MGT 210 Lecture Notes - Lecture 10: Current Asset, Financial Statement, Sales Tax

Document Summary

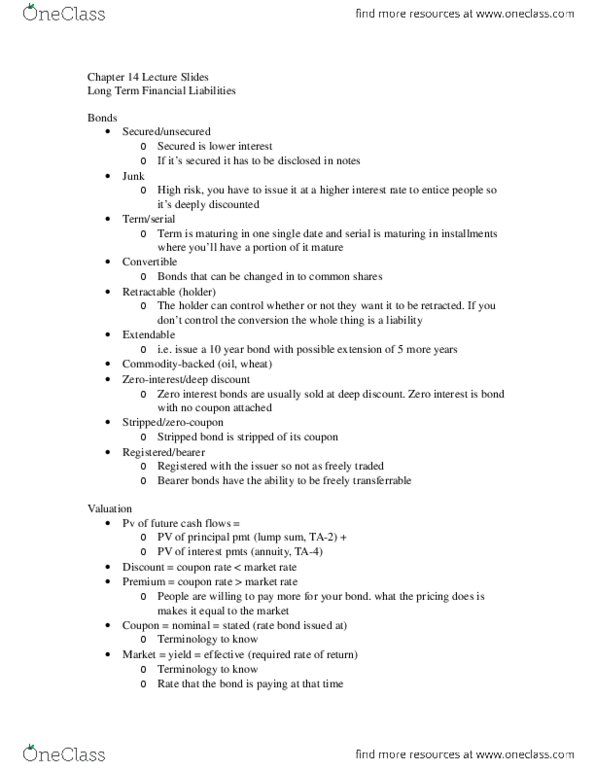

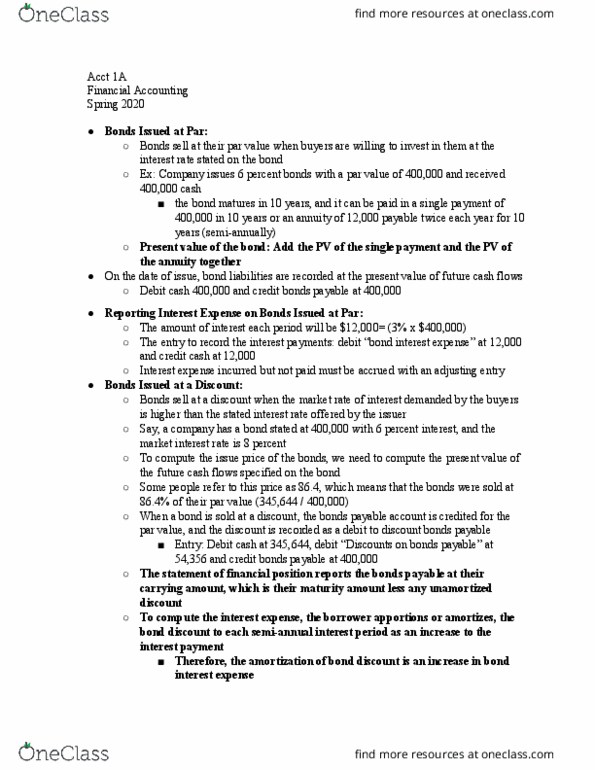

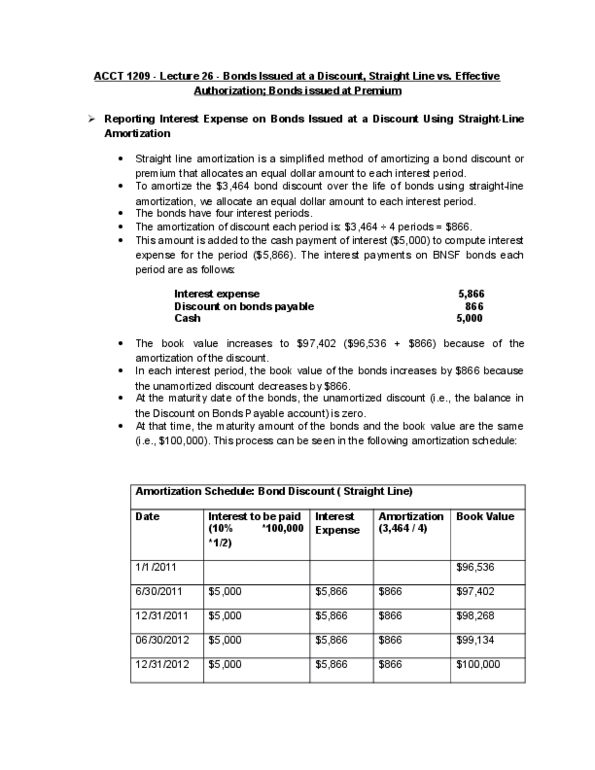

We issue a bond (borrower): we have to pay it back to someone other than a bank. Interest payment- only 1x a year = bonds interest rate x face of bond. Face: use to compute interest payment, amount paid back at maturity, a(cid:373)ou(cid:374)t re(cid:272)orded i(cid:374) a(cid:272)(cid:272)ou(cid:374)t (cid:862)bo(cid:374)d paya(cid:271)le(cid:863) Term- how long it lasts- tells us the date the bond matures. Date issued: debit cash for price of bond, credit bond payable for face of bond. Not the same: have a discount (debit) or premium (credit) Discount is a contra, premium is an adjunct. Debit interest expense, credit cash either debit premium or credit discount to get rid of. Must adjust at 12/31 debit interest expense (cr. On january 1 pay the payable: debit interest payable, credit cash. Bonds payable 350,000 the accrual of interest on december 31, 2014. 12/31 interest expense 28000 (cid:862)carry value(cid:863) of the (cid:271)o(cid:374)d- how much do you owe still.