Economics ECON E - 1600 Lecture 1:

7 Sep 2021

School

Department

Course

Professor

Document Summary

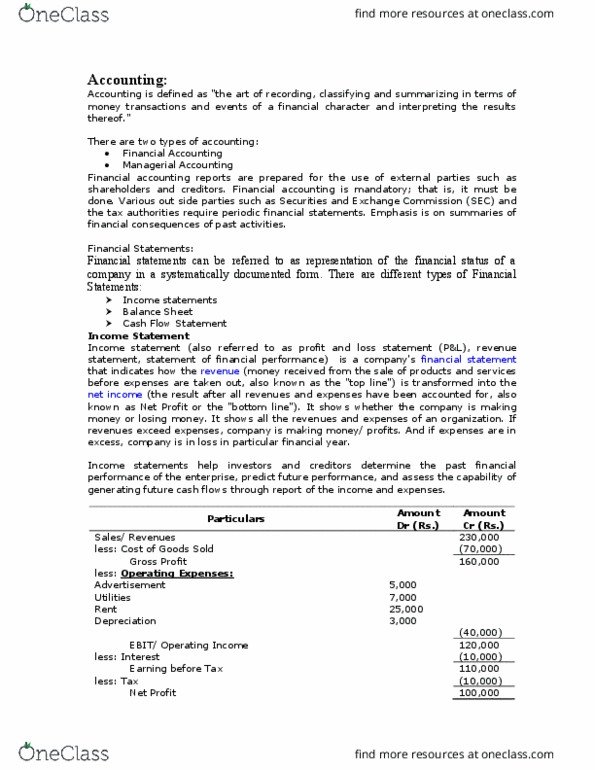

Accounting is defined as "the art of recording, classifying and summarizing in terms of money transactions and events of a financial character and interpreting the results thereof. " There are two types of accounting: financial accounting, managerial accounting. Financial accounting reports are prepared for the use of external parties such as shareholders and creditors. Financial accounting is mandatory; that is, it must be done. Various out side parties such as securities and exchange commission (sec) and the tax authorities require periodic financial statements. Emphasis is on summaries of financial consequences of past activities. Financial statements can be referred to as representation of the financial status of a company in a systematically documented form. It shows whether the company is making money or losing money. It shows all the revenues and expenses of an organization. If revenues exceed expenses, company is making money/ profits. And if expenses are in excess, company is in loss in particular financial year.