ACCT 2101 Lecture Notes - Lecture 8: Balance Sheet, Income Statement

30 Aug 2016

School

Department

Course

Professor

Document Summary

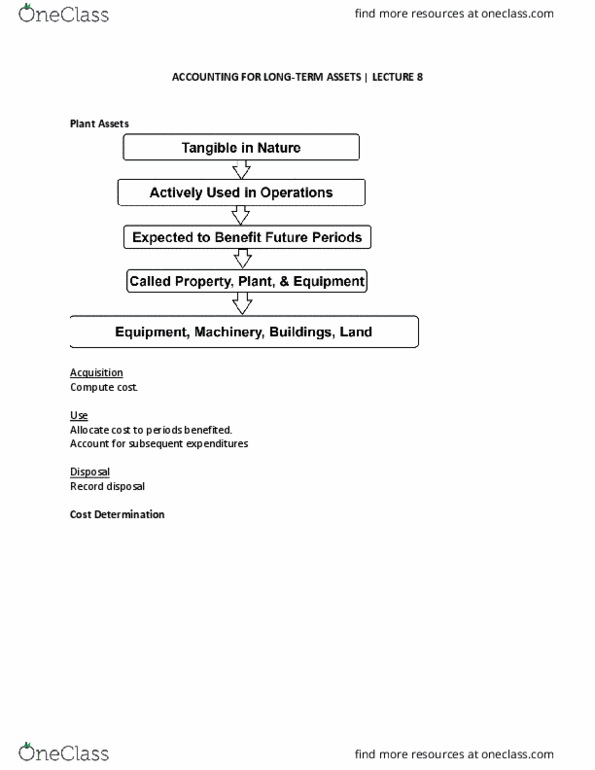

Invoice cost + all necessary expenditures incurred to get asset in place and ready for its intended use - return and cash discounts for early payment. Note: negligence costs and fines are not added to acquisition costs. The total cost of a combined purchase of land and building is separated on the basis of their relative market values. Use: allocation of cost of asset to periods benefited. Depreciation process of allocating the cost of a plant asset to expense in the accounting periods benefiting from its use. Balance sheet: acquisition cost (unused) cost allocation income statement: depreciation expense (used) An adjusting journal entry is prepared at the end of the accounting period to allocate the cost of the asset to the current period. The calculation of depreciation requires three amounts for each asset: Depreciable cost of asset = cost - salvage value. Depreciation expense for period = (cost - salvage value) / useful life.