FIN 4504 Lecture Notes - Lecture 21: Capital Asset Pricing Model, Sharpe Ratio, Municipal Bond

9 Nov 2016

School

Department

Course

Professor

Document Summary

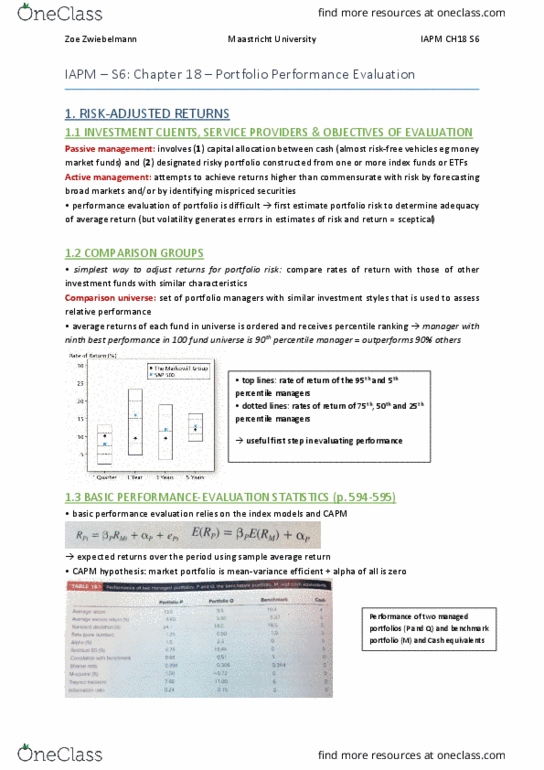

> diversified portfolio with no security mispricing identification. > forecasting broad markets and/or idefntifying mispriced securities to achieve higher. > market timing: move fun between risky portfolio and cash, based on foreasts of. > to measure abnormal performance, we must measure normal performance first. From this the expected return e(rp) can be found. Measures the reward to total risk tradeoff. Measures the reward to systematic risk tradeoff. Measures the average return over and above that predicted by the capm, (i. e. alpha) Measures abnormal return per unit of diversifiable risk. When choosing among portfolios competing for the overall risky portfolio. When ranking many portfolios that will be mixed to form the overall risky portfolio. When evaluating a portfolio to be mixed with the benchmark portfolio. Most popular procedure to measure performance is to compare fund returns with returns on a (cid:271)e(cid:374)(cid:272)h(cid:373)ark i(cid:374)de(cid:454) sele(cid:272)ted (cid:271)ased o(cid:374) fu(cid:374)d"s i(cid:374)vest(cid:373)e(cid:374)t st(cid:455)le. The first step is to establish a benchmark for performance evaluation.