Overhead Variances, Four-Variance Analysis, Journal Entries Laughlin, Inc., uses a standard costing system. The predetermined overhead rates are calculated using practical capacity. Practical capacity for a year is defined as 1,000,000 units requiring 200,000 standard direct labor hours. Budgeted overhead for the year is $750,000, of which $300,000 is fixed overhead. During the year, 900,000 units were produced using 190,000 direct labor hours. Actual annual overhead costs totaled $800,000, of which $294,700 is fixed overhead. Required: 1. Calculate the fixed overhead spending and volume variances. Fixed Overhead Spending Variance $ Fixed Overhead Volume Variance $ 2. Calculate the variable overhead spending and efficiency variances. Variable Overhead Spending Variance $ Variable Overhead Efficiency Variance $ 3. Prepare the journal entries that reflect the following: Assignment of overhead to production Recognition of the incurrence of actual overhead Recognition of overhead variances Closing out overhead variances, assuming they are not material Note: Close the variances with a debit balance first. For compound entries, if an amount box does not require an entry, leave it blank or enter "0". a. b. c. d.

Overhead Variances, Four-Variance Analysis, Journal Entries Laughlin, Inc., uses a standard costing system. The predetermined overhead rates are calculated using practical capacity. Practical capacity for a year is defined as 1,000,000 units requiring 200,000 standard direct labor hours. Budgeted overhead for the year is $750,000, of which $300,000 is fixed overhead. During the year, 900,000 units were produced using 190,000 direct labor hours. Actual annual overhead costs totaled $800,000, of which $294,700 is fixed overhead. Required: 1. Calculate the fixed overhead spending and volume variances. Fixed Overhead Spending Variance $ Fixed Overhead Volume Variance $ 2. Calculate the variable overhead spending and efficiency variances. Variable Overhead Spending Variance $ Variable Overhead Efficiency Variance $ 3. Prepare the journal entries that reflect the following: Assignment of overhead to production Recognition of the incurrence of actual overhead Recognition of overhead variances Closing out overhead variances, assuming they are not material Note: Close the variances with a debit balance first. For compound entries, if an amount box does not require an entry, leave it blank or enter "0". a. b. c. d.

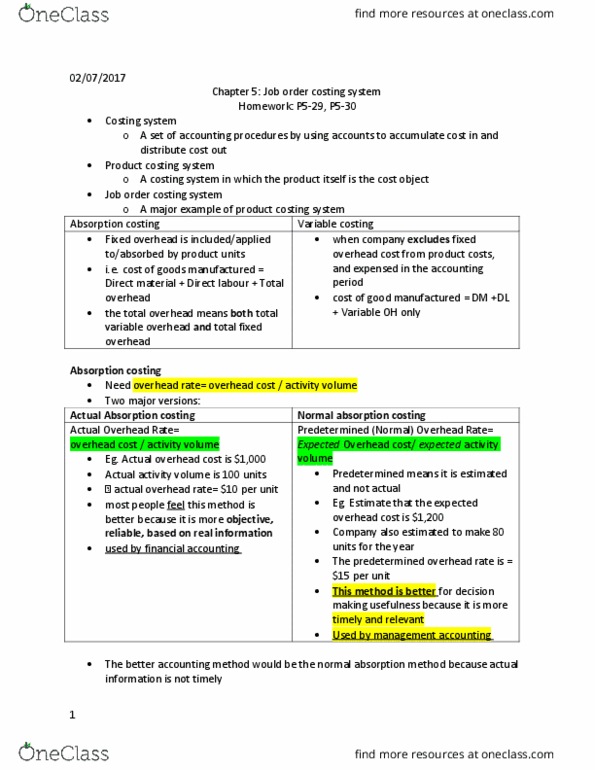

Related questions

Exercise 9.22

Overhead Variances, Four-Variance Analysis, Journal Entries

Laughlin, Inc., uses a standard costing system. Thepredetermined overhead rates are calculated using practicalcapacity. Practical capacity for a year is defined as 1,000,000units requiring 200,000 standard direct labor hours. Budgetedoverhead for the year is $750,000, of which $300,000 is fixedoverhead. During the year, 900,000 units were produced using190,000 direct labor hours. Actual annual overhead costs totaled$800,000, of which $294,700 is fixed overhead.

Required:

1. Calculate the fixed overhead spending andvolume variances.

| Fixed Overhead Spending Variance | $ | - Select your answer -FavorableUnfavorableCorrect 2 of Item1 |

| Fixed Overhead Volume Variance | $ | - Select your answer -FavorableUnfavorableCorrect 4 of Item1 |

2. Calculate the variable overhead spending andefficiency variances.

| Variable Overhead Spending Variance | $ | - Select your answer -FavorableUnfavorableCorrect 6 of Item1 |

| Variable Overhead Efficiency Variance | $ | - Select your answer -FavorableUnfavorableCorrect 8 of Item1 |

3. Prepare the journal entries that reflect thefollowing: Assignment of overhead to production Recognition of the incurrence of actual overhead Recognition of overhead variances Closing out overhead variances, assuming they are notmaterial Note: Close the variances with a debit balance first.For compound entries, if an amount box does not require an entry,leave it blank or enter "0".

| ||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

Overhead Variances, Four-Variance Analysis

Oerstman, Inc., uses a standard costing system and develops itsoverhead rates from the current annual budget. The budget is basedon an expected annual output of 128,000 units requiring 512,000direct labor hours. (Practical capacity is 532,000 hours.) Annualbudgeted overhead costs total $844,800, of which $604,160 is fixedoverhead. A total of 119,500 units using 510,000 direct labor hourswere produced during the year. Actual variable overhead costs forthe year were $262,000, and actual fixed overhead costs were$555,550.

Required:

1. Compute the fixed overhead spending andvolume variances.

| Fixed Overhead Spending Variance | $ | |

| Fixed Overhead Volume Variance | $ |

2. Compute the variable overhead spending andefficiency variances. Do not round intermediate calculations

| Variable Overhead Spending Variance | $ | |

| Variable Overhead Efficiency Variance | $ |

Exercise 9.16

Overhead Variances, Two- And Three-Variance Analyses

Oerstman, Inc., uses a standard costing system and develops itsoverhead rates from the current annual budget. The budget is basedon an expected annual output of 120,000 units requiring 480,000direct labor hours. (Practical capacity is 500,000 hours.) Annualbudgeted overhead costs total $787,200, of which $556,800 is fixedoverhead. A total of 119,400 units using 478,000 direct labor hourswere produced during the year. Actual variable overhead costs forthe year were $230,600, and actual fixed overhead costs were$556,250.

Required:

1. Compute overhead variances using atwo-variance analysis.

| Budget Variance | $_____ | Favorable or Unfavorable |

| Volume Variance | $_____ | Favorable or Unfavorable |

2. Compute overhead variances using athree-variance analysis.

| Spending Variance | $____ | Favorable or Unfavorable |

| Efficiency Variance | $____ | Favorable or Unfavorable |

| Volume Variance | $____ | Favorable or Unfavorable |