ACCOUNTG 221 Lecture Notes - Lecture 2: Gross Margin, Net Income, Income Statement

22 Aug 2016

School

Department

Course

Professor

Document Summary

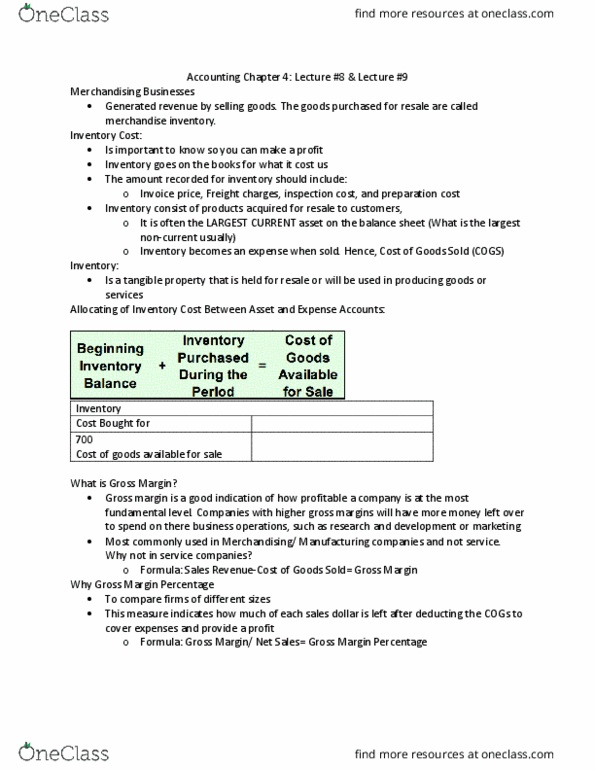

Product costs- (inventory costs) examples; price of goods purchased, shipping and handling costs, transit insurance, and storage costs. Expensed when products are sold; regardless of when they are purchased. Selling and administrative costs- examples; advertising, administrative, salaries, sales commissions, and insurance. Usually recognized as expenses in the period in which they are incurred. Gross margin (gross profit)= net sales cost of goods sold. The selling and administrative expenses are subtracted form the gross margin to get net income. Perpetual inventory system- inventory account is adjusted continually throughout the accounting period. Each time merchandise is purchased the inventory account is increased. Purchase returns and allowances- on financial statements returns and allowances are combined in one entry. Allowances are a reduction of price of a good because the customer is dissatisfied. Purchase discount- when a cash discount is applied to a purchase. Annual rate= discount rate x (365 days / terms of the loan)