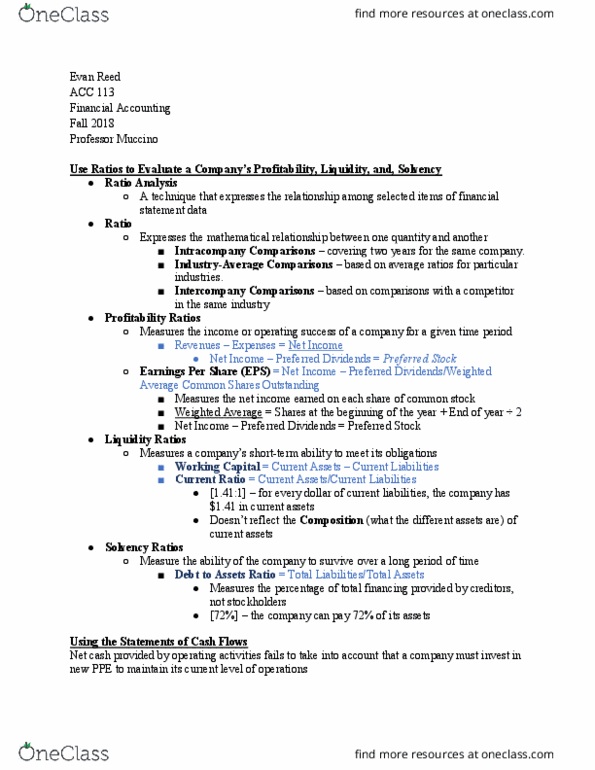

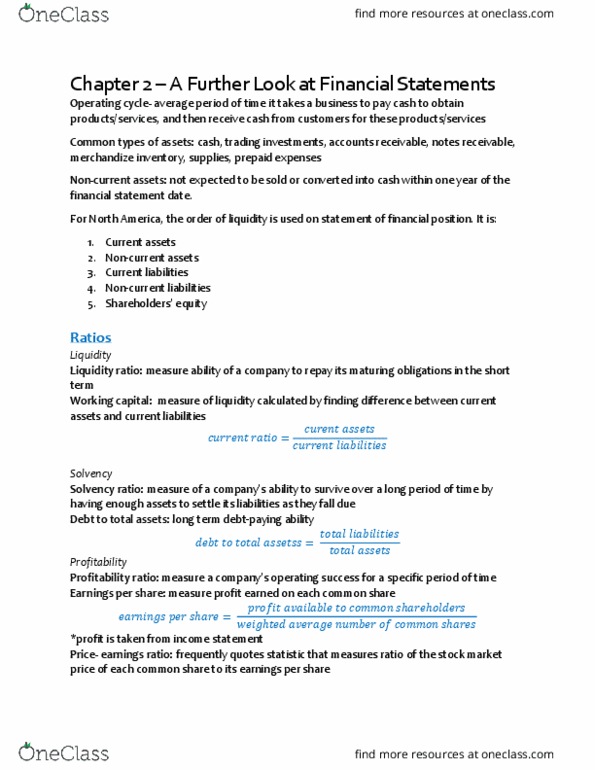

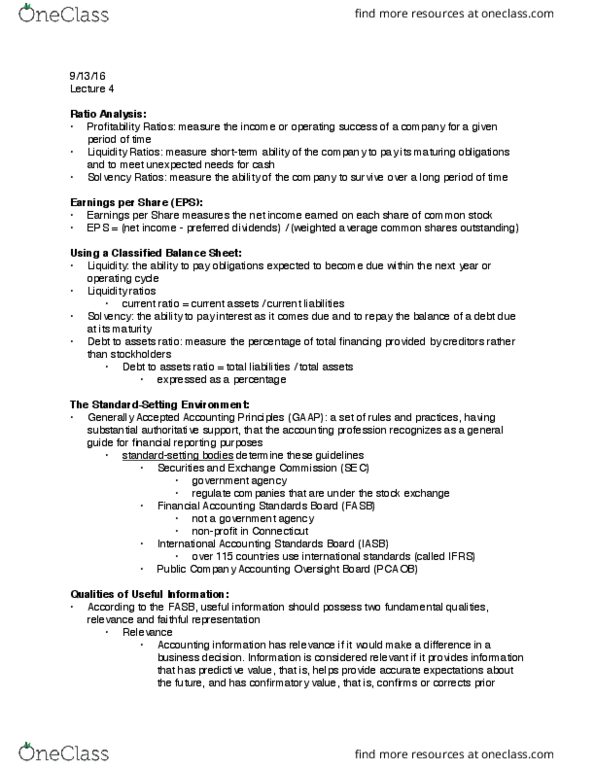

Class, hereâs a great opportunity for a peer response. Take alook at the ratios below. Select a category and examine how theseratios might be useful to an external financial statement user:Liquidity Ratios Working Capital = Current Assets â CurrentLiabilities Current Ratio = Current Assets / Current LiabilitiesQuick Ratio = (Current Assets â Inventory) / Current LiabilitiesLong-Term Solvency Ratios Debt to Assets Ratio = Total Liabilities/ Total Assets Debt to Equity Ratio = Total Liabilities / TotalEquity Interest Coverage Ratio = Earnings before interest and taxes/ Interest Expense

Class, hereâs a great opportunity for a peer response. Take alook at the ratios below. Select a category and examine how theseratios might be useful to an external financial statement user:Liquidity Ratios Working Capital = Current Assets â CurrentLiabilities Current Ratio = Current Assets / Current LiabilitiesQuick Ratio = (Current Assets â Inventory) / Current LiabilitiesLong-Term Solvency Ratios Debt to Assets Ratio = Total Liabilities/ Total Assets Debt to Equity Ratio = Total Liabilities / TotalEquity Interest Coverage Ratio = Earnings before interest and taxes/ Interest Expense

Related questions

Debt Management Ratios

Financial statements for Remington Inc. follow.

| RemingtonInc. | |||||

| ConsolidatedStatements of Income | |||||

| (In thousands exceptper share amounts) | |||||

| 2013 | 2012 | 2011 | |||

| Net sales | $ 7,245,088 | $ 6,944,296 | $ 6,149,218 | ||

| Cost of goods sold | (5,286,253) | (4,953,556) | (4,355,675) | ||

| Gross margin | $ 1,958,835 | $ 1,990,740 | $ 1,793,543 | ||

| General and administrativeexpenses | (1,259,896) | (1,202,042) | (1,080,843) | ||

| Special and nonrecurring items | 2,617 | - | - | ||

| Operating income | $ 701,556 | $ 788,698 | $ 712,700 | ||

| Interest expense | (63,685) | (62,398) | (63,927) | ||

| Other income | 7,308 | 10,080 | 11,529 | ||

| Gain on sale of investments | - | 9,117 | - | ||

| Income before income taxes | $ 645,179 | $ 745,497 | $ 660,302 | ||

| Provision for income taxes | 254,000 | 290,000 | 257,000 | ||

| Net income | $ 391,179 | $ 455,497 | $ 403,302 | ||

| Net income per share | $1.08 | $1.25 | $1.11 | ||

| RemingtonInc. | ||||||

| ConsolidatedBalance Sheets | ||||||

| (In thousands) | ||||||

| ASSETS | Dec. 31,2013 | Dec. 31,2012 | ||||

| Current assets: | ||||||

| Cashand equivalents | $ 320,558 | $ 41,235 | ||||

| Accounts receivable | 1,056,911 | 837,377 | ||||

| Inventories | 733,700 | 803,707 | ||||

| Other | 109,456 | 101,811 | ||||

| Total current assets | $2,220,625 | $1,784,130 | ||||

| Property and equipment, net | 1,666,588 | 1,813,948 | ||||

| Other assets | 205,342 | 248,372 | ||||

| Total assets | $4,092,555 | $3,846,450 | ||||

| LIABILITIES ANDSTOCKHOLDERS' EQUITY | ||||||

| Currentliabilities: | ||||||

| Accounts payable | $ 250,363 | $ 309,092 | ||||

| Accrued expenses | 347,892 | 274,220 | ||||

| Other current liabilities | 15,700 | - | ||||

| Income taxes | 93,489 | 137,466 | ||||

| Total current liabilities | $ 707,444 | $ 720,778 | ||||

| Long-term debt | $ 650,000 | $ 541,639 | ||||

| Deferred income taxes | 275,101 | 274,844 | ||||

| Other long-term liabilities | 61,267 | 41,572 | ||||

| Total liabilities | $1,693,812 | $1,578,833 | ||||

| Stockholders'equity: | ||||||

| Common and preferred stock | $ 189,727 | $ 189,727 | ||||

| Additional paid-in capital | 128,906 | 127,776 | ||||

| Retained earnings | 2,397,112 | 2,136,794 | ||||

| $2,715,745 | $2,454,297 | |||||

| Less: Treasury stock, at cost | (317,002) | (186,680) | ||||

| Total stockholders' equity | 2,398,743 | $2,267,617 | ||||

| Total liabilities and stockholders'equity | 4,092,555 | $3,846,450 | ||||

Required:

Using Remington's financial statements as shown above, respondto the following requirements.

1. Compute the five debt management ratios for2012 and 2013. Round your answers to two decimal places.

| 2013 | 2012 | |

| Times interest earned | ||

| Debt to equity ratio | ||

| Debt to total assets ratio | ||

| Long-term debt to equity ratio | ||

| Long-term debt to total assetsratio |

2. Conceptual Connection: Indicate whether theratios have changed significantly from 2012 to 2013.

Select All the ratios decreased,Times interest earned ratiodecreased, other ratios did not change by much., Debt to equityratio decreased, other ratios did not change by much., Debt tototal assets ratio decreased, other ratios did not change by much,Long-term-debt to equity ratio decreased, other ratios did notchange by much, Long-term-debt to total assets ratio decreased,other ratios did not change by much.

B. Do the ratios suggest that Remington is more or less riskyfor long-term creditors at December 31, 2013, than at December 31,2012? Explain.

SelectMore risky for long-term creditors Less risky forlong-term creditors