FIN 3104 Lecture Notes - Lecture 7: Capital Asset Pricing Model, Risk-Free Interest Rate, Systematic Risk

5 Apr 2020

School

Department

Course

Professor

Document Summary

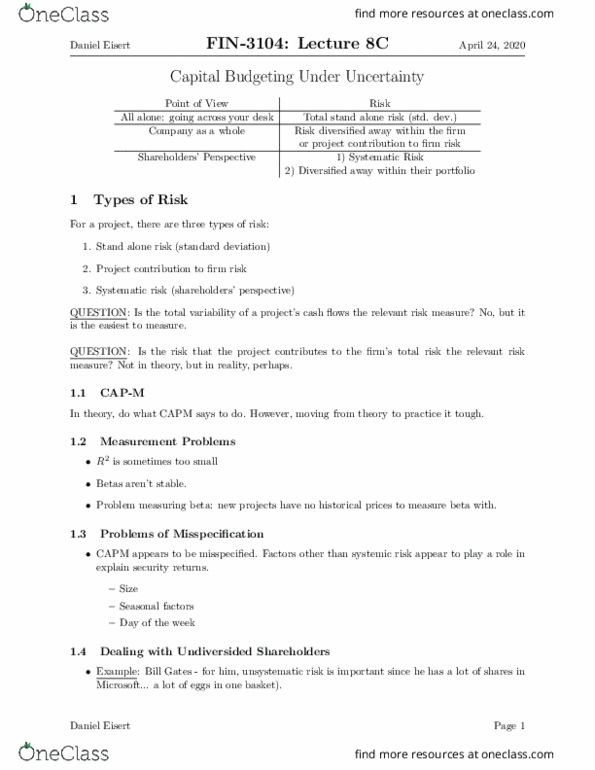

Class business: look for wall street journal readings on canvas. Complete a 1-2 page summary for the group of articles. Recall that systematic risk is the risk that cannot be diversi ed away. It a ects all securities: to measure systematic risk, we measure the tendency of a stock"s movement relative to the market. The average beta for a stock is 1. 00. Beta > 1 ampli es movements in the market. Beta < 1 mutes movements in the market. Since the beta of a portfolio is the weighted average of the individual securities betas, the security"s beta coe cient determines how that stock a ects the riskiness of a diversi ed portfolio. Exam question: calculate the weighted average of betas. Main assumptions: investors are rational, no bankruptcy costs. The cap-m provides use with the theoretically correct required rate of return on asset i, ki.