MGT 210 Lecture Notes - Lecture 12: Deferral, Treasury Stock, Cash Flow

Document Summary

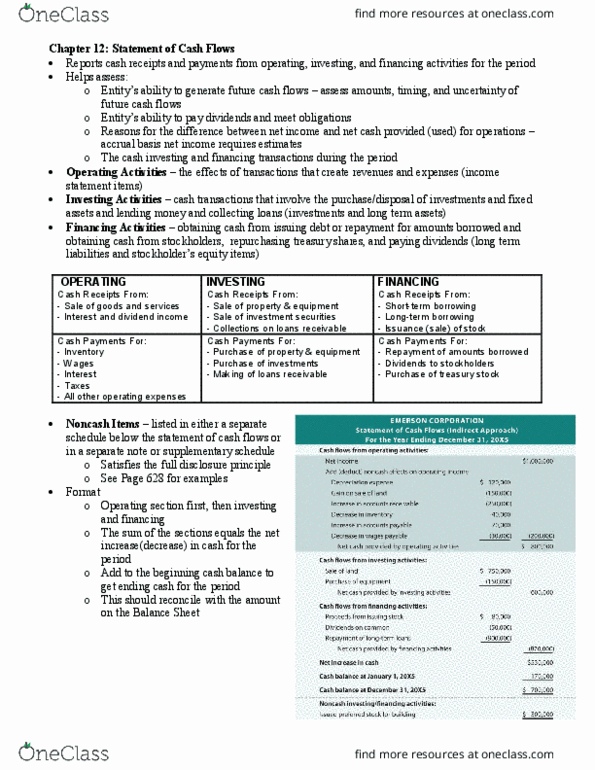

Statement of cash flows- reports cash receipts and cash payments from operating, investing, and financing activities during a period. Can determine future ability to generate cash flow, ability to pay dividends and meet obligations, and the reason for the difference between net income and net cash, and the investing and financing transactions of the period. Operating activities- cash effects on transactions that create revenues and expenses (net income); current assets and current liabilities. Investing activities- cash transactions that involve cash related to investments, ppe, and intangibles (long term assets) Financing activities- long term liability- issuing debt and repaying amounts borrowed; equity that isn"t income- getting $ from stockholders, repurchasing shares, and paying dividends. Issue 100,000 shares of par value common stock for ,000 cash- financing (contributions) Borrowed ,000 from castle bank, signing a 5-year note bearing 8% interest- financing (ltl) Purchased 2 semi-trailer trucks for ,000 cash- investing (ppe) Paid employees ,000 for salaries and wages- operating (expense)