ACC 310F Lecture Notes - Lecture 1: Variable Cost

Document Summary

Get access

Related Documents

Related Questions

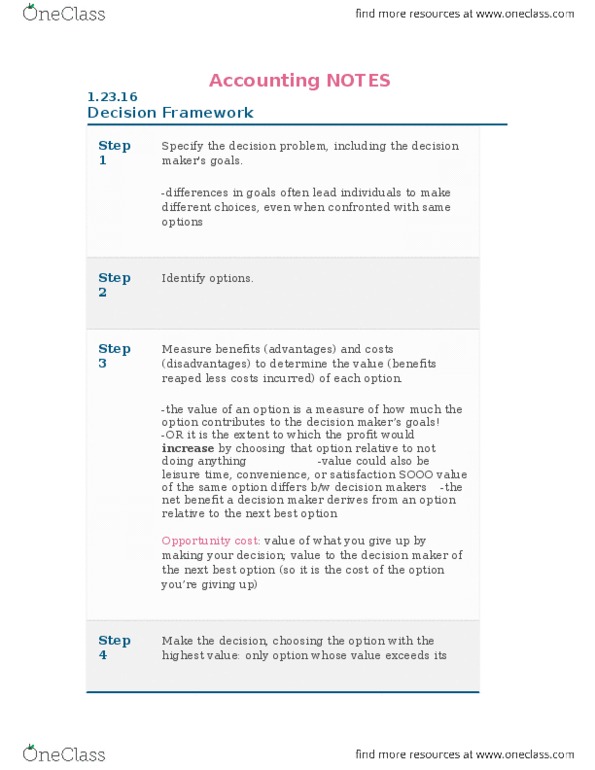

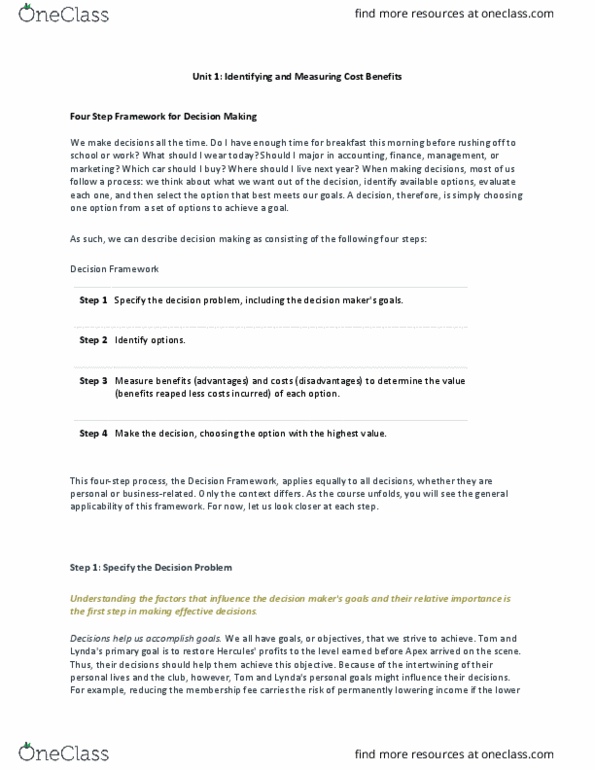

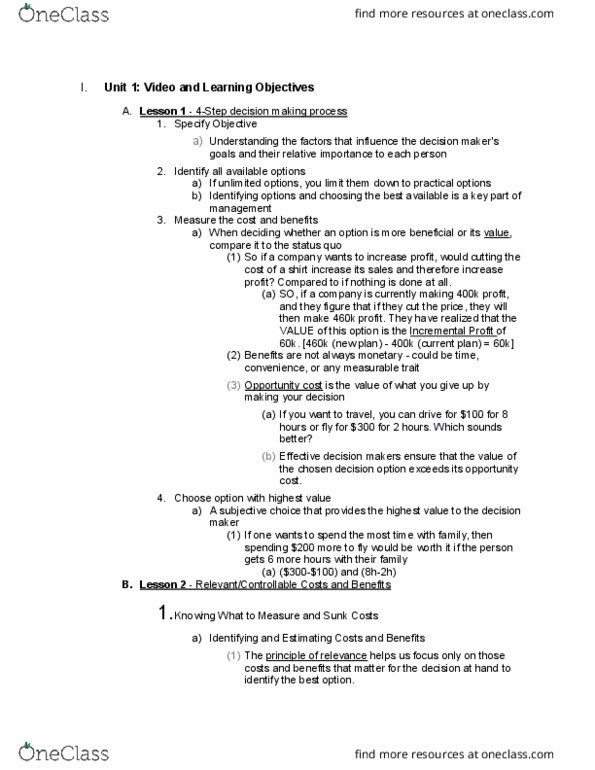

Tactical decision making

Tactical decision making means choosing among alternatives withan immediate or limited end in view. For example, a company mayaccept a special order for less than the normal selling price touse idle capacity. Tactical decisions tend to be short-runin nature; however, it should be emphasized that short-rundecisions often have long-run consequences. A general tacticaldecision-making model is outlined here.

| 1. | Recognize and define theproblem. |

| 2. | Identify possible alternativesolutions to the problem, and eliminate any unfeasiblealternatives. |

| 3. | Identify the costs and benefitsassociated with each feasible alternative. Eliminate the costs andbenefits that are not relevant to the decision. |

| 4. | Compare the relevant costsand benefits for each alternative. |

| 5. | Assess qualitative factors. |

| 6. | Select the alternative with thegreatest overall benefit. |

Identifying and comparing relevant costs and revenues is theheart of the tactical decision model. Relevant costs (revenues) arefuture costs (revenues) that differ across alternatives. (Revenuesare treated in the same way as costs, so we will simplify thediscussion by referring to costs.) All decisions relate to thefuture; so, only future costs can be relevant. In addition, thecost must differ from one alternative to another. If a future costis the same for more than one alternative, it has no effect on thedecision. Such a cost is an irrelevant cost.

Assume that Reeves Company is considering accepting a specialorder for $25 per unit when the normal selling price is $30 perunit. Reeves has enough excess capacity to make the order withoutdisplacing normal sales. The alternatives facing Reeves Company are(Select "Yes" for the statements that are applicable and "No" forthe items that do not apply):

| Accept the special order. | - Select your answer -YesNoItem1 |

| Reject the special order. | - Select your answer -YesNoItem2 |

| Sell normal sales for $25 perunit. | - Select your answer -YesNoItem3 |

Choose which of the following are relevant in deciding whetheror not to accept the special order. (Select "Yes" for thestatements that are applicable and "No" for the items that do notapply)

| $25 price. | - Select your answer -YesNoItem4 |

| $30 normal price. | - Select your answer -YesNoItem5 |

| Variable cost of making the unitsin the special order. | - Select your answer -YesNoItem6 |

| Depreciation on factory equipmentused in making the special order units. | - Select your answer -YesNoItem7 |

| Increased property taxes on thefactory building which are due while the special order would bemade. | - Select your answer -YesNoItem8 |

While cost and revenue information is important, otherinformation may be needed to make an informed decision. Thesenon-financial factors are termed qualitative and are often relevantin decision making. For example, in deciding whether to make acomponent in-house or purchase it from an outside supplier, thecompany may consider any difference in quality or in responsivenessto the company's production schedules.

In my opinion, we ought to stop making our own drums and accept that outside supplierâs offer,â said Wim Niewindt, managing director of Antilles Refining, N.V., of Aruba. âAt a price of $17 per drum, we would be paying $6.85 less than it costs us to manufacture the drums in our own plant. Since we use 50,000 drums a year, that would be an annual cost savings of $342,500.â Antilles Refiningâs current cost to manufacture one drum is given below (based on 50,000 drums per year):

| Direct materials | $ | 10.40 |

| Direct labor | 6.50 | |

| Variable overhead | 1.50 | |

| Fixed overhead ($2.90 general company overhead, $1.65 depreciation, and, $0.90 supervision) | 5.45 | |

| Total cost per drum | $ | 23.85 |

A decision about whether to make or buy the drums is especially important at this time because the equipment being used to make the drums is completely worn out and must be replaced. The choices facing the company are:

Alternative 1: Rent new equipment and continue to make the drums. The equipment would be rented for $135,000 per year.

Alternative 2: Purchase the drums from an outside supplier at $17 per drum.

The new equipment would be more efficient than the equipment that Antilles Refining has been using and, according to the manufacturer, would reduce direct labor and variable overhead costs by 40%. The old equipment has no resale value. Supervision cost ($45,000 per year) and direct materials cost per drum would not be affected by the new equipment. The new equipmentâs capacity would be 125,000 drums per year.

The companyâs total general company overhead would be unaffected by this decision. (Round all intermediate calculations to 2 decimal places.)

Required:

1. To assist the managing director in making a decision, prepare an analysis showing the total cost and the cost per drum for each of the two alternatives given above. Assume that 50,000 drums are needed each year.

a. What will be the total relevant cost of 50,000 drums if they are manufactured internally as compared to being purchased?

b. What would be the per unit cost of each drum manufactured internally? (Round your answer to 2 decimal places.)

c. Which course of action would you recommend to the managing director?

| Purchase from the outside supplier | |

| Manufacture internally | |

| Indifferent between the two alternatives |

2a-1. What will be the total relevant cost of 100,000 drums if they are manufactured internally?

2a-2. What would be the per unit cost of drums?

2 a-3. What course of action would you recommend if 100,000 drums are needed each year?

| Indifferent between the two alternatives | |

| Manufacture internally | |

| Purchase from the outside supplier |

2b-1. What will be the total relevant cost of 125,000 drums if they are manufactured internally?

2b-2. What would be the per unit cost of drums? (Round your answer to 2 decimal places.)

2b-3. What course of action would you recommend if 125,000 drums are needed each year?

| Manufacture internally | |

| Purchase from the outside supplier | |

| Indifferent between the two alternatives |

Case 9-6: Profit PlanningâChoice of CostStructure

The owner of a package delivery business is currently evaluatingthe choice between two different cost structures, based on how thedelivery personnel are paid. One option (hereafter, âAlternative#1â) has relatively higher short-term fixed costs, while the otheroption (hereafter, âAlternative #2â) has the reverseâthat is,relatively higher variable costs in its cost structure. (Forsimplicity in this example we hold the delivery cost per package,that is, the selling price per unit is constant. Selling price isindependent of the cost-structure choice.) The following tablecontains pertinent information for creating the CVP model for eachdecision alternative:

Decision Inputs (Data) | Cost Structure Alternative #1 | Cost Structure Alternative #2 |

Delivery price (i.e., revenue) per package | $60 | $60 |

Variable cost per package delivered | $48 | $30 |

Contribution margin per unit | $12 | $30 |

Fixed costs (per year) | $600,000 | $3,000,000 |

Requirements

1. What is meant by the term âshort-term profit-planningâ model,and how can such a model be used by management? (That is, in whatsense can this model be used to facilitate planning, control, ordecision-making by managers of an organization?)

2. What are the definitions of fixed costs, variable costs,contribution margin ratio, contribution margin per unit, andrelevant range?

3. What is the break-even point, in terms of number ofdeliveries per year (or per month), for Alternative #1? ForAlternative #2?

4. How many deliveries would have to be made under Alternative#1 to generate a pre-tax profit, ÏB, of $25,000per year?

5. How many deliveries (per month or per year) would have to bemade under Alternative #1 to generate a pre-tax profit,ÏB, equal to 15% of sales revenue?

6. How many deliveries would have to be made under Alternative#2 to generate an after-tax profit, ÏA, of$100,0000 per year, assuming a tax rate of, say, 45%?

7. Assume that for the coming year total fixed costs areexpected to increase by 10% for each of the two alternatives. Whatis the new break-even point, in terms of number of deliveries, foreach decision alternative? By what percentage did the break-evenpoint change for each case? How do these figures compare to thepercentage increase in budgeted fixed costs?

8. Assume an average income-tax rate of 40%. What volume (numberof deliveries) would be needed to generate an after-taxprofit, ÏA, of 5% of sales for each alternative?