BUS 202 Lecture Notes - Lecture 2: Direct Labor Cost, Management Accounting, Finished Good

Document Summary

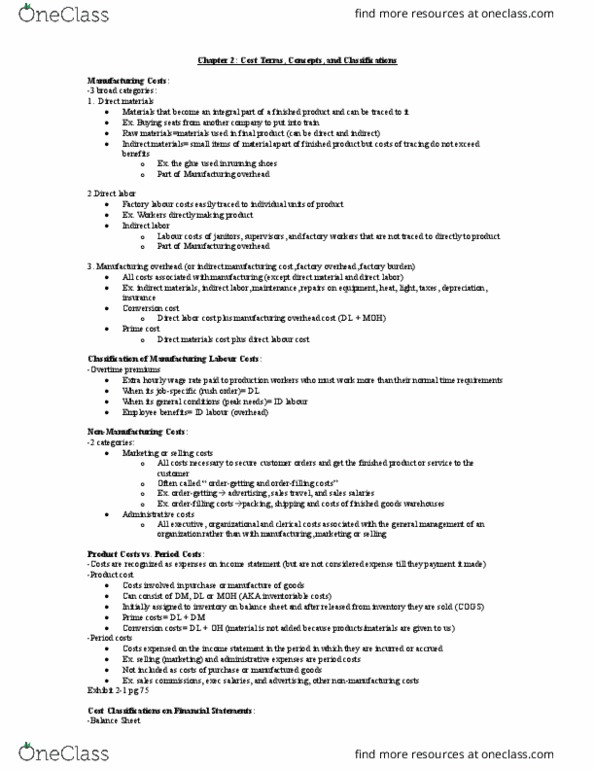

Manufacturing inventories = product cost on sfp/bs reported as current assets. Raw materials inventory: cost of materials on hand such as cloth, plastic, wood, etc. Work in-process inventory: cost (dm, dl, and oh) of partially-completed goods on hand. Finished goods inventory: cost (dm, dl, and oh) of completed goods held for sale on hand. Cost of goods sold: cost (dm, dl, and oh) of finished goods sold and delivered (ownership transferred) Manufacturing cost of goods sold expense on cis. Direct cost: a cost that can be traced to a cost object because a cause-and-effect relationship exists. Traceability: the ability to cost-effectively observe, measure, and assign the effects of specific costs to specific cost objects. Direct manufacturing product costs: costs of production inputs that can be traced and assigned to specific outputs (products) because: Direct mfg costs = dm + dl = prime costs. A shirt manufacturer used 5,000 yards of cloth to complete a production run of 2,000 dress shirts.