ECON 002 Lecture Notes - Lecture 15: Adverse Selection, Liquidity Premium, Current Asset

Document Summary

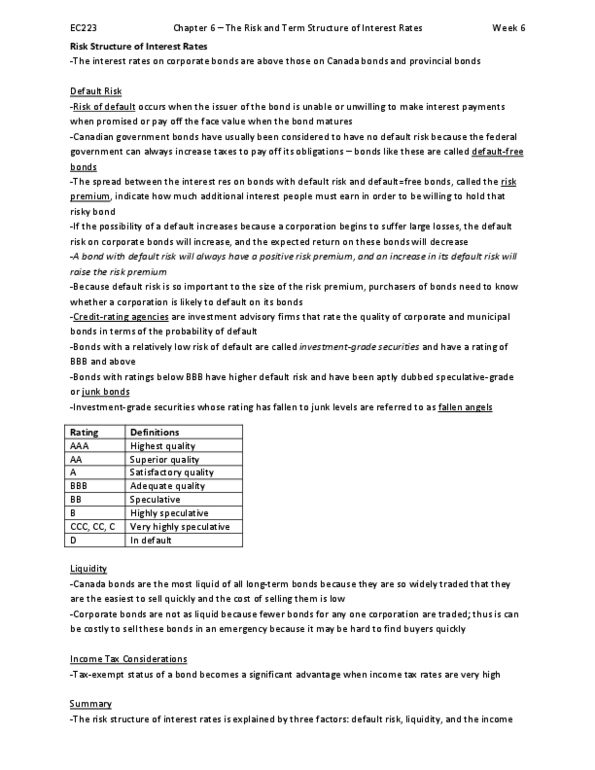

Financial risk is present whenever there is some probability of earning a return on an investment that is less than the amount expected. In general, the greater the probability of a return far below that anticipate d, the greater the risk. In statistical terms, you can think of as variance (a measure of dispersion around the mean). The risk component embeds at least 2 terms: term or liquidity premium: e. g. the spread between the return of long term and short- term bonds. Short term bonds are more liquid (easy to sell) than longer term bonds, so they are less risky. Ii) default or credit risk premium role of credit rating agencies: note that real interest rates can be negative!! Even though a firm wishes to borrow, lenders may not allow the firm to do so. Banks are operating in environments with only partial information and this can lead to market failures. Example: adverse selection and moral hazard in insurance market.