ECON 2304 Lecture Notes - Lecture 3: Economic Surplus, Economic Equilibrium, Efficient-Market Hypothesis

Document Summary

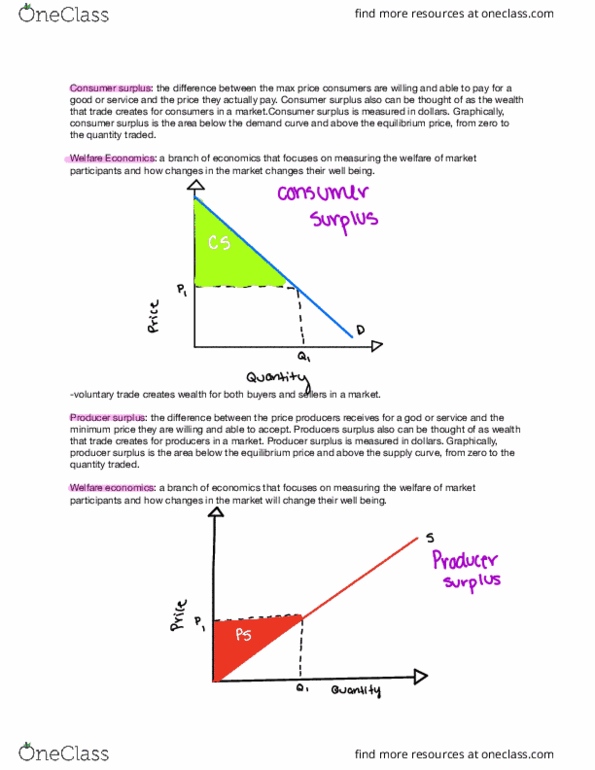

The difference between the maximum price consumers are willing and able to pay for a good or service and the price they actually pay. Can be thought of as the wealth that trade creates for consumers in a market. Everything below the demand curve and above the price: producer surplus. The difference between the price producers receive for a good or service and the minimum price they are willing and able to accept. The area below the equilibrium price and above the supply curve, form zero to the quantity traded: economic surplus. The sum of the consumer and producer. Measuring how much both sides are gaining, or the total benefits toward the producers and consumers. Also known as social welfare or total surplus. Productive efficiency: producing output at the lowest possible average total cost of production. Using the fewest resources possible to produce a good or service.