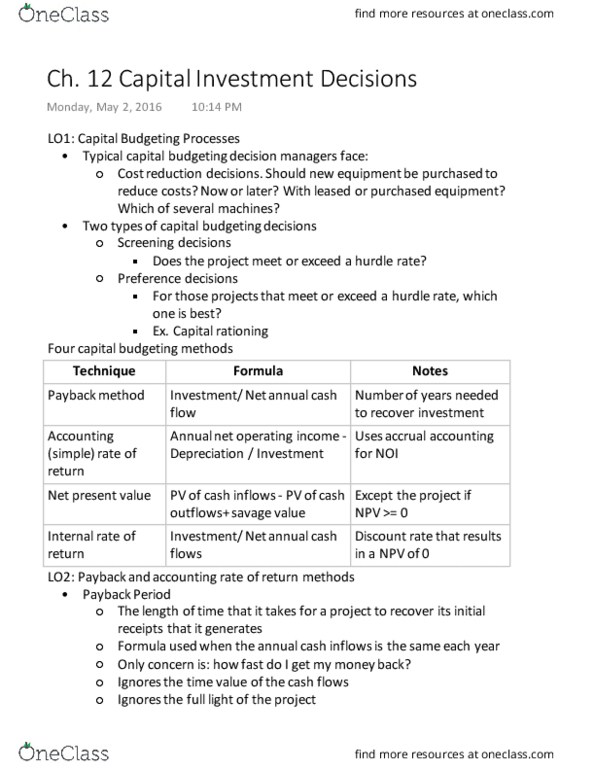

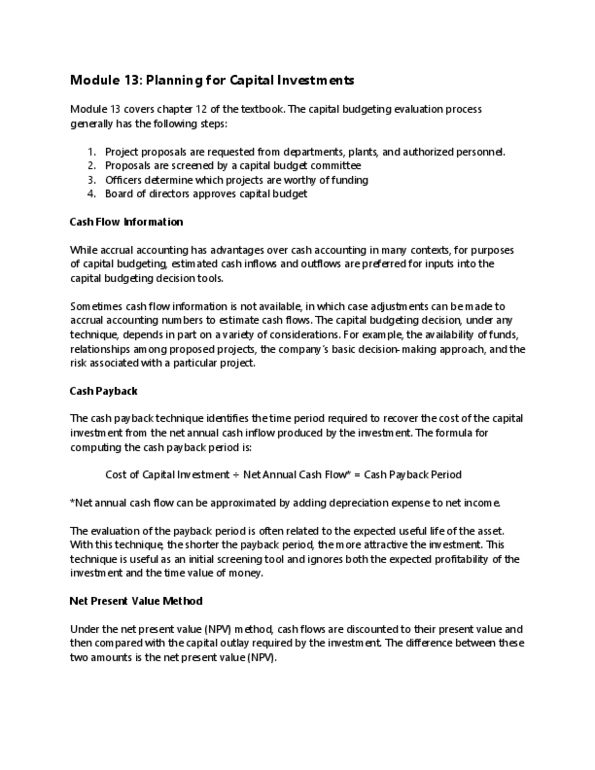

Payback period: pros and cons: advantages, simple, use as initial screening tool, highlights risk of not recouping investment, short cash recovery period versus long cash recovery period, disadvantages, focuses only on payback time, not overall profitability. Ignores: post-payback cash flows, residual value, time value of money. Annual depreciation expense = (initial cost of asset residual value) / useful life of asset (in years) Accounting rate of return: overview: average a(cid:374)(cid:374)ual a(cid:272)(cid:272)ou(cid:374)ti(cid:374)g rate of retur(cid:374) over asset"s life, measures overall profitability of capital investment, unique feature, based on accrual-basis accounting income, not cash flows. Accounting rate of return: decision rule: accounting rate of return equals or exceeds required rate of return. Invest in project: accounting rate of return less than required rate of return, do not invest. Uneven cash flows and residual value: uneven annual net cash inflows, compute and use average annual net cash inflow to compute arr, residual value, reduces depreciation expense.