25 Bowling R Us Ltd. leases the building in which it operates its bowling alleys. Bowling revenues for the year just ended were $27,000. The lease agreement calls for an annual rental fee equal to 10% of the annual bowling revenues, with $200 payable on the 1st day of each month. If all required monthly payments for the year were made and debited to the rent expense account, the adjusting journal entry at year-end would be? a. Debit rent expense $300 Credit rent payable $300 b. Debit rent payable $300 Credit rent expense $300 Debit rent expense $240 Credit rent payable $240 d. Debit rent payable $240 Credit rent expense $240 e. None of the above The correct answer is 'a'

Related questions

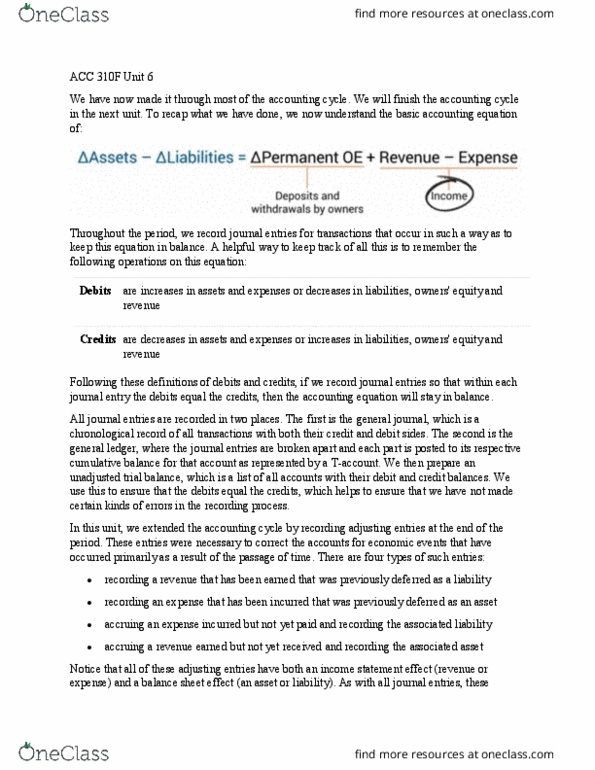

The following adjustments need to be made before the financialstatements can be prepared at the end of the year.

Task 1: Enter the necessary journal entries into the templateprovided and provide the journal entry for each.

December Interest on a bank loan is due on January 2nd of thefollowing year: accrue $1,000.

A contractor (outside services) has finished work on December 31st,but the invoice will not be received until January 7th of thefollowing year: accrue $750. A rent payment was made on December1st for three months from December 1st to February 28th of thefollowing year (6,000 in total). Record the transactionproperly.

The companyâs part-time employees worked a total of 50 hours inDecember, but will get paid only by January 5th. The hourly rate is$15.

The company must record the payment of its annual insurance premiumfor next year. The annual premium is $1,200, an adjustment isnecessary to prepaid insurance.

Task 2: Provide the adjusted trial balance (combine exercises2.1 and 2.2 to show the adjusted trial balance).

| 1 | Interest Expense | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Interest Payable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record December interest expense to bepaid in January | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 2 | Expense for Outside Services | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Accounts Payable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record liability towardscontractor | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 3 | Rental Expenses | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Prepaid Rent | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record the appropiate rental expensefor the month | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 4 | Wage Expense | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Wages Payable | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record liability towards employees | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| 5 | Prepaid Insurance | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Cash | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| To record insurance payment for thefollowing year | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $0 | $0 | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Question 16

Corresponds to CLO 3(d) Hemmingway Corporation paid salaries of$5,000 and advertising expense of $2,000. Which of the followingjournal entries correctly records these expenses?

Debit: Cash $7,000 | ||

Debit: Salaries/Wages Expense$5,000 | ||

Debit: Salaries/Wages Expense$5,000 | ||

Debit: Salaries/Wages Expense$5,000 |

3 points

Question 17

Corresponds to CLO 4(a) Which of the following statements iscorrect regarding accrued revenues and unearned revenues, beforeadjusting entries have been made?

Accrued revenues have not been earned and unearned revenues havebeen earned. | ||

Accrued revenues have been paid and unearned revenues havenot. | ||

Accrued revenues have not been recorded and unearned revenueshave been recorded. | ||

Accrued revenues have been recorded and unearned revenues havebeen recorded. |

3 points

Question 18

Corresponds to CLO 4(b) Hudson Law Corporation received $5,500cash for legal services to be rendered in the future. The fullamount was credited to the liability account Unearned ServiceRevenue. At the end of the period, Hudson determines that $3,000 ofthe legal services have been rendered. The appropriate adjustingjournal entry to be made at the end of the period is:

debit Unearned Service Revenue, $3,000; credit Cash, $3,000. | ||

debit Unearned Service Revenue, $3,000; credit Service Revenue,$3,000. | ||

debit Unearned Service Revenue, $2,500; credit Service Revenue,$2,500. | ||

debit Service Revenue, $2,500; credit Unearned Service Revenue,$2,500. |

3 points

Question 19

Corresponds to CLO 4(c) Ace Corporation purchased officesupplies costing $13,000 and debited Office Supplies for the fullamount. At the end of the accounting period, a physical count ofoffice supplies revealed $2,700 still on hand. The appropriateadjusting journal entry to be made at the end of the period is:

debit Office Supplies Expense, $10,300; credit Office Supplies,$10,300. | ||

debit Office Supplies, $10,300; credit Office Supplies Expense,$10,300. | ||

debit Office Supplies Expense, $2,700; credit Office Supplies,$2,700. | ||

debit Office Supplies, $2,700; credit Office Supplies Expense,$2,700. |

3 points

Question 20

Corresponds to CLO 4(d) On September 1, Northgate paid $18,000to Evans Management Company for 12 months of rent beginning onSeptember 1. The appropriate journal entry was made to record thistransaction. If financial statements are prepared for the 9 monthsended September 30, the adjusting entry to be made by Northgateis:

debit Rent Expense, $13,500; credit Prepaid Rent, $13,500. | ||

debit Prepaid Rent, $1,500; credit Rent Revenue, $1,500. | ||

debit Prepaid Rent, $1,500; credit Rent Expense, $1,500. | ||

debit Rent Expense, $1,500; credit Prepaid Rent, $1,500. |

3 points

Question 21

Corresponds to CLO 5(a) Lennox Corporation purchased a newdelivery truck for 35,000. The sales taxes are $2,700. The logo ispainted on the side of the truck for $800. The truck's annuallicense is $200. Annual insurance on the truck is $1,300. Whatshould Lennox record as the cost of the new truck?

$40,000 | ||

$38,500 | ||

$37,700 | ||

$35,000 |

3 points

Question 22

Corresponds to CLO 5(b) On April 1, 2013, Ballard Corporationpurchased equipment for $65,000. It is estimated that the equipmentwill have a $5,000 salvage value at the end of its 5 year usefullife. If Ballard uses the straight-line method of depreciation,what is the accumulated depreciation at December 31, 2013?

$13,000 | ||

$12,000 | ||

$9,750 | ||

$9,000 |

3 points

Question 23

Corresponds to CLO 5(c) Tyree Company purchased equipment with acost of $90,000 and an estimated salvage value of $18,000. Theequipment is expected to produce 150,000 units over its estimateduseful life of 10 years. If Tyree uses the units-of-activitymethod, what is the depreciation cost per unit to be used incalculating depreciation?

$1.67 | ||

$0.48 | ||

$2.08 | ||

$0.60 |

3 points

Question 24

Corresponds to CLO 5(d) Kerns Company purchased equipment with acost of $200,000 and an estimated salvage value of $10,000. Theequipment has an estimated useful life of 10 years. If Kerns usesthe double-declining balance method, what is the annualdepreciation rate to be used in calculating depreciation?

5% | ||

10% | ||

20% | ||

40% |

3 points

Question 25

Corresponds to CLO 6(a) Marshall Machinery made a sale for$150,000 on March 31. The customer is sent a statement on April 6and payment is received on April 15. Marshall prepares March'smonthly internal financial statements on April 20. Marshall followsGAAP and applies the revenue recognition principle. When is the$150,000 considered to be earned?

March 31 | ||

April 6 | ||

April 15 | ||

April 20 |

On January 1, 2013, NRC Credit Corporation leased equipment toBrand Services under a direct financing lease designed to earn NRCa 12% rate of return for providing long-term financing. The leaseagreement specified:

| a. | Twelve annual payments of $64,000 (including executory costs)beginning January 1, 2013, the inception of the lease and eachDecember 31 thereafter through 2021. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| b. | The estimated useful life of the leased equipment is 12 yearswith no residual value. Its cost to NRC was $403,080. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| c. | The leasequalifies as a capital lease to Brand. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| d. | A 12-year service agreement with Quality Maintenance Company wasnegotiated to provide maintenance of the equipment as required.Payments of $5,900 per year are specified, beginning January 1,2013. NRC was to pay this executory cost as incurred, but leasepayments reflect this expenditure. | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| A partial amortization schedule, appropriate for boththe lessee and lessor, follows

Assume the contract specified that NRC (the lessor) wasto pay, not only the $5,900 maintenance fees, but also insurance of$790 per year, and was to receive a $340 management fee forfacilitating service and paying executory costs. The lesseeâs leasepayments were increased to include an amount sufficient toreimburse executory costs plus NRCâs fee.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||