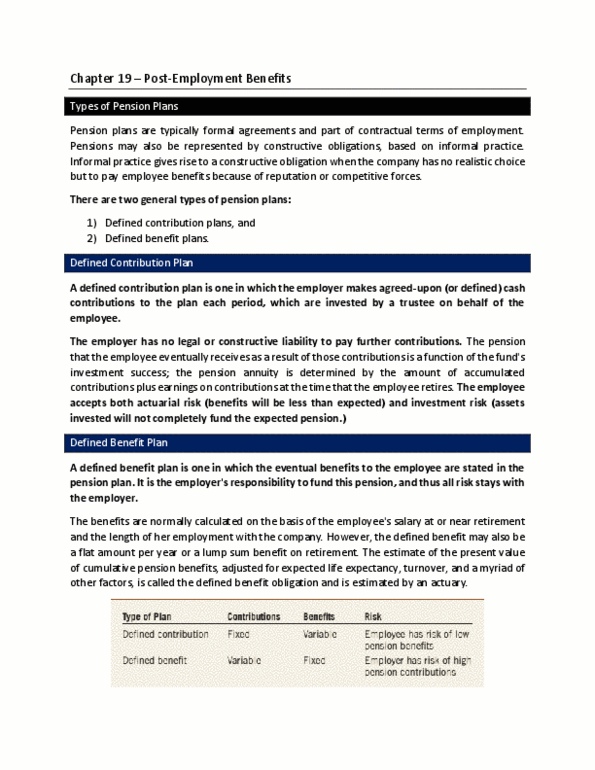

Ballooning Out of Control LLC (âBLOCâ or the âCompanyâ) is amanufacturer of hot air balloons. Because of decreased demand forhot air balloons and challenging industry conditions, BLOCâsmanagement is exploring ways to reduce the Companyâs rapidly risingcompensation and benefit costs. Management has determined it willeither (1) amend the Companyâs single-employer defined benefitpension plan by eliminating the future earning of pension benefitsfor its employees (i.e., freeze its pension plan) or (2) reduceheadcount across the Company by 5 percent. Either option willrequire approval by BLOCâs board of directors.

If BLOC decides to freeze its current pension plan, it will notoffer any new pension benefits to its employees through anotherplan. BLOCâs current pension plan is the only retirement benefitarrangement it provides to its employees. The planâs pensionbenefits are based on years of service and average salary for thelast five years of the employeeâs service period, and allemployees, both hourly and salaried, who have attained six monthsof service are participants in the pension plan.

Under the plan freeze, the Company will eliminate the accrual ofadditional pension benefits for future service. However, theCompany will continue to take future salary increases into accountin computing the average salary for the last five years beforeretirement when determining the pension benefits earned for servicebefore the plan freeze. (This type of plan amendment is commonlyreferred to as a âsoft freeze.â)

The pension plan freeze will be effective on October 1, thebeginning of BLOCâs next fiscal year, and is expected to beapproved and communicated to employees before BLOCâs September 30year-end.

If BLOCâs management decides instead to reduce costs by reducingheadcount by 5 percent, it anticipates that the board of directorswould approve the reductions and management would communicate itsplans to the affected employees before September 30. Beforechoosing which cost-cutting plan to recommend to the board ofdirectors, management would like to determine how to account foreach alternative.

Required: 1. Determine how to account for each of the followingalternative actions to reduce BLOCâs increasing compensation andbenefit costs:

a. Management decides to amend the pension plan by eliminatingthe accrual of pension benefits for future service while continuingto take future salary increases into account in determining pensionbenefits at retirement (i.e., a soft freeze).

b. Management decides to permanently lay off 5 percent of BLOCâsplan eligible workforce while retaining the current pensionplan.

2. What are the differences, if any, between the requirements ofU.S. GAAP and IFRSs in accounting for the two alternative actionsmanagement, is considering?

Ballooning Out of Control LLC (âBLOCâ or the âCompanyâ) is amanufacturer of hot air balloons. Because of decreased demand forhot air balloons and challenging industry conditions, BLOCâsmanagement is exploring ways to reduce the Companyâs rapidly risingcompensation and benefit costs. Management has determined it willeither (1) amend the Companyâs single-employer defined benefitpension plan by eliminating the future earning of pension benefitsfor its employees (i.e., freeze its pension plan) or (2) reduceheadcount across the Company by 5 percent. Either option willrequire approval by BLOCâs board of directors.

If BLOC decides to freeze its current pension plan, it will notoffer any new pension benefits to its employees through anotherplan. BLOCâs current pension plan is the only retirement benefitarrangement it provides to its employees. The planâs pensionbenefits are based on years of service and average salary for thelast five years of the employeeâs service period, and allemployees, both hourly and salaried, who have attained six monthsof service are participants in the pension plan.

Under the plan freeze, the Company will eliminate the accrual ofadditional pension benefits for future service. However, theCompany will continue to take future salary increases into accountin computing the average salary for the last five years beforeretirement when determining the pension benefits earned for servicebefore the plan freeze. (This type of plan amendment is commonlyreferred to as a âsoft freeze.â)

The pension plan freeze will be effective on October 1, thebeginning of BLOCâs next fiscal year, and is expected to beapproved and communicated to employees before BLOCâs September 30year-end.

If BLOCâs management decides instead to reduce costs by reducingheadcount by 5 percent, it anticipates that the board of directorswould approve the reductions and management would communicate itsplans to the affected employees before September 30. Beforechoosing which cost-cutting plan to recommend to the board ofdirectors, management would like to determine how to account foreach alternative.

Required: 1. Determine how to account for each of the followingalternative actions to reduce BLOCâs increasing compensation andbenefit costs:

a. Management decides to amend the pension plan by eliminatingthe accrual of pension benefits for future service while continuingto take future salary increases into account in determining pensionbenefits at retirement (i.e., a soft freeze).

b. Management decides to permanently lay off 5 percent of BLOCâsplan eligible workforce while retaining the current pensionplan.

2. What are the differences, if any, between the requirements ofU.S. GAAP and IFRSs in accounting for the two alternative actionsmanagement, is considering?