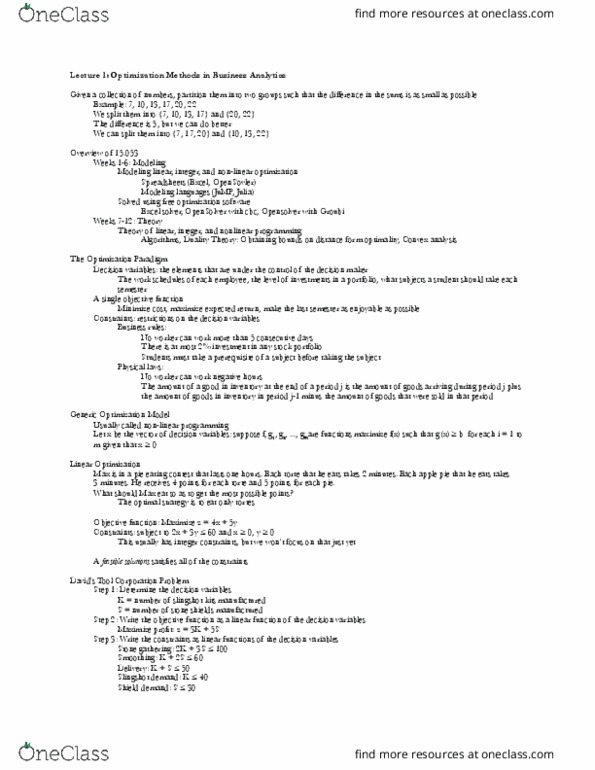

OPRE 3333 Lecture Notes - Lecture 11: Isocost, Sensitivity Analysis, Feasible Region

25 Jun 2018

School

Department

Course

Professor

CH 11 Sensitivity Analysis and Linear Optimization

Optimization problems:

Can be used to support and improve managerial decision making.◦

Maximize or minimize some function, called the objective function, and have a set of restrictions◦

known as constraints.

Can be linear or nonlinear.◦

Application:

A manufacturer wants to develop a production schedule and an inventory policy that will satisfy ◦

demand and minimize costs.

A financial analyst would like to establish an investment portfolio that maximizes the return on ◦

investment.

◦ A marketing manager wants to determine how best to allocate a fixed budget among alternative

media that maximizes advertising effectiveness.

A company had warehouses in a number of locations. Given specific customer demands, the company◦

wants to know how much each warehouse should ship to each customer to minimize costs.

Linear Model Formulation

Decision Variables: The decision variables should completely describe the decisions to be made.

Objective Function : A function of the decision variables upon which the decision maker wants to

maximize or minimize (i.e. optimize), use z to denote OF.

Constraints: there are restrictions that limit how large x1 and x2 can be … these

are called“constraints”

Sign Restrictions Note: Constraints and Sign Restrictions are expressed using the Standard Form of the

linear equation.

(Objective function)

("subject to")

(C1:Finishing constraint)

(C2 :Carpentry constraint)

(C3:Soldier demand constraint)

(Sign constraint)

(Sign constraint)

Optimal Solution:

For a maximization problem, an optimal solution to an LP is a point in the feasible region with the largest

objective function value

for a minimization problem, an optimal solution is a point in the feasible region with the smallest

objective function

The Intersection Point of Two Constraints

Step 1: Rewrite constraints as equalities.

Step 2: Choose a decision variable.

Step 3: Multiply constraints by appropriate constants so that the coefficients of the chosen decision

variable is the same in each equation.

Step 4: Subtract one constraint from the other.

Step 5: Solve for the other decision variable.

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Can be used to support and improve managerial decision making. Maximize or minimize some function, called the objective function, and have a set of restrictions. A manufacturer wants to develop a production schedule and an inventory policy that will satisfy demand and minimize costs. A financial analyst would like to establish an investment portfolio that maximizes the return on investment: a marketing manager wants to determine how best to allocate a fixed budget among alternative media that maximizes advertising effectiveness. A company had warehouses in a number of locations. Given specific customer demands, the company wants to know how much each warehouse should ship to each customer to minimize costs. Decision variables: the decision variables should completely describe the decisions to be made. Objective function : a function of the decision variables upon which the decision maker wants to maximize or minimize (i. e. optimize), use z to denote of.