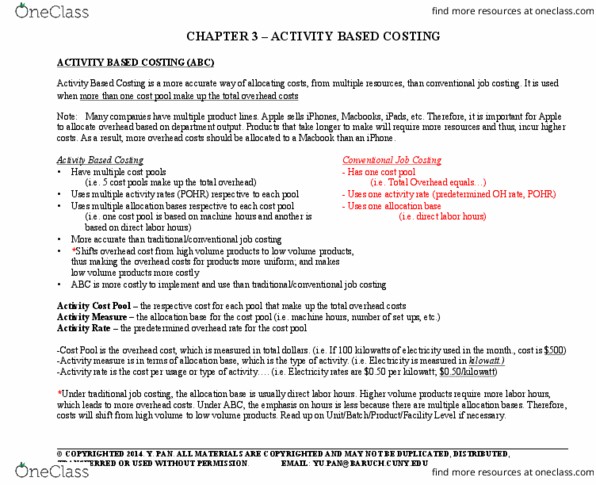

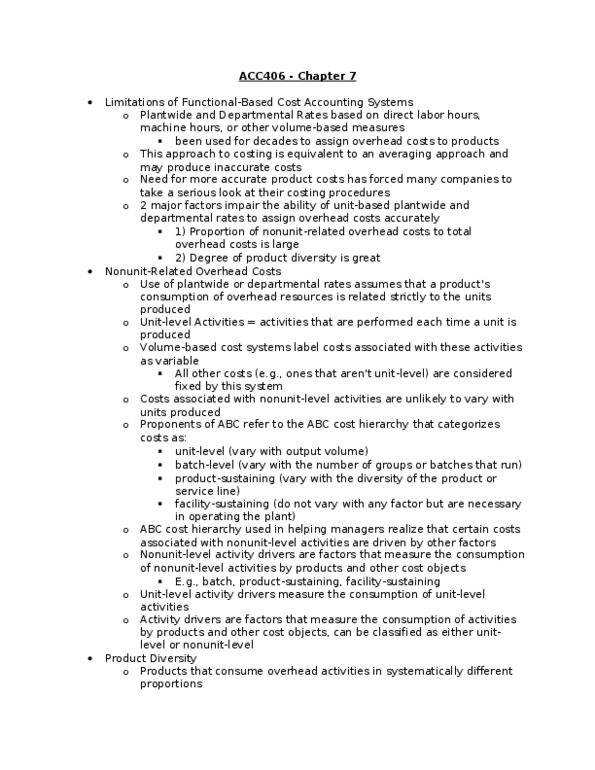

Activity based costing is considered a better method ofallocating manufacturing overhead than the more simplified"plant-wide" overhead allocation method.

a. Activity based costing doesrequire more work than a plant-wide allocation. Under whatcircumstances is it worth the extra effort?

b. What is the typically result when activity based costing isadopted, in terms of cost allocation between differentproducts?

c. Name three advantages of activity based costing overplant-wide allocation.

Please describe with details ALL questions, do not submitincomplete answer

Activity based costing is considered a better method ofallocating manufacturing overhead than the more simplified"plant-wide" overhead allocation method.

a. Activity based costing doesrequire more work than a plant-wide allocation. Under whatcircumstances is it worth the extra effort?

b. What is the typically result when activity based costing isadopted, in terms of cost allocation between differentproducts?

c. Name three advantages of activity based costing overplant-wide allocation.

Please describe with details ALL questions, do not submitincomplete answer

Related questions

Dakota Motors produces electric motors for commercial use. Until the end of 1994, only 2 models were produced, the âStandardâ modelâ and the âDeluxeâ model. The Deluxe model had more expensive components and raw materials, required more quality control and required more labor hours per unit to produce than the Standard model. Both models were produced in fairly large volume. Since 1994, in an attempt to grow its business, and in response to competitive pressures, Dakota Motors has begun producing many different varieties of electric motors, in addition to its regular models. These new models are tailor made to the needs of individual customers and are produced only on demand, and are typically low volume lines.

Dakota Motors has a simple (traditional) costing system which traces the costs of direct materials, components, and direct labor to each of its product lines. All support costs are assigned to product lines via a single plant wide overhead rate based on direct labor hours. Its volume of manufacturing activity has grown from 20,000 direct labor hours in 1994 to 30,000 direct labor hours in 1997.

Dakota Motorsâ accounting system is reporting a rapid escalation in the costs per unit of producing the Standard and Deluxe models. Management is puzzled and vexed by these cost increases, since the prices of various production inputs (such as labor, raw materials, components, engineers, supervisors, etc.) have increased only marginally during these years, and the production methods for producing the Standard and Deluxe models have not changed.

Below, is data regarding support activities, annual support costs and driver volumes:

| Support Costs | |||

| Support Activity | Cost driver | 1994 | 1997 |

| Supervision | Direct labor hours | $144,000 | $220,000 |

| Machine maintenance | Machine hours | $ 80,000 | $140,000 |

| Quality control | # of inspections | $ 40,000 | $100,000 |

| Machine set ups | # of setups | $ 20,000 | $120,000 |

| Process engineering | Engineering hours | $ 10,000 | $150,000 |

| Total support costs | $294,000 | $730,000 | |

| Standard | Deluxe | New Models | Total | |

| Direct labor hours | 12,000 | 8,000 | 10,000 | 30,000 |

| Machine hours | 14,000 | 12,000 | 14,000 | 40,000 |

| # of inspections | 400 | 400 | 600 | 1400 |

| # of setups | 11 | 9 | 100 | 120 |

| Engineering hours | 120 | 140 | 1,740 | 2,000 |

Assume that the production quantities and driver volumes for the Standard and Deluxe models have not changed between 1994 and 1997.

Questions:

1) Determine the total support costs assigned to the Standard model and to the Deluxe model in 1994 and in 1997 under the traditional costing system.

2) Calculate the cost driver rates and determine the support costs that would be assigned to the Standard, Deluxe and New models in 1997 under an activity based costing system. Be sure to display and label all your calculations.

3) Write a paragraph explaining to top management how the traditional costing system distorts product costs in Dakota Motors. Use the data on engineering hours and direct labor hours to quantitatively support your argument.