ACCT 2101 Lecture Notes - Lecture 2: Dividend, Accounts Payable, Common Stock

23 Aug 2016

School

Department

Course

Professor

Document Summary

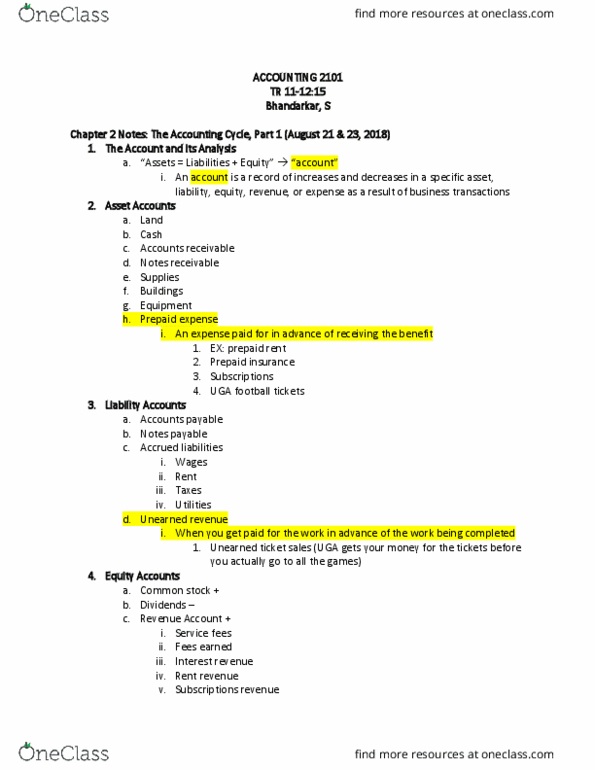

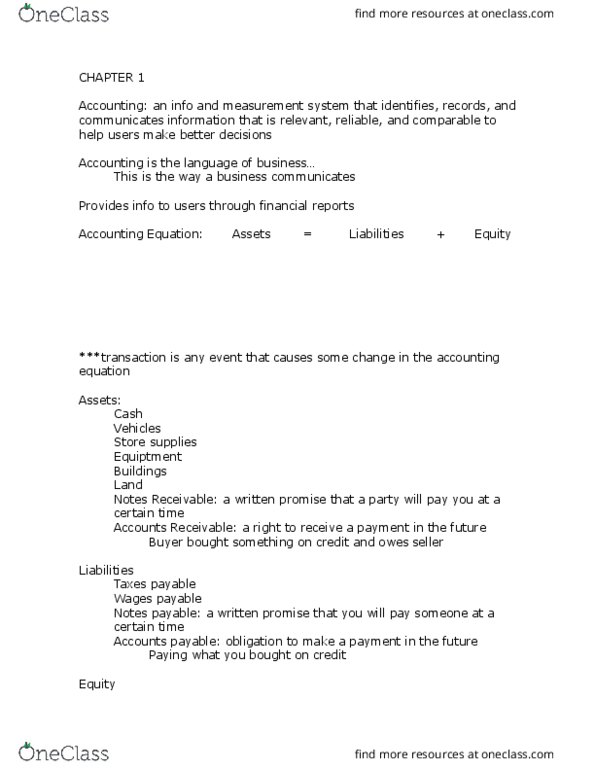

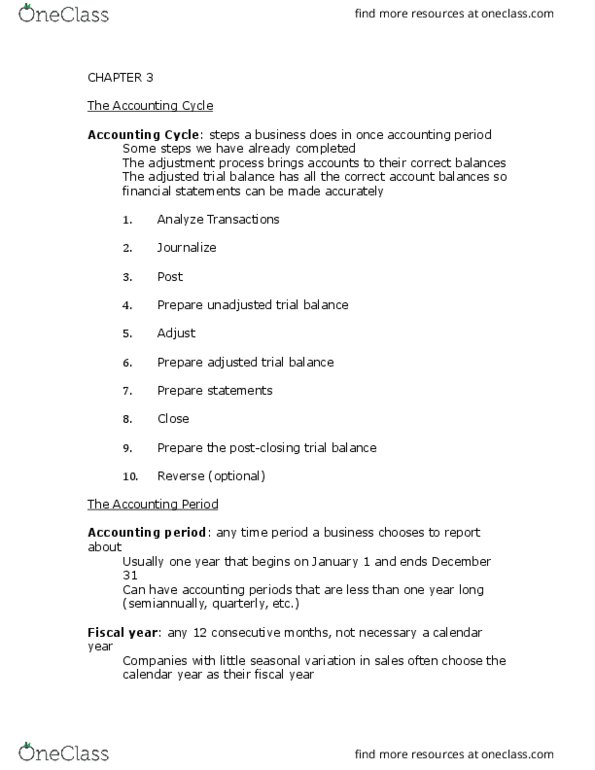

Assets accounts = liability accounts + equity accounts. Asset accounts: cash, land, buildings, equipment, prepaid accounts, accounts receivable, notes receivable, supplies. Liability accounts: notes payable, accounts payable, accrued liabilities, unearned revenue. Equity accounts: common stock, revenues, dividends, expenses, retained earnings. Equity = common stock - dividend +revenue - expenses. Ledger: a complete collection of all accounts for an information system. A company"s size and diversity of operations affect the number of accounts needed. The recording process: analyze each transaction from source documents record relevant transactions and events in the journal post journal information to ledger accounts prepare and analyze trail balance. A t-account represents a ledger account and is a tool used to understand the effects of one or more transactions. Rules of debit and credit: assets = liabilities + equity. Assets: debit = increase / credit = decrease. Liabilities: debit = decrease / credit = increase. Equity: debit = decrease / credit = increase.