ACCOUNTG 321 Lecture Notes - Lecture 3: General Ledger, Deferral, Deferred Income

21 Feb 2017

School

Department

Course

Professor

Document Summary

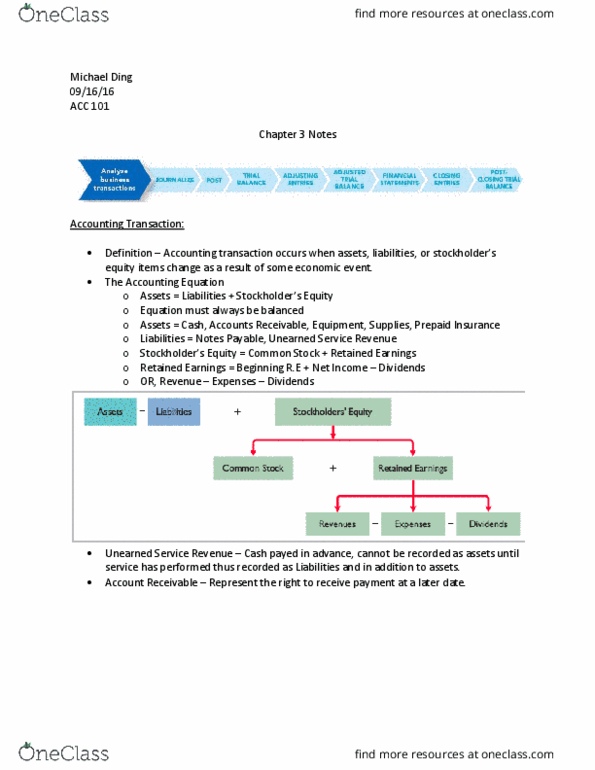

Accounting equation: assets = lia(cid:271)ilities + o(cid:449)(cid:374)e(cid:396)s" e(cid:395)uity, assets = total economic resources, lia(cid:271)ilities + o(cid:449)(cid:374)e(cid:396)s" e(cid:395)uity = total (cid:272)lai(cid:373)s. O(cid:449)(cid:374)e(cid:396)s" e(cid:395)uity paid-in capital (common stock) and. General ledger accounts: serve as control accounts, subsidiary accounts: maintained in separate subsidiary ledgers. Individual account receivable accounts or each of the (cid:272)o(cid:373)pa(cid:374)y"s (cid:272)(cid:396)edit (cid:272)usto(cid:373)e(cid:396)s: classified as: Unadjusted trial balance: list of the general ledger accounts along with their balances, purpose: to check for completeness and prove that the accounting equation is in balance. Total debit balances = total credit balances. Adjusting entries: record the effect of internal events on the accounting equation. Recorded at the end of any period when financial statements are prepared: objective: to implement the accrual accounting model. Prepayments: occur when the cash flow precedes either expense or revenue recognitions. Credit cash, debit prepaid asset account: sometimes referred to as deferrals, prepaid expenses: cost of assets acquired in one period and expensed in a future period.