ECON 2160 Lecture Notes - Lecture 5: Adverse Selection, Risk Premium, Risk Neutral

2 May 2018

School

Department

Course

Professor

“a

Adverse

selection

-

The

Lemon

Problem

One

of

the

big

suppositions

In

the

theory

on

perfectly

competitive

markets

and

our

work

with

game

theory

to

this

point

is

that

all

the

participants

have

complete

and

equal

information

regarding

the

transaction.

When

players

have

a5ymmetric

information,

this

can

lead

to

a

market

or

game

resulting

suffering

from

adverse

selection.

Asymmetric

information

can

be

any

information

inequality

between

parties.

it

does

not

always

have

to

be

one

knows

something

and

the

other

doesn't.

It

can

also

be

the

situation

where

one

knows

more

than

the

other

or

where

there

is

common

knowledge

between

the

players

and

private

Information

as

well.

You

can

visualize

the

Information

set

as

a

Venn

Diagram.

Any

situation

where

the

circles

for

two

players

are

not

exactly

on

top

of

each

other

(concentric

with

equal

radii),

there

is

Information

asymmetry.

Asymmetric

Information

most

often

leads

to

the

market

failure

named

Adverse

Selection.

The

term,

Adverse

Selection,

comes

from

the

insurance

Industry

and

is

one

of

the

biggest

challenges

in

insurance

underwriting.

If

the

people

you

are

trying

to

insure

have

an

incentive

(lower

premium)

to

either

lie

or

hide

information,

then

the

Insurer

can

miss

assign

the

risk

premium

needed

to

properly

insure

those

people.

As

a

result,

if

the

Insurer

wants

to

stay

in

business

in

the

long

run,

it

must

charge

a

premium

where

It

assumes

some

of

the

information

it

is

getting

on

coverage

risk

is

wrong.

Thus,

it

has

to

charge

a

premium

that

is

higher

than

the

truthful,

low-risk

people

would

want

to

pay.

Hence,

all

the

insurer

gets

are

those

people

with

high

risk

to

buy

the

policy.

However,

those

who

may

believe

they

are

truly

low

risk

may

be

high

risk

or

become

high

risk.

Therefore,

an

efficient

insurance

market

where

everyone

to

be

covered

has

some

probability

of

being

very

risk

needs

to

have

everyone

be

able

to

buy

the

policy.

We

can

see

this

play

out

in

health

insurance.

Some

may

be

easily

categorized

as

high

risk

due

to

past

issues

or

simple

test

and

observations,

while

others

may

appear

to

below

risk

are,

in

fact,

high

risk

(e.g.

hidden

genetic

disease)

or

become

high

risk

(e.g.

traffic

accident).

A

classic

model

looking

into

this

circumstance

is

called

the

Lemon

Model

(Akerlof,

1970).

The

situation

is

there

are

two

types

of

used

cars.

Good

ones:

Oranges

and

Bad

ones:

Lemons

Sellers

of

Oranges

will

sell

at

$12,500

and

up.

Sellers

of

Lemon’s

will

sell

for

at

least

$3000.

The

maximum

buyers

are

willing

to

pay

for

an

Orange

is

$16,000

and

the

maximum

for

3

Lemon

is

$6,000.

In

the

market,

regardless

of

whether

the

car

is

an

Orange

or

a

Lemon,

it

will

have

the

same

price.

To

help

the

model

come

to

specific

results,

without

losing

its

applicability,

we

assume

there

are

enough

buyers

in

the

market,

compared

to

cars

available,

where

the

price

will

be

bid

up

to

the

buyer’s

maximum

wiliness

to

day.

This

assumption

removes

any

uncertainty

about

the

price

paid

and

whether

the

market

will

clear.

It

is

possible

to

relax

this

assumption.

Doing

so

doesn’t

shed

more

light

on

the

basic

concept,

but

the

math

does

get

messier.

Our

numbers

in

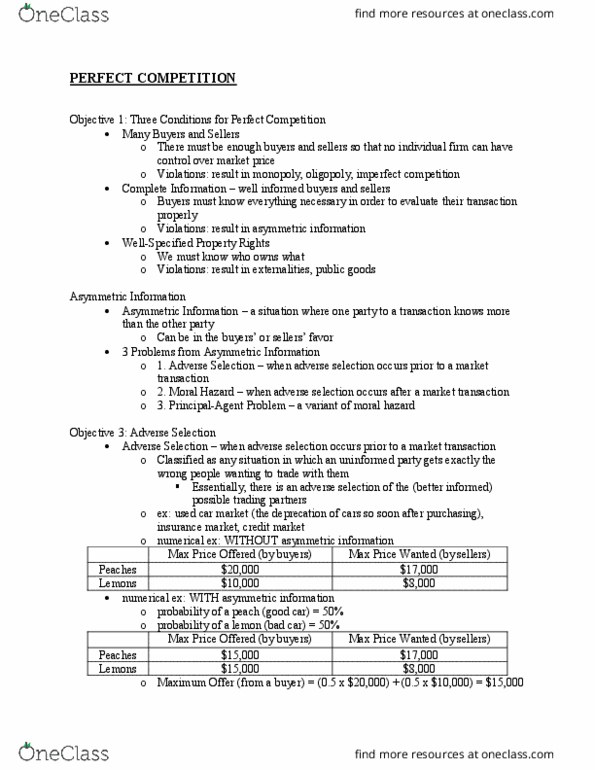

table.

tam—.-

sewerswnme

ear-.m-

As

we

can

see,

any

otter

irom

a

Buyer

below

$12,500

will

guarantee

the

car

is

a

Lemon,

as

Orange

sellers

will

not

put

their

car

up

lor

sale

at

that

prrc‘e.

However,

an

oller

above

$12,500

does

not

guarantee

that

the

car

offered

for

sale

is

an

Orange.

There

is

just

the

possibility

that

it

is

one.

As

this

is

the

case,

the

Buyer

then

needs

to

think

of

their

expected

value

or

the

car

they

purchased.

An

important

concept

is

the

level

of

risk

a

buyer,

in

this

case,

is

willing

to

assume.

To

help

ease

the

model,

we

are

going

to

say

our

buyers

are

"risk

neutral."

Risk

neutrality

simple

means

as

long

as

the

value

or

expected

value

received

is

greater

than

Its

cost,

the

transaction

takes

placemp'ly

put,

lfthere

l

thbflu'm,

the

rlslt

neutral

agent

does

thinlvltyfihere

is

no

compensation

for

the

risk

taken.

it

is

possible

to

include

risk

aversion

in

to

models.

However,

it

doesn’t

add

much

more

to

our

understanding

of

the

underlying

concept

at

this

point.

Would

there

be

a

used

car

market,

including

both

types

of

cars,

if

there

are

3

Oranges

for

every

2

Lemons

for

sale,

or

the

used

car

supply

is

60%

Oranges?

What

would

be

a

car

buyers

expected

value

of

any

randomly

drawn

car?

"but,"

:2

Probablity

of

Orange

*

Value

of

Orange

+

Probablity

of

Lemon

1:

Value

of

Lemon

For

our

numbers,

we

get

EVbuyer

=

.6(16,000)

+

.4(6,000)

=

12,000

The

risk

neutral

car

buyer

will

offer

a

seller

no

more

than

her

expected

value

of

the

car.~"|n

this

case,

the

offer

of

$12,000

isn’t

enough

to

have

an

Orange

be

sold.

Therefore.

only

lemons

will

be

for

offer

-

there

a

is

no

market

with

both

types

of

cars

for

sale

at

this

proportion

of

Oranges

to

Lemons.

How

do

we

find

the

’cut

off

point’

or

the

minimum

proportion

of

Oranges

available

to

have

a

functioning

market?

If

we

say

the

probability

of

an

Orange

is

"f",

then

the

probability

of

a

Lemon

is

(1-f).

We

would

rewrlt'e

our

buyer's

expected

value

as

Eme,

=

f(16,000)

+

(1-f)(6,000)

=

10,000f

-

6000

As

the

Expected

value

of

any

random

car

needs

to

be

more

than

12,500

to

guarantee

there

being

Oranges

for

sale

EVbuyer

—>

orangereservation

price

10,000f

—

6000

_>

12500

10,000f

>._

6500

[2.65

in

order

tor

the

martet

to

function.

there

need

to

be

at

least

a

65%

chance

at

any

randomly drawn

car

tor

sale

being'

an

Orange,

We

can

then

use

our

simple

model

to

see

what

happens

when

we

have

changes

to

demand

for

Orange

can,

An

increase

in

demand

lor

Oranges

would

rais'e

the

maximum

willingness

to

pay

of

them

-

let’s

say

to

180m.

f(i8.000)+

(1

—

[)(6.000)

2

12500

12,000;

2

6500

f

z

.54

Now

that

may

seem

a

little

counterinturt‘ive.

The

demand

for

good

cars

increasing

actually

means

the

number

of

good

cars

for

sale

can

decrease

and

the

market

still

functions.

Why

do

you

think

this

is?

What

happens

if

the

sellers

feel

their

Oranges

are

more

valuable?

Now

they

require

14,500

to

sell.

We

will

go

back

to

the

original

values

for

buyers.

[(16,000)

+

(1

—

f)(6,000)

2

14500

10,000f

—

6000

>_

14500

f

>_.

.85

The

increase

in

value

from

the

sellers

perspective

increases

the

number

of

good

cars

needed

to

make

the

market

function.

Why

do

you

think

this

is

the

case?

Now,

to

be

good

economists,

we

would

be

reticent

to

do

both

changes

in

the

same

model

as

we

cannot

fully

ascribe

causality,

but,

let’s

do

it

anyway.

f(18,000)

+

(1

—

f)(6,000)

>_

14500

12,000f

>_

8500

f

>_

.71

Now

we

may

have

assumed

the

two

factors

would

have

canceled

each

other

out,

but

we

see

the

increase

in

the

price

from

the

sellers

point

of

view

is

more

impactful

than

that

of

the

buyer’s

increase

in

demand.

Thus,

we

see

more

good

cars

on

the

market.

We

can

see

what

price

the

sellers

can

ask

for

if

they

see

the

increase

of

demand,

when

they

have

65%

of

the

cars

on

the

lot

being

Oranges.

.65(18,000)

+

(.

35)(6,000)

=

X

13,800

=

X

This

is

that

we

would

expect.

An

increase

in

demand

would

increase

the

price

of

the

item,

given

a

constant

supply.

And

this

makes

more

sense

as

it

would

be

easier

for

sellers

to

change

the

price

of

a

car

than

to

change

the

proportion

of

cars

on

their

lot.

Document Summary

One of the big suppositions in the theory on perfectly competitive markets and our work with game theory to this point is that all the participants have complete and equal information regarding the transaction. When players have a5ymmetric information, this can lead to a market or game resulting suffering from adverse selection. Asymmetric information can be any information inequality between parties. it does not always have to be one knows something and the other doesn"t. It can also be the situation where one knows more than the other or where there is common knowledge between the players and private. You can visualize the information set as a venn diagram. Any situation where the circles for two players are not exactly on top of each other (concentric with equal radii), there is. Asymmetric information most often leads to the market failure named adverse selection. Adverse selection, comes from the insurance industry and is one of the biggest challenges in insurance underwriting.