ACCT 305 Lecture Notes - Lecture 23: Cash Flow, Net Income, Income Statement

Document Summary

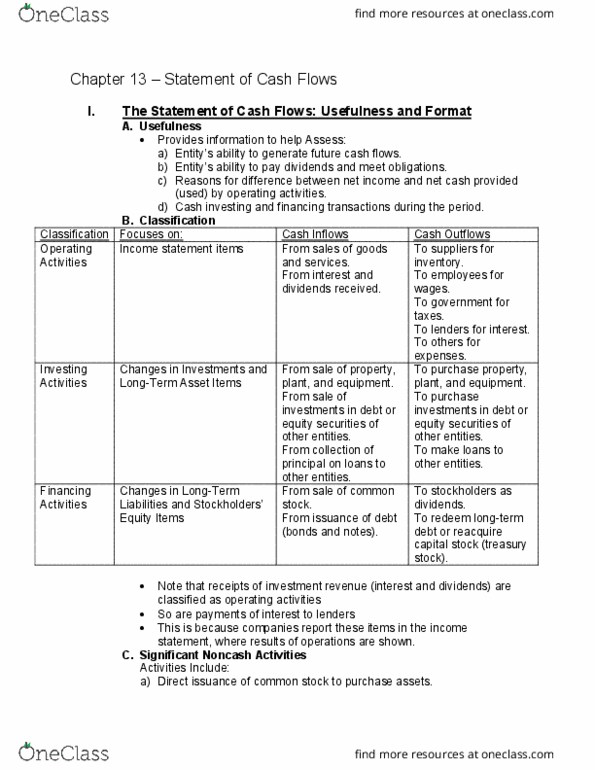

Primary purpose: to provide information about a company"s cash receipts and cash payment during a period. Secondary objective: to provide cash-basis information about the company"s operating, investing, and financing activities. Classification of cash flows: operating activities -> income statement transactions, cash inflows: From returns on loans (interest) and on equity securities (dividends: cash outflows: To others for expenses: investing activities -> changes in investments and long-term asset items, cash inflows: From sale of debt or equity securities of other entities. From collection of principle on loans to other entities: cash outflows: To purchase debt or equity securities of other entities. To make loans to other entities: financing activities -> changes in long-term liabilities & stockholders" equity, cash inflows: From issuance of debt (bonds and notes: cash outflows: To redeem long-term debt or reacquire capital stock. **generally, only investments with original maturities of three months or less qualify under this definition.